“But I’m strong

Strong enough to carry him

He ain’t heavy, he’s my brother” – The Hollies

When a stock goes down day after day, in the face of what appears to be good fundamentals, there are two main possibilities. The first, there is a lot of bad news on the horizon and those in the know have started selling in bulk. The second is that it is moving away from fundamentals and due for a sizeable rebound.

In the case of Micron Technology Inc. (MU), we believe both those apply. Let us explain.

Future price trumps current price

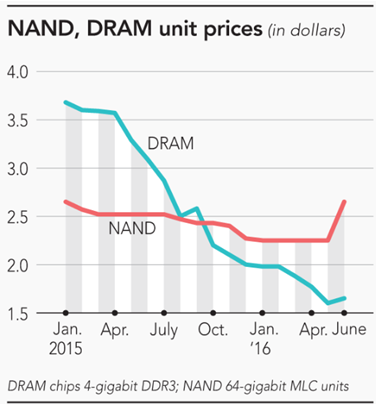

The stock market is forward-looking and nowhere is that more apparent in cyclical stocks like MU where the price of their products often top out and bottom out before the stock does. We saw that in the October 2014 top (prices peaked a little later) and the January 2016 top (prices bottomed in June 2016).

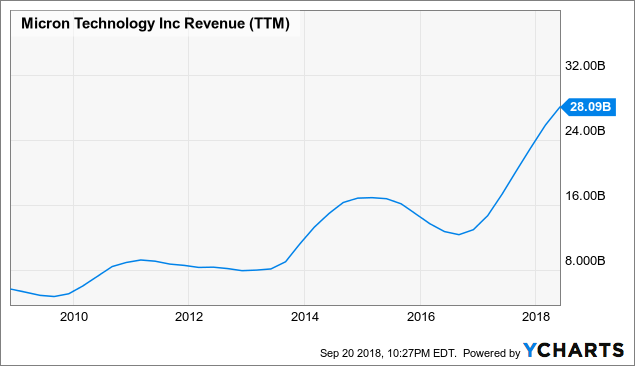

MU data by YCharts

This, of course, makes sense as profits evaporate rather rapidly in downturns for chip stocks and this is not a consumer staple to hold till you are old.

This, of course, makes sense as profits evaporate rather rapidly in downturns for chip stocks and this is not a consumer staple to hold till you are old.

The current downturn in the stock

We wrote our first article on this with the stock at $46/share and explained why the low P/E meant “diddly squat” (not to be confused with this guy). While we are not changing our tune on this, we believe the further $9 of decline represents an opportunity to go long.

The crux of the hard-core bear thesis (ours was more of a teddy bear kind) is that MU is slated for a quick and rapid free fall in profits and these should transition to losses rather quickly. Why else would they drive the stock down almost 40% from its peak?

MU data by YCharts

MU data by YCharts

One key facet that is being lost here is that DRAM prices have still not moved lower. DRAM forms the bulk of MU’s sales and while predictions have been coming in for some time, demand has been exceptionally strong.

Right direction, wrong magnitude, wrong trajectory

The stock is at $37.60 as we write this, bears have to not only be right about direction of the DRAM price move, but they also have to be right about the magnitude and trajectory. The reason is simple. For every quarter they are wrong about this, MU makes close to $3/share. Whether it buys back stock or simply holds the cash for better financial health in the next downturn, it should add to MU’s market value.

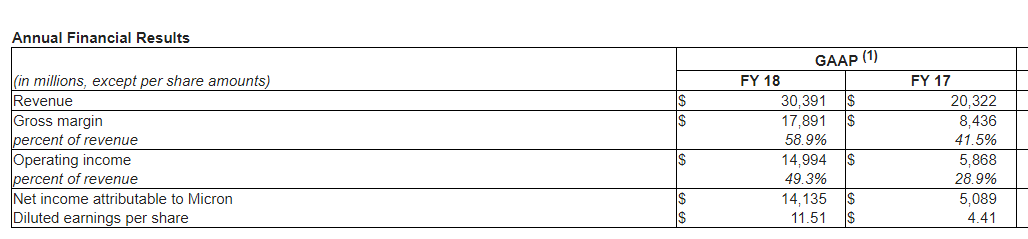

For a sensible downside case, the prices don’t have to just fall, they have to cliff-dive. As previously shown, MU’s revenues stay relatively constant during even downturns as bit growth helps keep it steady. While operating margin came in at a scintillating 48.9% for full-year 2018, it was at 28.9% just the year previously.

{kind=link}

Source: MU Q4-Fiscal 2018 results

Even if we assume prices fall quarter after quarter and MU reaches those margins in 12 months, on current revenues, MU should generate over $7.50 in EPS. Mind you this is the extrapolated run rate, four quarters out. In the interim, MU should generate close to $9-10 more in EPS. That is a very significant valuation that gets added to the current shares.

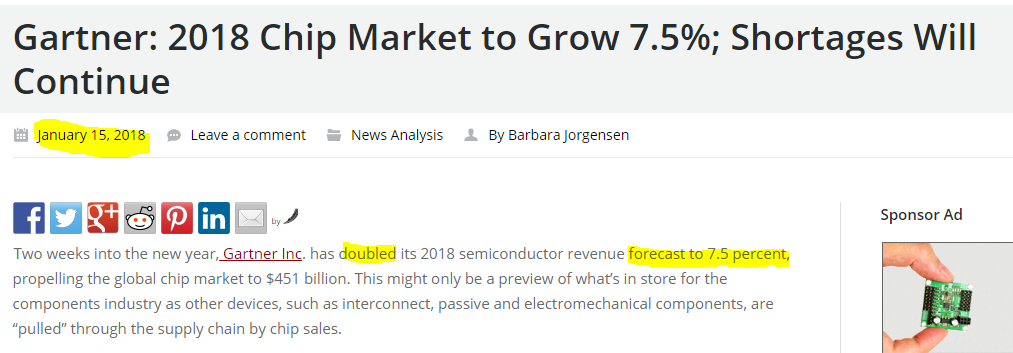

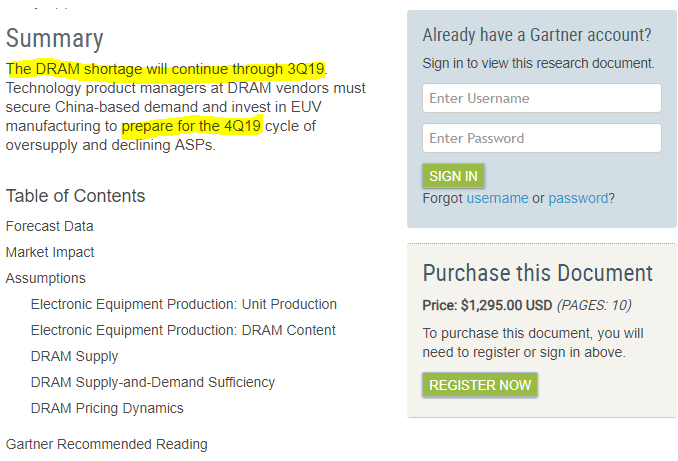

What has actually happened is that forecasts are being revised up instead of down. At the beginning of the year, 2018 was supposed to grow just by 4% and instead was revised up to 7.5%.

The “peak revenue” at the time was supposed to be in Q3-2018.

That timeline has faded away and the shortage will now persist till Q3-2019. You can get the full version if you pony up $129.50 per page.

Source: Gartner.com

From our point of view, the incongruence between actual numbers and expected numbers is rather extreme and it sets up a bottom.

Conclusion

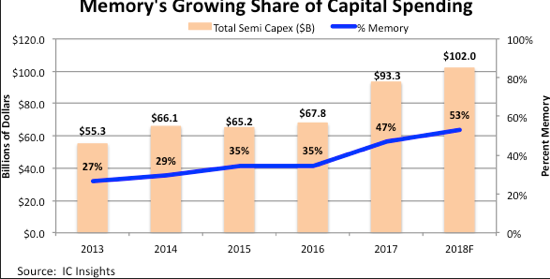

The supply additions are real. Those billions are not being spent to buy analyst reports.

The wafer additions in 2019 will be rather huge and the highest since 2007. The average selling point at this stage though tells us that demand continues to be extremely robust and bears are overestimating how rapidly things will take the downslope. We believe this is a high conviction tradable bottom with a wash-out sentiment.

Source: AlphaQuery.Com

For whom the price action has been a rather big glum spot we would say “It ain’t heavy, it’s a bottom.”

Whether it materializes into a longer term buy point will depend on whether the “oligopoly” is able to successfully defend its margins. Samsung (OTC:SSDIY), SK Hynix (OTC:HXSCF) did defer some capex plans and it will be interesting to see if they can actually, for once, proactively cut supply.

For more analysis such as this, along with real-time alerts on income stocks on both sides of the border along with ideas on how to prepare for the end of this bull market, please consider subscribing to our marketplace service Wheel of Fortune.

Disclaimer: Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints. Tipranks: Buy

Seeking Alpha has changed its policies. Previously “following” someone required a ritualistic commitment and an offering of not less than 4 oxen or 3 breeding horses. Now, all it takes is one click! If you enjoyed this article, please scroll up and click on the “Follow” button next to my name to not miss my future articles. If you did not like this article, please read it again, change your mind and then click on the “Follow” button next to my name to not miss my future articles.

Disclosure: I am/we are long MU.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment