Photo Credit: Miranda Patti & Alyssa Ockerbloom

Summer is the best time of the year in New England. The below-freezing temperatures, 3-day blizzard power outages, genital-numbing ocean water, depressing gray skies, and yellow and brown vegetation have finally disappeared. It’s now time to enjoy warm days at the beach, cool summer nights, refreshing (but still very cold) water, beautiful blue skies, green trees, and fresh cut grass (does a better smell exist?).

Since Summer is so short in New England, most of us, including myself, do anything we can to enjoy it to the fullest. Therefore, it’s been awhile since I’ve published an article on Seeking Alpha.

This growing desire to enjoy every Summer like it’s your last can be quite distracting. But because of this feeling, I realize the benefit of building your own dividend growth and value portfolio. No matter how fun or distracting life gets, your portfolio will be working hard to complete your goals. Other investments like rental properties or owning a small business are probably going to keep you busy during your favorite times of the year.

It also doesn’t take much time to monitor a dividend portfolio of this kind. I am approaching 30 positions, and only really care about 30 headlines a year. The most important headline that I want to see is if my stocks are raising their dividend. It is true; I will read the occasional earnings report or the infrequent major news headline that may involve one of my stocks, but if my companies are increasing their dividend payment every year, I know that my stocks are performing well enough to continue owning.

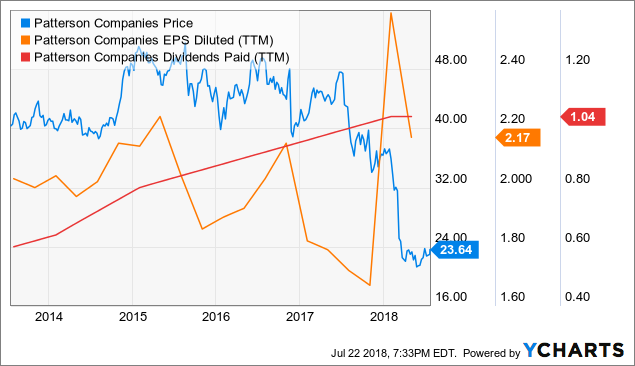

Now that I found some free time during my “Summer of Fun” schedule, I would like to share with you one of my latest additions to my portfolio; Patterson Companies (PDCO). PDCO is worth a look because of its strong financials, fundamentals, and dividend.

Patterson Companies

PDCO is one of the largest medical distributors and wholesalers of dental and animal health products, equipment, and devices in the United States. Although not a well-known stock or exciting investment idea, PDCO is a well-managed company that is trading below value. The results from my stock rating system are as follows:

|

Criteria |

PDCO @ $23.64 |

Score |

|

Total Assets/Total Liabilities>= 1.5 |

1.95 |

100% |

|

Long Term Debt/Net Assets <= 1.10 |

1.07 |

100% |

|

Positive EPS Streak of 5 Years |

5 |

100% |

|

Dividend > 0 |

1.04 |

100% |

|

Current EPS > 5 Years Ago |

2.16>1.97 |

100% |

|

#6 Price/Book <= 1.2 |

1.53 |

72% |

|

#7 P/E(ttm) < 10 |

10.94 |

91% |

|

Higher Dividend Streak > 4 Years |

8 |

100% |

|

Current Yield >= 3% |

4.40% |

100% |

|

Payout Ratio < 50% |

48.1% |

100% |

|

FCF/Dividend Payout >=1 |

1.41 |

100% |

|

5 Year DGR >= 10% |

12.50% |

100% |

|

3 Year DGR/5 Year DGR >= 1 |

0.66 |

66% |

|

Final Score: |

94% |

|

Sources: Morningstar, David Fish’s U.S. Companies with 25+ Straight Years Higher Dividends, GuruFocus, & Author Calculations

I scored PDCO a 94% which is a near-perfect score. This high score is derived from an excellent balance sheet, strong financial metrics, and a healthy and growing dividend.

When I look at a balance sheet, I focus on a few key numbers and ratios. The current assets outweigh the total liabilities by a factor of 1.95. This is one of the highest current ratios I have seen when analyzing dividend growth stocks. Because of this high ratio, the company has little risk and no threat of being able to pay its short-term bills with cash and/or cash equivalents at any given time. The long-term debt is also relatively low in comparison to its working capital (1.07 ratio). PDCO passes the important stress test question: in an emergency can you pay off all your long-term debt in an instance with available capital? The answer is a ‘yes’, meaning that PDCO has effectively managed its risk and is operating at healthy debt levels, unlike a spend-happy 16-year-old racking up credit card debt at the mall.

The valuation metric P/B is one of PDCO’s minor weaknesses as it stands at 1.53. Although the company is trading at a slightly higher price relative to its net asset value, it still sports a 10.94 P/E which is nearly 10 P/E under its 5-year average of 20.67. One can make a strong case that PDCO is priced at its best value in relation to its EPS in the last 5 years.

EPS has increased by 9.6% in the last 5 years. During that same time, PDCO’s stock price has fallen by about 40%. Does it make sense when a stock falls by 40% while becoming nearly 10% more profitable and maintaining an attractive net asset value? This company cannot be overlooked as far as value is concerned.

The dividend has been increased by management for 8 years in a row now. Current yield stands at 4.04% and is well protected with a low payout ratio of 48.1% and 136 million of FCF. The dividend growth rates are very attractive, and I see no reason why PDCO cannot continue to raise their dividend by an inflation crushing 8.2% (3-year average) clip.

PDCO has impressive financial and valuation metrics that should not be ignored. The dental distribution industry does not seem to be in a state of panic as Americans will continue to visit the dentist 1-2 times a year. I’ve also noticed a positive culture change where Americans care a lot more about what their pets are consuming. PDCO distributes a lot of healthy and organic options for animals that continue to keep pet owners happy and their fluffed-faced counterparts happy as well.

One should always perform due diligence before deciding to purchase any stock. I encourage investors to take a deeper look into PDCO’s management and forward-looking guidance before buying stock. Regardless, PDCO needs to be considered as an addition to one’s diversified dividend portfolio. It may be summer in New England, but I’m making sure I have the time to acquire and learn more about this profitable and consistent company while it’s stock price is so low.

Disclosure: I am/we are long PDCO.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment