We have two theories about what the US-China trade war is all about, and the difference in impact on the markets can hardly be more significant.

For the markets, the optimistic theory is that this is all about Trump’s eagerness for closing a deal and declare victory. The pessimistic view is that we are in the first innings of a hegemonic confrontation between the premier economic powers in the world.

Like other countries, the US can feel aggrieved by Chinese trade practices, especially since China entered the WTO in 2001:

- China developed a large trade surplus and kept its currency low to make inroads in world trade.

- Production moved to China to take advantage of cheap resources and the biggest growth market opportunity around, costing probably millions of US manufacturing jobs.

- At a minimum, China displayed a cavalier attitude towards foreign IP and at worst, it systematically set out to steal it.

- China hasn’t opened up its economy as many hoped it would.

- China hasn’t given up on supporting domestic industries with cheap credit and other forms of support, especially for the still large state-owned sector.

- Economic development hasn’t made China move towards being more of a liberal democracy (as many hoped WTO membership and economic development would achieve).

In short, while China might have played by at least most of the rules of that WTO membership, it hasn’t played by its spirit. While this is true, it is also a little one-sided:

- The US has also benefited from cheap Chinese imports (keeping inflation down) and Chinese investments in the US (keeping interest rates down) and exports to China have also multiplied.

- US companies have benefited enormously by locating parts of their supply networks to China and sourcing from China.

- Much of the huge US bilateral trade deficit with China is a mirage, with much of the value added not actually being produced in China.

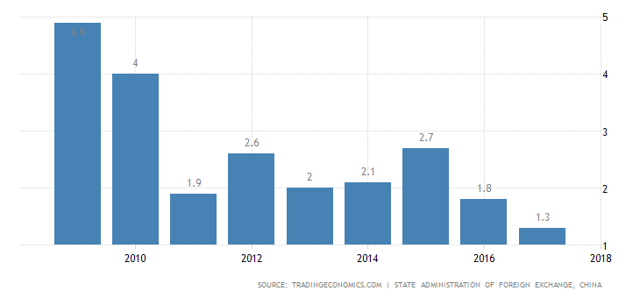

- China has nearly eliminated its huge trade surplus (see below).

- Exports have markedly declined as a percentage of Chinese GDP (see below).

- Rather than manipulating its currency downwards, the last four years or so the PBoC (the People’s Bank of China) tried to keep it up.

- There are experts (see here and here) who argue that China’s record on IP protection has been improving (which isn’t that strange, given the fact that they are themselves a big source of IP).

Here is how the Chinese trade surplus declined:

And here is how the Chinese economy has decreased its dependence on exports:

This is a rather amazing decline in the relative importance of exports and it has mostly gone unnoticed.

Scenarios

We see basically two scenarios for the trade war:

- The optimistic scenario: Trump declares a win and calls off the trade war.

- The pessimistic scenario, a clash of the old and the new hegemonic powers.

In the optimistic scenario, Trump simply calls a win after some Chinese concessions. There is quite a bit to be said for this:

- Trump doesn’t even really need a real win as he’s prone to declare wins where only cosmetic changes exist. As long as he can sell it to his base as something significant, the actual facts on the ground matter a great deal less (this is what happened with NAFTA or North Korea, for instance).

- The Chinese are indeed offering some concessions, like lower tariffs on imported US cars, more purchases of US agricultural and energy goods and the like.

- Trump might be quite anxious to get a big win under his belt, given the government shutdown saga, the ongoing Mueller investigation, the high turnover in his administration, etc.

- An ongoing trade war with the background of a weakening world economy and the waning effects of the tax cuts is an increasing negative of the stock market. Trump tends to see the stock market as a barometer of his success, the fourth-quarter declines might bring home the reality that trade wars aren’t so easy to win and that he’s got quite a bit to lose as well.

Hegemonic conflict

This view sees the trade war as a cover for something much more profound, a conflict between the old hegemonic power and the increasing threat from an emerging new one.

The trade war is one in name only, the real goal is to slow down China’s seemingly inexorable economic and geo-political rise, if not outrightly stop it in its tracks. Here is Peter Morici on MarketWatch:

China’s bilateral trade surplus is at the epicenter of its efforts to achieve parity or surpass the United States as the pre-eminent global superpower. This contest is waged in four theaters — the Korean Peninsula, the South China Sea and broader Pacific and Indian Oceans, the race for dominance in artificial intelligence, and most importantly, the standoff over trade…

China is building a navy to challenge American sea power. That shakes confidence among our Southeast Asian friends, and it has established a naval base on the Horn of Africa and has taken possession of a vital port in Sri Lanka. With the Belt and Road Initiative, China is financing a network of ports and rail connections stretching from China to Europe and duping developing nations, like Sri Lanka, into debt servitude. Importantly, it seeks an undisputed sphere of influence through island nations stretching from Taiwan to Sri Lanka and the Maldives and on to the Horn of Africa.

You’ll get the picture. It’s interesting to note that Morici sees the bilateral trade surplus as a crucial underpinning of China’s global ambitions. This seems to suggest that even if the trade war is a proxy for a battle for global hegemony, it nevertheless serves as a means to derail these Chinese ambitions:

All of this takes hundreds of billions of dollars to buy, develop and as necessary illegally appropriate Western technology and hardware ranging from port cranes to fighter aircraft to artificial intelligence enabled hardware and software. It’s substantially financed by China’s elaborate trade and industrial policies designed to foster trade surpluses with the United States.

Cutting the bilateral deficit will cut Chinese access to dollars and China will face real constraints on executing its ambitions. Quite frankly, we think this is nonsense.

Assume for a moment that China is forced into trade concessions, for instance by importing lots more from the US (cars, energy, agriculture, etc.). Insofar as this moves the overall Chinese trade balance into deficit, it will simply plunge its currency.

This move is probably enhanced by the economic slowdown and subsequent capital flight (and the loosening of policy to combat the economic slowdown). Even in the absence of these events, it isn’t difficult for China to engineer a depreciation of its currency.

If you think Morici’s vision is an outlier, think again. The Trump administration contains at least two known lifelong China trade hawks, Robert Lighthizer and Peter Navarro.

Robert Lighthizer has been a lifelong swamp creature lobbying for the steel industry and against everything that threatened to come on its path, like lobbying for cutting the funding of the International Trade Commission (a US semi-independent advice body on trade cases) when its research showed US steel wasn’t hobbled by unfair competition from imports as the Bush administration argued.

He has been a lifelong adversary of the WTO (which ruled against the US even after the ITC was buffeted by pressure) which he sees as an unwarranted constraint on US sovereignty. His views on China are equally predictable (The Atlantic):

He wants to roll back China’s advances on the global economy. His zeal for that mission comes directly from his years working on behalf of American steel interests.

And of course Peter Navarro is there with him as the author of “Death by China” has argued for years that China needs to be confronted.

There are a series of events and actions that have us concerned the hegemonic conflict is on the upper hand:

- A much less accommodating attitude on Chinese acquisition efforts of US tech companies has already been operative

- The issuing of a Section 301 (1974 Trade Act) report on China, listing its economic crimes.

- The Section 301 allows the President unilateral action on trade practices he deems unfair or harming and this was the basis of the tariffs imposed on Chinese exports.

- The undermining of the WTO, which poses limits on the use of Section 301.

- The arrest of the CFO (and daughter of the founder) of Huawei, one of China’s premier tech companies.

- The targeting of American companies with manufacturing activities in China, like Apple (NASDAQ:AAPL).

- With Jim Mattis gone, Lighthizer’s influence on foreign policy, in which China looms large, is enhanced.

A central issue for the trade warriors is the Made in China 2025 program, an industrial policy program aimed at moving China up the value chain and spearhead it into a dominant position in 10 advanced technology sectors (like 5G, AI, new materials, robotics, biotech, aerospace, new-energy vehicles, etc.).

Here is Bloomberg (our emphasis):

These are things that if China dominates the world, it’s bad for America,” U.S. Trade Representative Robert Lighthizer told a Senate committee this month. The U.S. now sees China as a strategic rival and imposing such curbs would mark a concrete shift in its strategy toward containing China’s ascent in advanced industries.

As it happens, China 2025 is modeled on a similar German initiative to propel this country into the fourth industrial revolution called Industry 4.0 Development Plan, with the side note that it can be argued that Germany, with its 8%+ trade surplus, is a much bigger drain on international trade than China.

On the other hand, the German subsidies are generally much smaller and more on the level of basic research, and Germany places much less conditions on foreign investment and doesn’t have state-owned companies that are marshaled as an asset in attaining its ambitions.

In one way China 2025 is actually nothing new. China already expressed the ambition to become a world leader in science and technology in 2006. What the US objects to is how China tries to achieve these objectives, because this involves a central role for the state and proposes a different capitalist model, state-led capitalism.

It isn’t necessarily the ambitions of China 2025, but the means with which China tries to realize these, involving unfair competition, forced technology transfers and even outright IP theft and industrial espionage.

On the latter, Chinese network infrastructure producers like Huawei and ZTE are at the forefront of the battle. Here is US economist Jeffrey Sachs (our emphasis):

The US requested that Canada arrest Meng in the Vancouver airport en route to Mexico from Hong Kong, and then extradite her to the US. Such a move is almost a US declaration of war on China’s business community. Nearly unprecedented, it puts American business people traveling abroad at much greater risk of such actions by other countries.

The US rarely arrests senior business people, US or foreign, for alleged crimes committed by their companies. Corporate managers are usually arrested for their alleged personal crimes (such as embezzlement, bribery, or violence) rather than their company’s alleged malfeasance.

Meng was arrested for her company’s violations of sanctions on Iran, but Sachs goes on to list a host of companies who did the same, many of which US companies but none of their officers got arrested, the company paid fines. In stark contrast, ZTE was nearly bankrupted over sanctions violations.

It is also based on US law forcing third-party companies to adhere to US sanction policies, but Sachs notes that surely US companies would not like to be dictated to who they can and can’t sell by foreign governments, let alone have their officers arrested if they don’t adhere to these rules.

Perhaps even more importantly:

The US is trying to targeting Huawei especially because of the company’s success in marketing cutting-edge 5G technologies globally. The US claims the company poses a specific security risk through hidden surveillance capabilities in its hardware and software. Yet the US government has provided no evidence for this claim.

But there are already sales limits on Huawei and ZTE in the US. In 2012, a report by the House Intelligence Committee declared Huawei and ZTE threats to national security due to the potential for Beijing to use their networks for spying or sabotage, and the Commerce department restricted their ability to sell their products, contract with government agencies, and otherwise operate in the United States.

Note the report speaks of the potential for China to use their networks for spying or sabotage, there is no proof this actually happens. There is US pressure on allies to do the same. Australia, New Zealand and British Telecom have already banned the companies.

This isn’t going away

And indeed, Trump came to some rapport with President Xi in Buenos Aires, resulting in a 3-month truce and there are new soundbites indicating that the actual negotiations are proceeding pretty well, for what those are worth.

However, China is in a bit of a bind as the room for manoeuvre is limited because Xi’s power could be said to rest on two pillars:

- Economic success

- Nationalism

Caving too much to US demands can stave off a further economic slowdown but at the cost of undermining Xi’s nationalist credentials. And the margins are thin as industrial growth is already stalling with the PMI actually below 50 and (Asia Times):

Manufacturing activity has declined, consumer spending has shrunk and new car sales have stalled. A cooling property market has also been squeezed by tighter credit restrictions.

And the effect of the tariffs has yet to kick in so China might be willing to offer substantial concessions, at least on parts where it is not required to fundamentally change their economic model.

And there is now also pressure on Trump with the rapid declines in the US stock markets, which he considers a crucial barometer of success of his economic policies.

But even if the US and China manage to arrive at some kind of agreement that avoids the further implementation of tariffs, a new era has begun, according to the Asia Times:

The year to come might herald the official start of a long Sino-US cold war with global ramifications, even if an elusive trade breakthrough can be achieved. After decades of economic growth and a “peaceful rise,” a new chapter of open strategic competition between Washington and Beijing has begun. This new environment will hang over all the key issues China’s leadership will face in 2019, from domestic politics to economic strategy, or diplomacy, making the next 12 months a potential watershed.

Increasing conflict seems inevitable from the natural evolution of the Chinese economy. Until now, the US and Chinese economies were largely complementary but with the Chinese ambitions to move up the value chain, competition with established US companies is inevitable.

And the ring of inevitability expands to other domains, like military and geo-political as the ever bigger Chinese economy underpins ambitions to play a more important role on the world stage.

China’s ambition to become more independent from foreign, especially US, technology actually chimes well with most anti-China parts of the US administration, so we could see a gradual unwind of the massive economic interdependence between the economies.

It’s a pity, because trade isn’t a zero sum game, as the trade warriors seem to have lost sight of.

It also spells trouble, as we remember the central idea of one of the founding fathers of the European Union Jean Monnet – which is that economic integration rises the cost of war to such extent as to become unthinkable.

Conclusion

It’s unlikely the trade war will go away anytime soon. The problem is simply that the economic rise of China poses a threat to US dominance and China is unlikely to change its model of state-led capitalism that has produced an economic miracle the past four decades the world has not seen before.

But it is possible we get an important respite. The fall in US markets has increased the likelihood that Trump will accept whatever concessions China has on offer and declare victory, even if this isn’t likely to fundamentally change the hegemonic conflict between the two countries.

The risk is, the longer we have to wait for a resolution, the more the market will continue in turmoil and the more likely it is to affect world growth. A deal may come too late to reverse the negative momentum.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment