We’ve been investing in the common stock of Assured Guaranty (AGO) for nearly 10 years now. Our investments have largely been centered on buying stock outright and selling cash-secured puts. During this past decade the business has faced numerous negative headlines, and the stock has been chronically undervalued. While the stock’s performance has been very strong for us at T&T Capital Management, the reality is that the stock currently trades at one of the largest disconnects between price and intrinsic value in its history. This disconnect allows the long-term investor a fantastic opportunity to buy shares in a business that has its best new business production potential in a decade.

Source: AGO 3rd Quarter 2018 Equity Investor Presentation

All images are from same presentation.

Over the past nine years, AGO’s insured book of business has dropped dramatically due to amortization and refundings. Structured Finance in particular, represents a very small part of the insured portfolio, with much of the formerly troublesome RMBS exposure covered by rep and warranty protection agreements. Assured Guaranty was able to remain profitable on an operating basis through the Financial Crisis, the bankruptcies of Detroit, Jefferson County, and Puerto Rico etc. Insurance companies are built to pay claims as an ongoing part of their business. I’ve found that because AGO’s claims occur in such a public and political manner, that the reaction in markets is usually overly dramatic.

Many of AGO’s competitors couldn’t fully honor their commitments and ended up having to restructure. AGO of course has always honored its obligations, and it has taken years for the company to rebuild the market for bond insurance, from a market that had been burned by some of the companies that failed to pay all principal and interest on defaulted bonds when due. Record-low interest rates and slim credit spreads have also reduced demand. The beauty is that AGO now operates in a uniquely attractive business with very little competition. The only other company writing new business is Build America Mutual, which has a rather weak balance sheet and profit record up to this point. The fact that it is rated as high as AGO’s subsidiaries is pretty laughable in my opinion.

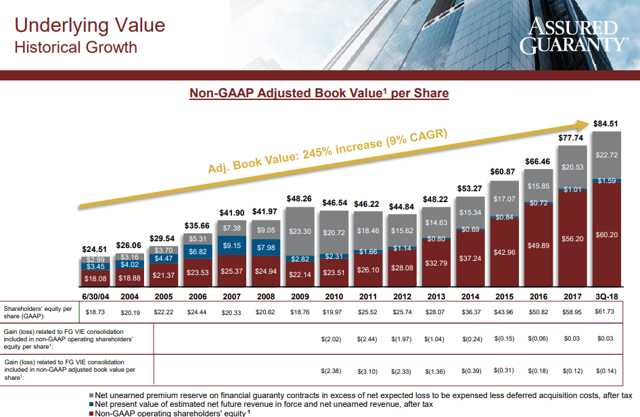

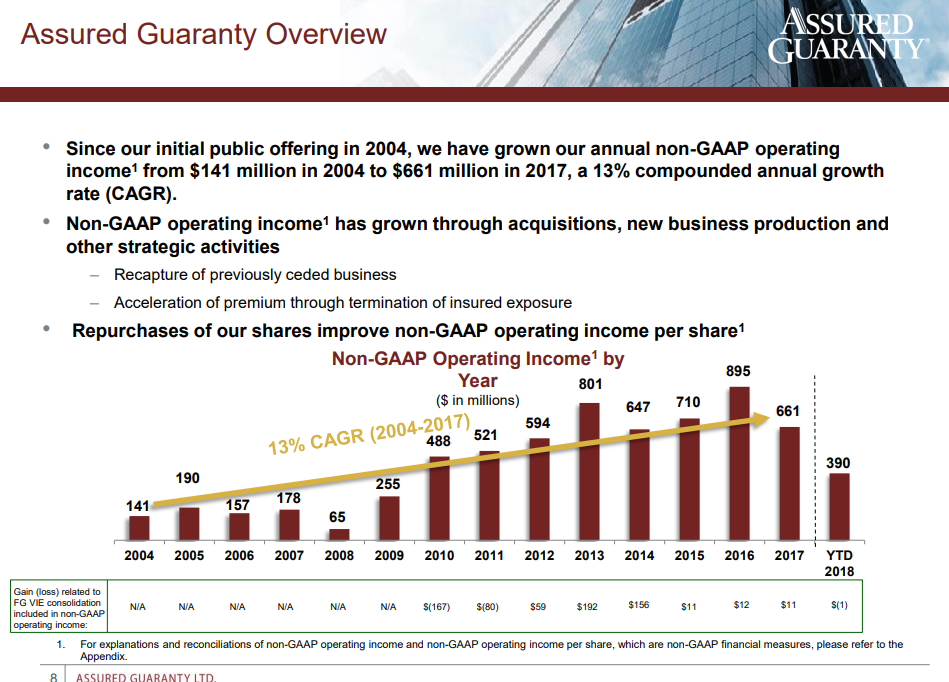

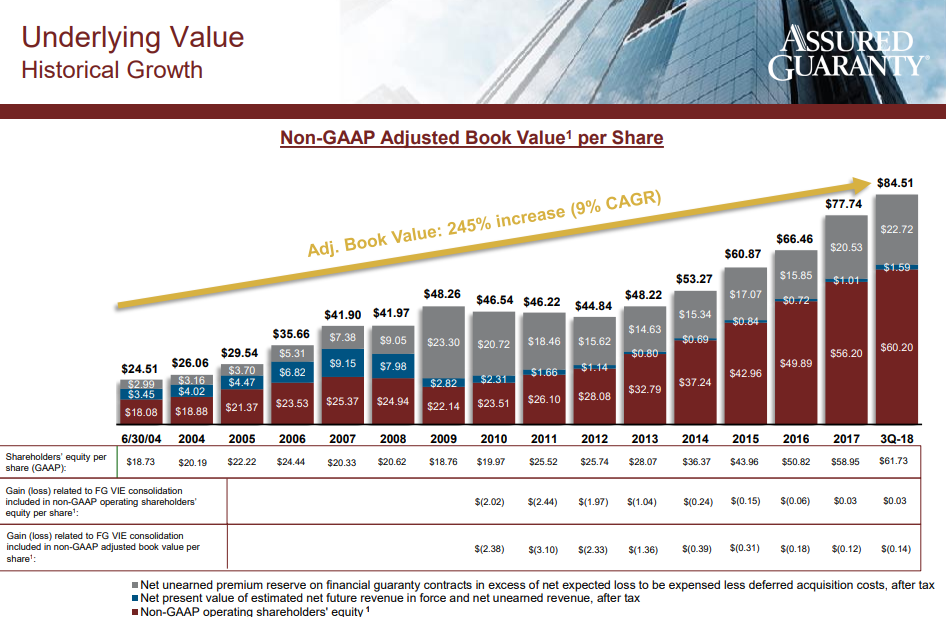

Assured Guaranty has one of the best CEO’s I’m aware of in Dominic Frederico. Dominic understands prudent capital allocation and him and his team have been good underwriters of credit risk. The company avoided insuring the CDO-squareds and much of the subprime garbage that killed off its competitors. Because AGO’s stock has always been very reactionary to headlines, the stock has traded at material discounts to intrinsic value. Management have been very smart about taking advantage of the bargain price of its shares with an aggressive. yet responsible buyback program. From the beginning of the program in 2013, the company has reduced its shares outstanding by 48%. This combined with robust financial results have created explosive growth in all of its book value per share metrics as seen above. Amazingly, despite buying nearly $500MM a year of its own stock, the company’s investment portfolio has basically held steady, while its insured leverage ratios have all gotten materially better.

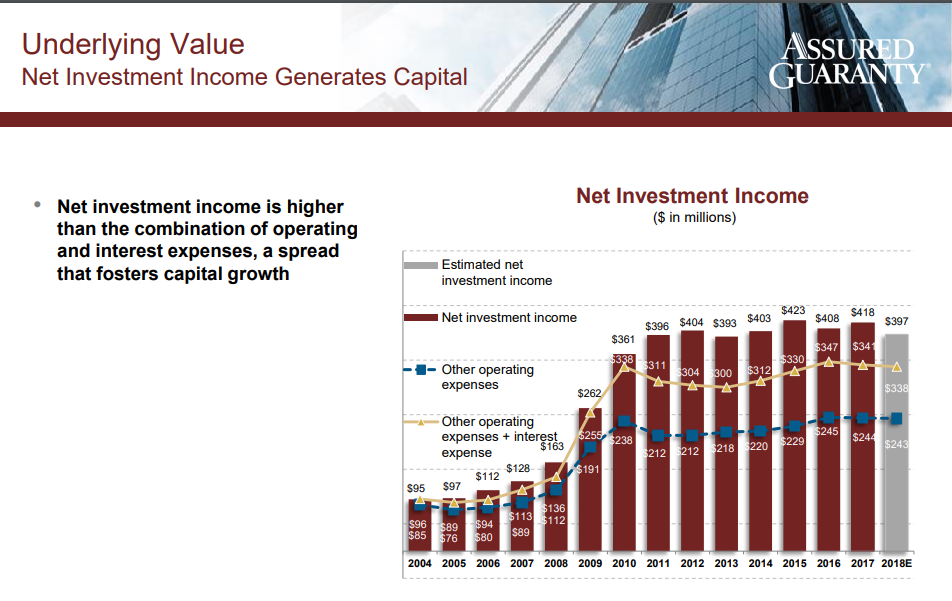

Higher interest rates are set to provide a nice boost to AGO’s investment portfolio over the long-term. AGO is the only company in its industry that generates a profitable spread between its annual investment income and its operating and interest costs. This spread fosters capital growth and while investment income is down a bit this year, it should grow as the company starts to grow the insured portfolio once again through new business production.

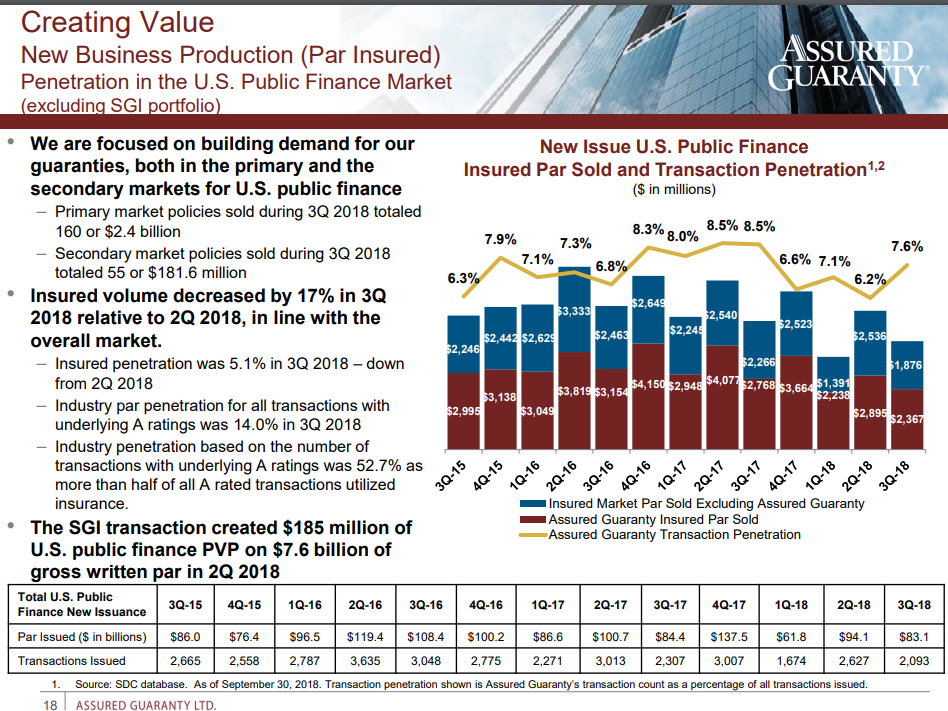

AGO is the leading U.S. municipal bond insurer and the company has made steady progress the last few years in increasing its new business production. The tax law change has negatively impacted issuance, particularly due to its impact on advanced refundings, but AGO has been very active in its target market of A rated transactions. When credit spreads widen, the savings that bond insurance provides increases and production could increase dramatically. In the pre-financial crisis world, there was annually $4-5 billion of premiums written on bond insurance. That was an era where several bond insurers were AAA rates, which enhanced the market opportunities, but if we could get half of that with higher rates, AGO’s insured portfolio could really see some geometric growth.

In addition to U.S. municipal bonds, AGO has once again built an attractive market with non-U.S. infrastructure bond insurance. AGO’s guarantees are an eloquent solution in that many infrastructure projects are 30-year endeavors. Instead of having banks finance the projects for 8-12 years and then having to refinance, the projects can lock-in rates to match the future revenue streams, bolstered by the stability that AGO’s guarantees provide. The company has been cultivating demand for these insured bonds finding yield-hungry investors across the globe including some recent deals that were purchased by some South Korean funds.

The smallest part of AGO’s new business is done in the Structured Finance arena. Management has been very careful focusing on providing capital relief to companies such as banks that are dealing with new capital requirement rules. The days of taking on substantial RMBS risk appear to be over, but the company does have an appetite to do various types of deals when the risk-adjusted returns are favorable, even insuring a CLO in the 3rd quarter.

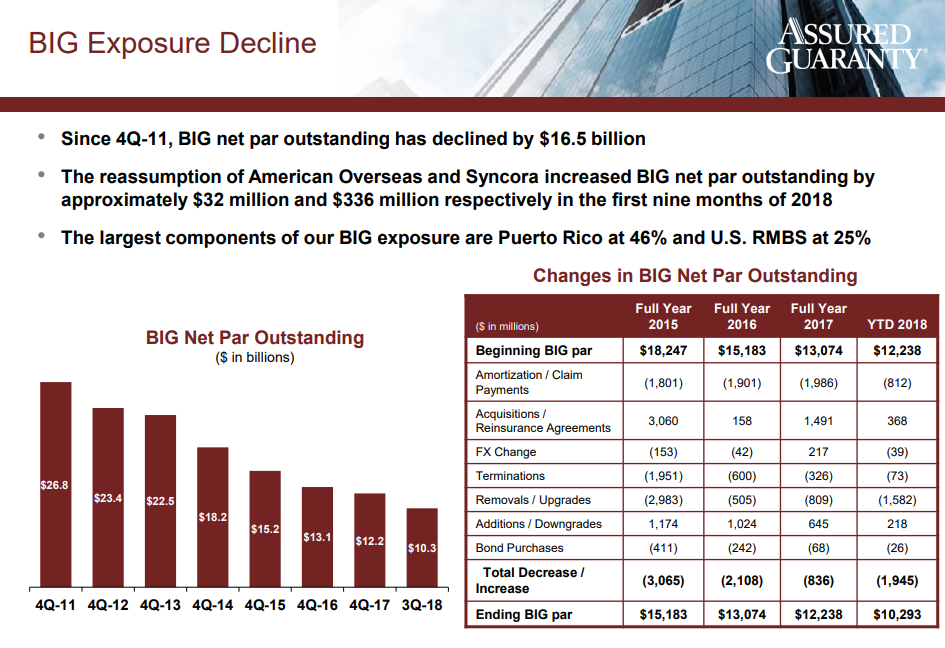

One of the areas that I spend a lot of time analyzing with AGO is its below investment grade net par outstanding. As you can see from the graphic above, ending BIG par is down to $10.293 billion, its lowest level in years. About half of that is related to Puerto Rico and another big chunk is legacy RMBS exposure that is covered by the rep and warranty settlements. AGO has a track record of being very conservative in its reserving policies, which has been exemplified in the releasing of reserves from its mortgage exposures.

On November 8th, AGO reported an extremely strong 3rd quarter with non-GAAP operating income of $1.47 per share, which was up 14% YoY. The company repurchased 3.3 million shares at a total cost of $130MM. The company insured $3 billion of insured par, generating $52MM of present value new business production, which was up 21% YoY. On a year-to date basis, which includes the large portfolio of business AGO assumed in the Syncora transaction in the 2nd quarter, AGO has produced $567MM of PVP. This number is far greater than any first three quarters since the company acquired AGM in 2009. Year-to-date, AGO has led with a 56% share of the insured new-issue par sold, totaling $7.5 billion of primary market par, which is 30% more than its nearest competitor.

There have been some majorly positive developments regarding Puerto Rico, which has been the biggest concern related to AGO. In October, AGO joined an agreement that ultimately should put the COFINA issue to rest. Senior Cofina bonds would see very strong recoveries in the $90s and the Juniors would recover in the mid-$50s. With judicial approval, this settlement would resolve about a quarter of Puerto Rico’s total capital market debt outstanding, saving Puerto Rico approximately $17.5 billion in debt service expense. AGO plans to wrap its share of the newly exchanged bonds, which will then be sold in the capital markets, further bolstering its recovery. One underappreciated aspect of this deal is that this frees up a lot of revenue that ultimately could be used to help recoveries on AGO’s biggest exposure, the GO debt, which carries that highest constitutional guarantee. Under the Constitution of Puerto Rico, GO debt must be paid before all other expenses. I believe recoveries should be in excess of 80 cents on the dollar and, they should recover par from a legal and economic standpoint.

On August 8th, the First Circuit Court of Appeals vacated the Title III Court order denying AGO’s request for relief from the automatic stay in relation to PREPA. This has allowed plaintiffs to file a motion to install an experienced professional to manage PREPA. This would be a great opportunity to improve the efficiency of the utility giant, which has been used as a political tool for far too long. There also is a proposed restructuring support agreement with some of the creditors, but the bond insurers are holding out for better terms. Remember, they have a secured lien on the net revenues of PREPA so recovery prospects are quite good.

In another major positive, the Oversight Board released a new fiscal plan in October that considers some of the dramatically improved economic data coming out of Puerto Rico and corrects some of the unrealistically morbid assumptions in previous plans. Puerto Rico has its lowest unemployment rate in its history and things are really improving rapidly, with further growth to come as more insurance money filters through the economy. The new plan projects a surplus through 2023 of $17 billion, which should be enough to cover the Commonwealth’s contractual debt service requirements during that period. There are still unrealistically negative assumptions as to Medicare Federal reimbursement and Act 154 multinational tax revenues that should be rectified.

A more realistic fiscal plan sets that stage for more settlements, which are in the best interests of everyone. Secured bonds are not something to be handled flippantly and debt must be honored. The COFINA debacle has already negatively impacted Chicago’s ability to monetize its sales tax revenue to issue new debt. It would be extremely naïve to assume that municipal markets aren’t watching the events in Puerto Rico very closely.

Puerto Rico must have access to capital markets to survive and ultimately thrive economically. The economy is doing very well with revenues growing. The problem with Puerto Rico has always been corruption and waste, which unfortunately their current governor has done nothing to resolve. It is up the Oversight Board and various courts to hold them accountable. On November 12th, there was an article put out by Axios Trump wants no more relief funds for Puerto Rico, saying that President Trump isn’t happy about what is going on in Puerto Rico. He is under the incorrect assumption that Puerto Rico is repaying creditors with Federal money, which is quite simply not the case. Creditors do benefit from a better economy in Puerto Rico, but they have gone years without payment. Puerto Rico has cash balances in excess of $10 billion, which should be used to repay contractual obligations and to fund essential services. It always strikes me as bizarre that natural disasters strike everywhere, but it is only Puerto Rico where politicians try to rationalize completely violating constitutions and contracts.

While the Axios article might show where the President’s head is at regarding Puerto Rico, there is a clear process in place to restructure the debt and a lot of the work has been done to start resolving these major issues. The sooner it is done, the sooner PR can access capital and attract additional investment. The whole island is an “Opportunity Zone”, so I’d expect many more billions of dollars to head its way to benefit from that favorable tax treatment. If the political climate gets even worse, creditors can assert their rights in Title III, appeals courts, and ultimately the Supreme Court.

At a recent price of $38.93, AGO trades at a 37% discount to its book value per share of $61.73. Unbelievably, the company trades at a 54% discount to its adjusted book value per share of $84.51. What is staggering about this book value growth is that it has come after years of adding loss reserves to deal with Puerto Rico, and more recently it has been negatively hit by rising interest rates reducing its AOCI, as other financials have seen too. This recent selloff provides a fantastic opportunity to buy back stock, further accreting value to shareholders. When I listened to the conference call and looked at the quarterly filings, I came away more optimistic on AGO than I have been in years. While the stock price is higher than it was earlier in the year, the outlook for new business has really improved, as have recoveries in Puerto Rico. Assuming those restructurings get wrapped up in the next year or two, AGO will have the clearest outlook in at least a decade.

AGO ended the quarter with 106.6MM shares outstanding. At some point next year, that number will drop below 100MM and in about 2 to 3 years, adjusted book value should be over $100 per share. Once AGO’s new business production or PVP, starts exceeding its earned premium revenues, adjusted book value growth will accelerate, as the unearned premium reserve grows. It is becoming increasingly likely that AGO will at some point do reinsurance deals with MBIA (MBI) and Ambac (AMBC) to help them free up capital, as they are no longer writing any new business. If those were to happen next year, you could see adjusted book value over $100 per share even sooner. Ignore headline risk and focus on the fundamentals of the enterprise. This is a fantastic opportunity to invest in AGO’s common stock.

Disclosure: I am/we are long AMBC, AGO.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment