The Company

Krystal Biotech Inc. (KRYS) is a clinical-stage gene therapy company based in Pittsburgh, PA, which is founded in 2015 and has its IPO in September 2017.

It develops novel, “off-the-shelf”, topical gene therapies for serious genetic skin diseases.

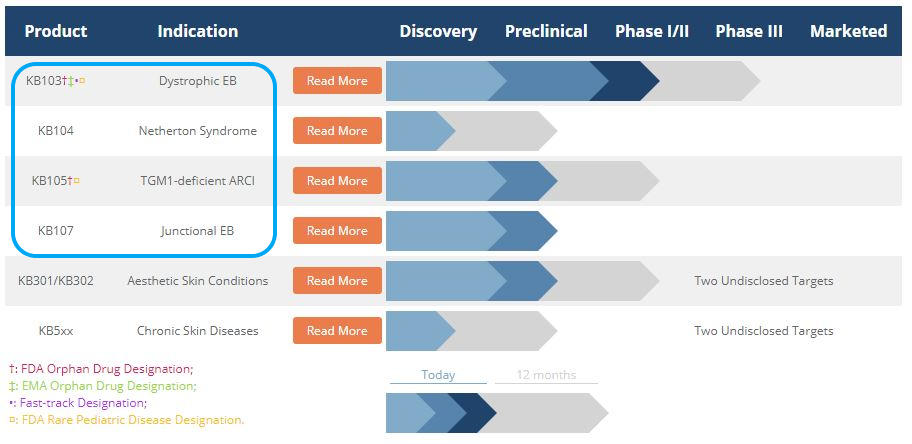

Based on the strength of their proprietary technology (to be discussed further below), the company currently focuses on the most severe congenital genetic skin diseases, including their lead indication, Dystrophic Epidermolysis Bullosa (or DEB), as shown within the blue box of the pipeline summary below.

(Source: Company website. blue highlight by the author)

The technology

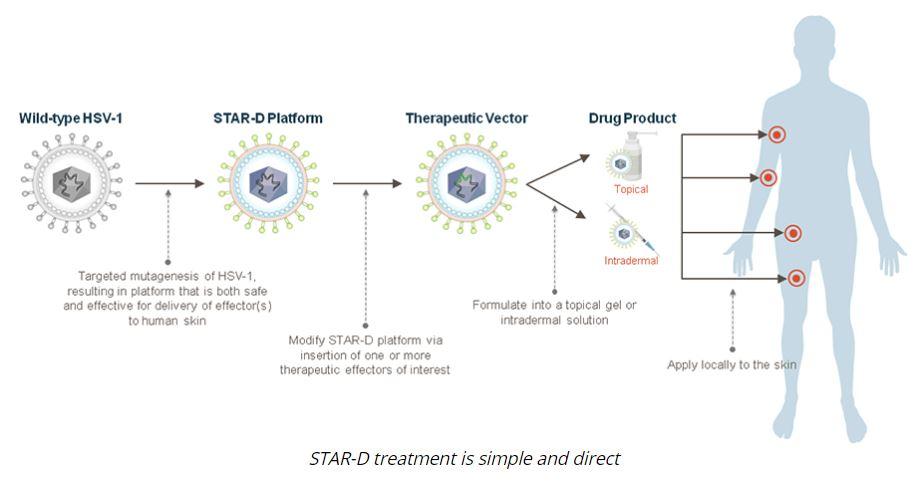

According to the company, they have developed a proprietary gene therapy platform, which they call the Skin TARgeted Delivery (or STAR-D) platform.

STAR-D platform produces gene therapies that use an engineered HSV-1 vector that the company believes can efficiently penetrate a broad range of skin cells, to then deliver to these skin cells the therapeutic (i.e. fully functional) gene.

As a result, the protein that is missing or defective due to the defective gene, that causes the disease, is able to be expressed by the patient’s skin cells to carry out their normal function.

(Source: Company website)

(Source: Company website)

The Vector

HSV-1 stands for type 1 herpes simplex virus, which causes cold sores and genital herpes. In recent years, HSV usage as a safe and effective vector in gene therapy has been extensively studied (here, here, here)

In 2015, Amgen’s IMLYGIC (a genetically modified HSV-1) was approved by the FDA as the first oncolytic viral therapy for melanoma.

According to the company, their proprietary technology can genetically modify HSV1 so that as a gene therapy vector, it is “replication-defective,” and “non-integrating” while still being able to efficiently penetrate a broad range of skin cells.

Simply put, the company believes that through their genetic modification they can get rid of what’s harmful about HSV1 (e.g. disruption of the host cells’ genome by integrating their own viral DNA; viral replication; and killing the host cell), while keeping what is useful for therapeutic purposes (e.g. the ability to penetrate skin cells; the ability to hide from the body’s immune system; large capacity for carrying therapeutic genes; and the ability to get the skin cells to express the fully-functional protein).

On KRYS’s website, six distinct advantages of STAR-D treatment over other viral gene therapy vectors are listed. They are:

- it can be administered topically as an “off-the-shelf” product (vs. autologous gene therapies, which use patients own cells that have to be harvested, genetically modified, then put back in by grafting or injection. All of which is accomplished through much more involved and complicated processes).

- it transduces dividing and non-dividing cells, increasing the efficiency of therapeutic gene transfer (vs. lower transduction efficiency of other vectors).

- it is non-replicating and is diluted by cell divisions, leading to transient transgene expression (vs. permanent alteration of the genome of the patients’ skin cells).

- its high payload capacity can accommodate large or multiple genes (vs. smaller payloads achievable with other vectors).

- it allows for repeat administration (vs. single administration).

- it does not insert itself into, or otherwise disrupt, the human genome (i.e. no potential risks of cancer or mutation).

The Lead Indication

The Dystrophic Epidermolysis Bullosa Research Association (or Debra) of America described the disease as ‘the worst disease you’ve never heard of’.

Epidermolysis Bullosa (ep-i-der-mo-lie-sis bu-low-suh), or EB, is a rare genetic connective tissue disorder that affects 1 out of every 20,000 births in the United States (approximately 200 children a year are born with EB). There is no treatment or cure. There are many genetic and symptomatic variations of EB, but all share the prominent symptom of extremely fragile skin that blisters and tears from minor friction or trauma. Internal organs and bodily systems can also be seriously affected by the disease. EB is always painful, often pervasive and debilitating, and is in some cases lethal before the age of 30. EB affects both genders and every racial and ethnic background equally. Daily wound care, pain management, and protective bandaging are the only options available for people with EB.

EB patients are endearingly described as ‘the butterfly children’ because their skins are as fragile as the butterflies wings.

[embedded content]

(Source: Debra of America website)

The cost of the palliative care is estimated to be around $200k to $400k annually.

Dystrophic EB (or DEB) is a subset within EB. According to Debra International, 500,000 people worldwide are estimated to live with EB and 25% of all EB patients (~125,000) have DEB.

Phase 1/2 DEB Trial

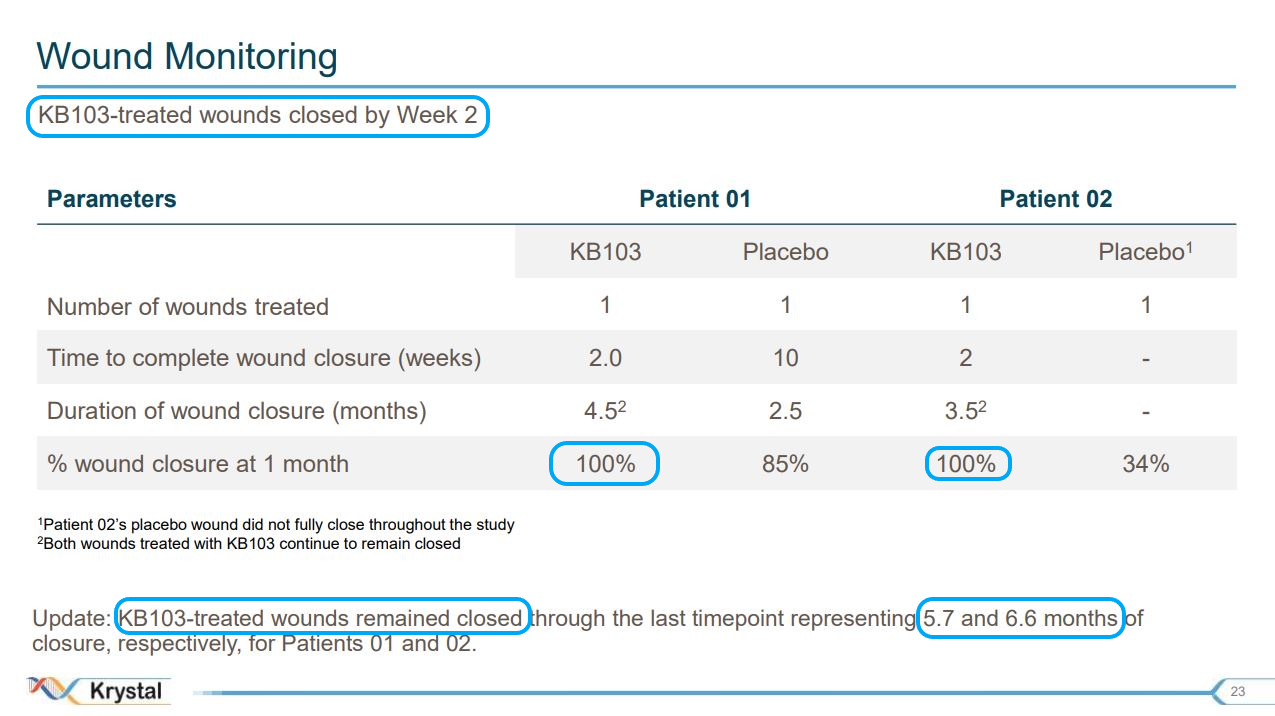

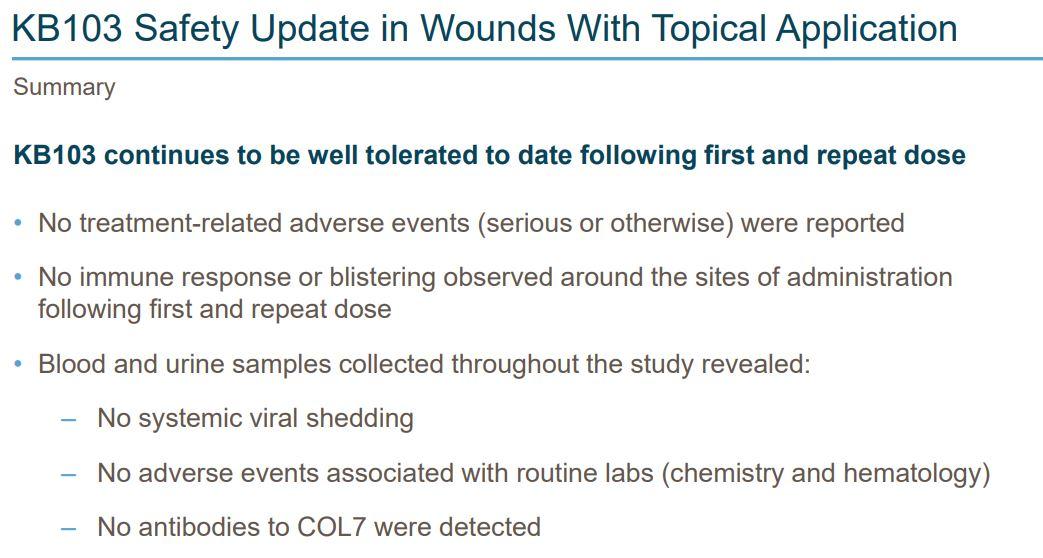

In Q4 2018, the company reported positive early data from their phase 1/2 DEB trial.

It is a small, open label, placebo-controlled trial of two adult patients, with two wounds from each patients being studied, one treated with placebo, the other with KB103 (Krystal’s DEB treatment).

The early data is promising, as seen in the tables below and image.

(Source: Company Q1 2019 Presentation, slide 23)

(Source: Company Q1 2019 Presentation, slide 23)

(Source: Company Q1 2019 Presentation, slide 27)

(Source: Company Q1 2019 Presentation, slide 27)

(Source: Company Q1 2019 Presentation, slide 25)

(Source: Company Q1 2019 Presentation, slide 25)

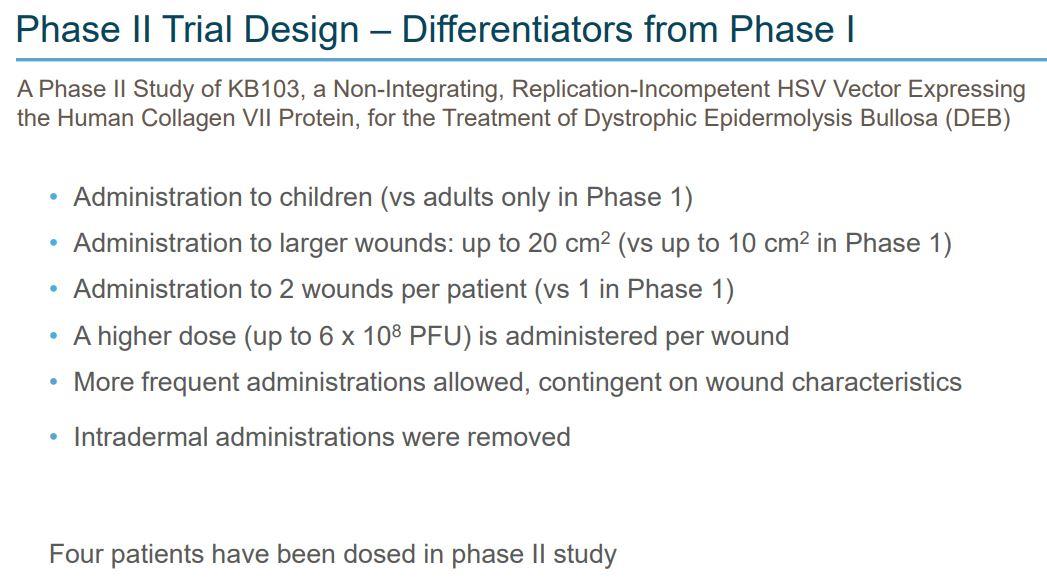

Since these results, the company has enrolled and dosed four more patients. There are some differences in the trial design (see below). The top-line results are expected in 1H 2019.

If successful, the company plans to start the phase 3 in 2H 2019.

(Source: Company Q1 2019 Presentation, slide 29)

(Source: Company Q1 2019 Presentation, slide 29)

Competitive Landscape in DEB market

In their latest 10-K (page 10), this is what the company states with regards to their DEB competitors:

A number of companies are developing drug candidates for EB. At this time, there is no FDA- or EMA-approved treatment for DEB. We believe our competitors fall into three broad categories:

•

Autologous Approaches: We are aware of two companies, Abeona and Fibrocell who are developing autologous or grafting gene therapy approaches to treating DEB.

•

Palliative Treatments: We are aware of companies such as Castle Creek Pharma who are developing product candidates taking a palliative approach to treating the disease.

•

Non-Gene Therapy: We are aware that ProQR Therapeutics has a product candidate in clinical development that intends to treat a subset of genetic defects that cause RDEB with a topical RNA-based treatment.

Both Abeona (ABEO) and Fibrocell (FCSC) reported positive phase 1/2 trial results.

Both also have recently announced that they will start their respective phase 3 trial in 1H 2019 (ABEO’s PR; FCSC’s 10-K, page 3)

Provided that KYRS’s phase 1/2 full data is successful and their phase 3 starts as planned, I estimate that all three companies share similarly high probability to succeed in their respective phase 3 trials, given their positive early data and strong scientific rationals.

If this estimation proves to be correct, it will put these companies in a similar time frame to obtain the FDA approval in DEB, though granted that ABEO and FCSC have a 6 months lead time in starting their p3 trial.

As discussed previously, KRYS’s gene therapy is distinctly different from the autologous gene therapy approaches of ABEO and FCSC with the advantages of being a simple, easy-to-use, safe to repeat, potential lower price tag topical gene therapy product.

In addition, ABEO and FCSC seem to focus on the recessive DEB (or RDEB) patients, a subset of DEB. If so, this will reduce their target patient number.

All this is to say that in my opinion, KYRS remains very competitive for DEB market uptake, if approved, despite being the last one to start their phase 3 trial.

A Few Notables

Since its 2017 IPO, KRYS has nearly tripled its stock price and continues to make new 52 wk highs.

(Source: Google)

(Source: Google)

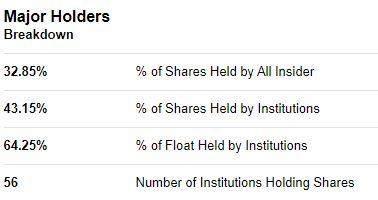

According to finel.io, the ownership of institutional ownership has soared recently.

(Source: Fintel.io: KRYS Ownership)

(Source: Fintel.io: KRYS Ownership)

The same confidence is seen also in the high percentage of insider’ ownership (~33%).

(Source: Yahoo Finance)

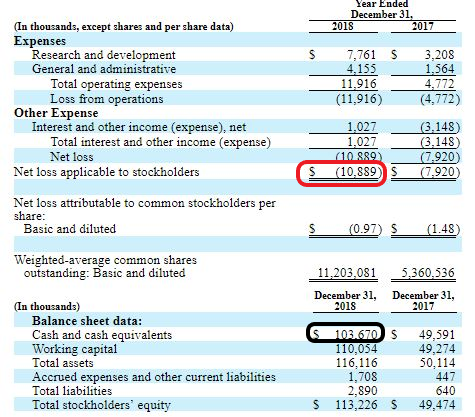

Financial results

For the year ended December 31, 2018, the company has

- Cash, cash equivalents and short-term investments totaled $103.7 million on December 31, 2018.

- Net losses for the years ended December 31, 2018 were $10.9 million.

(Source: Company 10-K, page 47)

It’s impressive how cost effective KRYS is in their execution considering that in 2018 they have opened a cGMP facility to support their ongoing DEB trial and future commercialization. All this is accomplished with an annual burn rate of $10M.

With the available cash of >$100M going forth, the near-term dilution risk is probably minimum.

Final Thoughts

Before I conclude, I want to remind readers that investing in any clinical stage biotech company is a highly risky undertaking.

Please beware that there can be no guarantee of success in clinical trials. Even with the best scientific rationals, positive prior results, or bullish SA articles, it’s always a clear and present danger ((risk)) that a trial will report less-than-expected results or even end in a complete failure.

That’s what a clinical trial is purposed to do–to vigorously study if a drug candidate is truly safe and effective in its target indication among the target patients.

When less-than-expected data is reported, the stock often crashes significantly and will take a long time, if ever, to recover.

Furthermore, the price action of small/micro cap biotech stocks can be very volatile and be driven up/down by short-term, irrational market movements.

For these two reasons, Krystal Biotech may not be suitable for many whose risk tolerance or time frame would make any clinical stage biotech stocks a bad fit.

Nevertheless, for those who think long term, who value the fundamentals of what constitutes a successful drug developer–to succeed in developing safe/effective drugs in meeting serious unmet medical needs and to do so effectively (profitably) in due course, Krystal biotech is a strong BUY!

According to a RnR March Research report, the global Dermatology market is estimated to reach $33.7B by 2022.

With their impressive speed and early success in the DEB so far, Krystal Biotech may very well run with the same zeal and efficiency with their 3 other orphan genetic diseases. If/when they succeed in developing these drugs, the company has further plans to go into other skin conditions and chronic skin diseases that have broader markets.

The market cap of Krystal Biotech is ~$431M (March 28, 2019). If/when some or all the indications are successfully developed, even a 1% of the global Dermatology market share will translate to an annual revenue of $337 M, which could easily justify a market cap of $1.69B (=5X$337M) or more.

Any potential investor needs to also consider the long term risks, which are that the company may fail in some or all of its programs, becoming unsuccessful or not viable commercially in the long run.

Thank you very much for reading! I hope that my article is helpful for your own DD. All the best.

Disclaimer: This articles is not an investment advice, and I am not an investment adviser. Small cap biotech stocks are highly volatile, speculative, and risky. Investing in these stocks may result in a partial or complete loss of investment. Conduct your own due diligence and/or consult a certified financial adviser before making any decision to buy, sell or hold any stock. You alone are responsible for your investment decisions, actions and results.

Disclosure: I am/we are long KRYS, ATBPF, PFSCF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment