Introduction

I like real estate. But I only like REIT’s when they are trading at attractive valuations. About six months ago I warned for complacency at Eurocommercial Properties (OTC:EUCMF) as although the property valuations do make sense in the current investment climate, Eurocommercial would have to deal with a higher leverage ratio in a stress test scenario (using higher required rental yields than Eurocommercial’s own base case). We’re now six months later and Eurocommercial has published its financial results of the first semester of 2019, so I will have another look at its portfolio, and stress-test the NAV and LTV performance.

Source: Yahoo Finance

Eurocommercial Properties is a Dutch REIT listed on Euronext Amsterdam with ECMPA as its ticker symbol. The current market capitalization based on the 49.75M shares (technically: ‘depository receipts’) is 1.274B EUR. The average daily trading volume in Amsterdam is 90,000 shares.

A decent performance

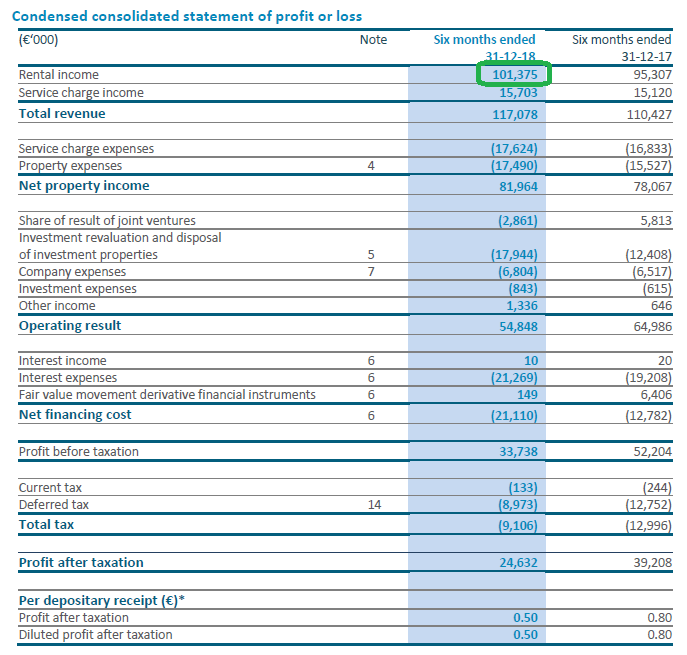

In the first six months of the year, Eurocommercial Properties reported a gross rental income of 101.4M EUR (unfortunately Eurocommercial does not provide unique URLs for its press releases. All press releases can be found here), which is a 6% increase compared to the first half of the previous financial year. As the property expenses remain relatively high (approximately 83% of the gross rental income gets converted into the net property income), and as Eurocommercial continues to (slightly) reduce the fair value of its real estate, the company reported a net income of 24.6M EUR, or 50 (euro) cents per share.

Source: Eurocommercial half-year report

Of course, a REIT should never be valued based on an EPS as A) property revaluations could have a major impact on the bottom line of the income statement although these are just ‘estimates’ and don’t provide a real income and B) the majority of Eurocommercial’s taxes are deferred taxes. The rental income doesn’t get taxed and the taxes on the (paper) profits on the revaluation of the real estate assets is only payable when the properties effectively get sold.

On a cash flow basis, Eurocommercial’s operating cash flow was approximately 77.5M EUR before deducting the 19.6M EUR in interest expenses. Which would result in a net cash flow of 58M EUR. The EPRA earnings were indeed 57.6M EUR, which translates to 1.16 EUR per share. On a full-year basis, it does look like the EPRA earnings should exceed 2.30 EUR per share, which provides a little bit of wiggle room for Eurocommercial to increase its dividend from 2.15 EUR per share to 2.20 EUR per share (Eurocommercial tries to increase its dividend on a yearly basis, but may have to limit itself to just a token 0.01 EUR increase this year if the situation doesn’t improve).

The low ‘net initial yields’ still bother me…

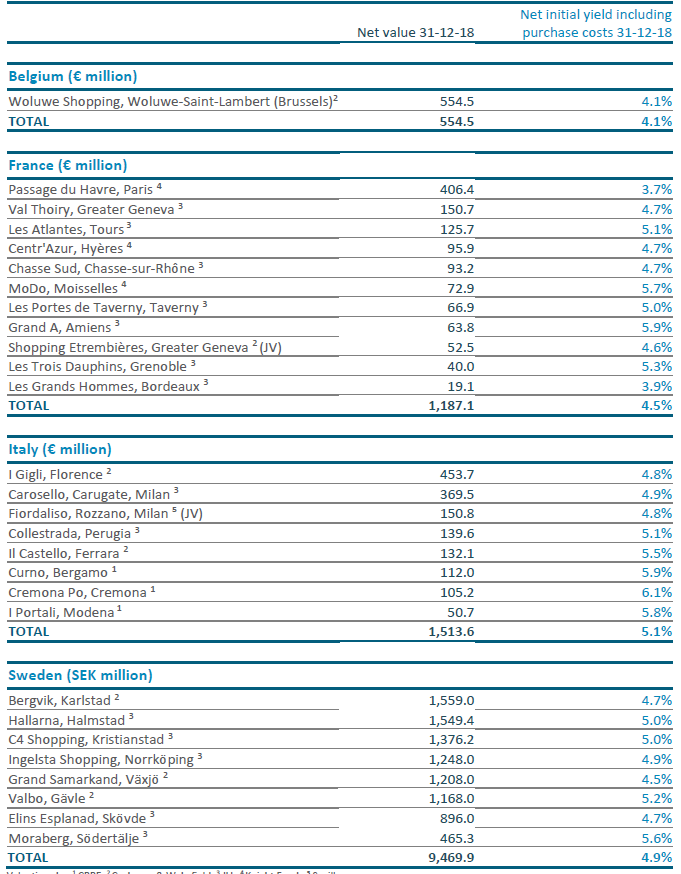

It’s always nice to see a REIT trading below its self-declared Net Asset Value (the EPRA NAV stood at 43.38 EUR/share and the NNNAV (the Triple Net Asset Value, explained here) at 37.64 EUR per share as of the end of December), but it’s also always very interesting to see how these NAV’s have been calculated, and which rental yields Eurocommercial has been using to justify its valuations.

Source: Eurocommercial half-year report

Does this mean Eurocommercial’s property valuations are too optimistic? Not necessarily, the market is what it is, and we have seen other transactions in the commercial real estate space that confirm the current valuations. However, this doesn’t mean the valuations will remain at sub-5% levels as there is an obvious correlation between the risk-free interest rate and the required returns on real estate. Now the official interest rates are still around 0%, valuing real estate properties at a 4.5-5% required return makes sense. But should we see a more normalized interest rate of 2%, Eurocommercial’s valuation experts will have to hike their yield metrics as well based on a mark-up on the risk-free interest rate.

… so I stress-tested Eurocommercial based on more conservative parameters

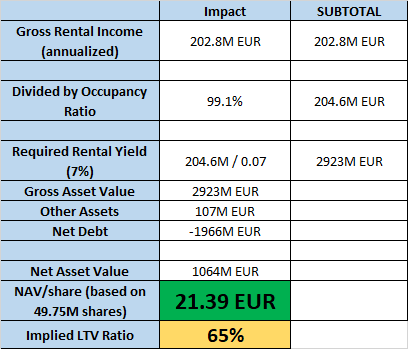

Considering I’d like to use a more conservative approach to value the assets in a more adverse market scenario with a higher required rental yield, I ran my own numbers based on a required yield of 7%. This provides me with two important elements. First of all, it shows a more conservative NAV/share which allows us to make a comparison between Eurocommercial’s own NAV and the NAV in a stress test scenario. Additionally, it will also provide more insight on how the LTV ratio will evolve based on the more conservative NAV calculations.

I am using a required gross rental yield of 7% (resulting in a net rental yield of approximately 5.7% using a similar ratio of net rental yield versus gross rental yield as in the first semester). I am also adding the 107M EUR in development assets and investments in joint ventures back to the equation.

Source: author calculation based on publicly available data and own assumptions

As you can see, this would result in a NAV/share of 21.39 EUR which is still relatively fine, but the LTV would jump to a substantially higher level, even alarmingly close to the 60% maximum.

This doesn’t mean Eurocommercial should go into panic mode, but it does indicate it should take some action by making the stock dividend as attractive as possible (rather than pricing it at a premium as the previous conversion rate for the stock dividend was higher than the share price at that time) and perhaps sell some assets at the current high valuations to protect itself against more adverse market scenarios.

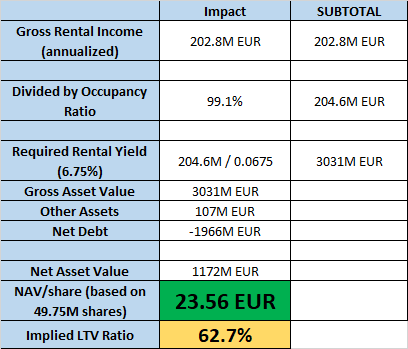

I also ran the numbers based on a required gross rental income yield of 6.75%:

Source: author calculation based on publicly available data and own assumptions

The 0.25% change in required rental yield has a substantial impact on the NAV/share which increased by 10%, but only a small impact on the LTV ratio, which remains above 60% in this scenario.

Eurocommercial still has plenty of time to strengthen its balance sheet and continuing to issue stock dividends while avoiding any purchases of malls at a rental yield of less than 5%, and Eurocommercial should be fine. If during the next two years 75% of the shareholders would elect to take the dividend in stock, Eurocommercial would retain 164M EUR in cash and even under the strict 7% required yield scenario, this would be sufficient to reduce the LTV ratio to less than 60%. So again, there’s no reason to be alarmed, but I wanted to raise the issue by providing this sensitivity analysis anyway.

Investment thesis

I do like Eurocommercial’s assets and core focus on the Netherlands, France, Italy and Belgium (since the purchase of the Woluwe mall) but I’m still not convinced about the valuations used to determine the fair value of the assets (especially after seeing how the value of the recently acquired Woluwe mall jumped from 453M EUR in June to 555M EUR in December compared to an effective purchase price of 468M EUR. I don’t think seller AG Insurance was so stupid to sell the property almost 100M EUR below the current ‘fair value’).

Despite this, I have recently increased my position in Eurocommercial Properties by 50% as the current share price already reflects a substantial part of the risks I explained. Ideally, Eurocommercial sells an additional asset (or perhaps two) just to be safe. Considering the Swedish economy was pretty weak in Q4 and given the valuation metrics of the Swedish portfolio (a 4.9% net rental yield) and the currency risk, I think it could make sense to follow Wereldhave (WRDE F) and monetize some of its Swedish assets (which make up approximately 1/4 th of the balance sheet total).

Consider joining European Small-Cap Ideas to gain exclusive access to actionable research on appealing Europe-focused investment opportunities, and to the real-time chat function to discuss ideas with similar-minded investors!

NEW at ESCI: A dedicated EUROPEAN REIT PORTFOLIO!

Take advantage of the TWO WEEK FREE TRIAL PERIOD and kick the tires!

Disclosure: I am/we are long EUCMF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment