Please note that I am affiliated with Avisol Capital Partners and their Total Pharma Tracker service. They have also covered the companies in this article in their writings, and I wanted to make readers aware of the potential for overlapping coverage.

Immunotherapy has become one of the hottest-ticket items in oncology over the past decade, and progress has been driven on numerous fronts, including antibodies, cell-based approaches, and cytokines.

At this point, antibody-based immunotherapy has shown the most potential, giving clinicians the opportunity to give “off-the-shelf” therapies that don’t require extensive processing. However, antibodies like the immune checkpoint inhibitors, for all the benefit they’ve yielded, continue to be plagued with relatively low response rates.

There’s room for improvement, and that’s what Affimed (AFMD) is trying to achieve. This German company has used a technology platform called ROCK to develop optimized antibodies that bridge the immune system and cancer antigens, with the hope of improving the standard of care.

Today, I want to take a deeper dive into AFMD’s developmental programs, as well as its financial situation, to give investors on the sidelines more information about whether this is a worthwhile investment, despite the recent volatility in valuation.

Clinical pipeline

AFMD sports a robust early-stage pipeline full of different immune cell-engaging antibodies:

Source: AFMD’s corporate presentation

AFM13

The most advanced of these developmental agents is AFM13, a tetravalent bispecific tandem diabody (TandAb) that simultaneously binds CD30 and CD16A. CD30 is a receptor that is expressed on activated immune cells, but it is most notable for its presence on tumor cells like anaplastic large cell lymphoma and classical Hodgkin’s lymphoma. The CD16A is a receptor found on natural killer cells, which are the body’s rapid defense against pathogens and abnormal cells.

By “ligating” the CD30 and CD16A receptors, you can force the NK cells to see tumor cells and mount an immune response. Activating the NK cells in this way has been an interesting mode of attack favored by several immunotherapy developers over the past few years, with Bristol-Myers Squibb’s (NYSE:BMY) elotuzumab being shown to mediate its anti-myeloma activity through NK cells.

To date, AFMD has completed one phase 1 trial involving AFM13 monotherapy in patients with CD30-positive lymphoma. The company reported favorable tolerability and activity via press release earlier this year, demonstrating a clinical response in two of three patients tested. Data from this phase 1 study are anticipated later in 2018.

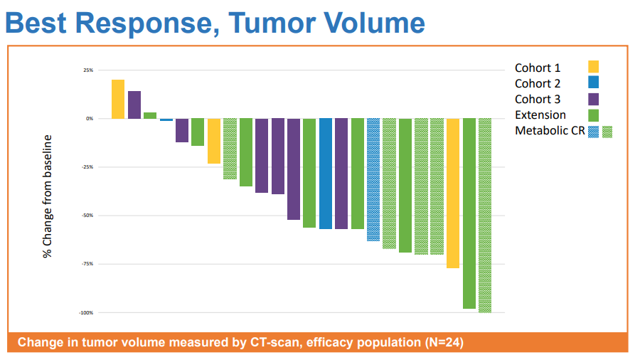

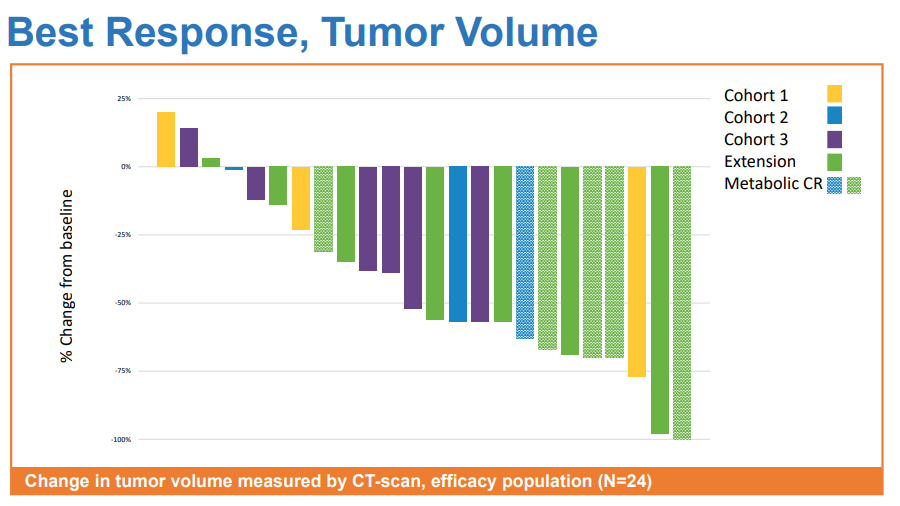

The press release also covered some findings from an ongoing collaboration with Merck (MRK) to assess pembrolizumab in combination with AFM13. This effort’s results were updated at EHA 2018 in Stockholm, with very intriguing responses observed:

Source: AFMD’s 2018 EHA poster presentation

This translated into a response rate that AFMD and its investigators viewed as favorable compared with past findings for pembrolizumab alone. AFMD has guided that it intends to have an update in the fourth quarter of 2018, indicating a potential presentation intended for ASH.

AFM11

The second most-advanced program in development by AFMD is AFM11, a TandAb that is bispecific for CD19 and CD3, which attentive readers will recognize as the same targets for Amgen’s (AMGN) blinatumomab, which was the first bispecific T-cell engager to be approved.

Unfortunately, AFMD decided to place a clinical hold on its two phase 1 studies in ALL and non-Hodgkin’s lymphoma due to toxicity concerns. One patient died from a serious adverse event, and two others experienced life-threatening toxicity.

It’s difficult to say right now what the outcome of the hold will be, considering these studies involved small numbers of patients. We can’t know yet whether AFMD will see it as valuable to continue the trials at this juncture, considering it hasn’t yet seen any efficacy data. That said, we have seen toxicity issues hamper other CD19-directed immunotherapies. In particular, blinatumomab carries a risk of cytokine release syndrome, which can lead to fatal complications.

AMV564

AFMD’s partner, Amphivena, is developing a bispecific T-cell engager called AMV564, which targets CD33, an antigen associated with acute myeloid leukemia (AML). You should note that CD33 is the same antigen target for the antibody-drug conjugate gemtuzumab ozogamicin, which Pfizer (PFE) hopes to make an important treatment option for the disease.

Amphivena presented initial phase 1 data at this year’s EHA meeting. At the time, 12 patients had been enrolled, 10 of whom had secondary AML and/or adverse cytogenetics, either of which can confer a notably poor prognosis for patients. AMV564 displayed no dose-limiting toxicity. In 6 of the 9 patients with evaluable disease, AMV564 led to blast reductions in the bone marrow, ranging from 13% to 38%, providing an early sign of efficacy.

In its latest corporate presentation, AFMD indicated that Amphivena also initiated a phase 1 study in myelodysplastic syndromes, but of course we don’t have any data yet for this indication.

Preclinical programs

AFMD is also working on a number of IND-enabling studies in its preclinical programs. This includes AFM24 and AFM26, which are both tetravalent, bispecific antibodies that coordinate NK cells to the site of tumor cells. AFM24’s main target is the epidermal growth factor receptor (EGFR), which is an important cell surface molecule in solid tumors like head and neck cancer (as well as a variant form, EGFRvIII, in glioblastoma).

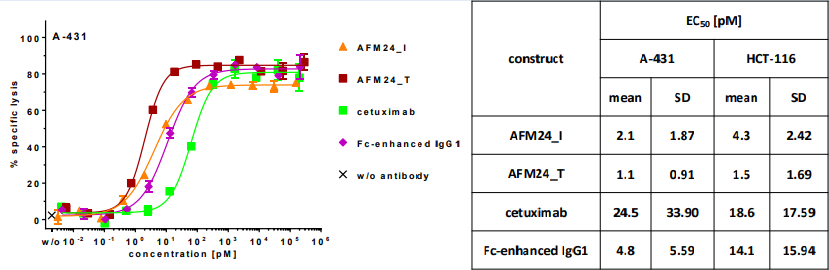

In a poster presentation at AACR 2018, AFMD presented some of its preclinical results showing efficacy of two AFM24 candidates in comparison with cetuximab, a monoclonal antibody that binds and inhibits EGFR.

Source: AACR 2018 poster presentation

AFM24 may prove to be a valuable contender in the immunotherapy space, with the added potential benefit of not significantly downregulating EGFR signaling, which could mean reduced class-specific toxicity associated with cetuximab and other EGFR inhibitors. For now, it’s unclear exactly which indications AFMD will pursue, but these preclinical data are encouraging.

AFM26 targets the B-cell maturation antigen (BCMA), which is an important emerging molecule of interest in multiple myeloma. Little surprise, then, that AFM26 has been characterized in preclinical models of myeloma. In a poster presentation last year at AACR, AFMD demonstrated encouraging activity against myeloma cells in terms of enhancing NK cell activity. This may be particularly relevant in myeloma, where stem cell transplantation is a key treatment option, and one where the rapid recovery of NK cells is an important component of reconstituting immunity and antitumor immunity.

Arguably, the most critical program for AFMD now is one we know very little about. The company announced a partnership with Roche’s (OTCQX:RHHBF) subsidiary Genentech to develop NK-targeted antibodies for various solid tumors and hematologic malignancies. That’s pretty much the extent of what we know, except for some of the financial arrangements, which will be discussed below.

Upcoming clinical catalysts

It is clear that most of AFMD’s development is centered squarely in the early stages. However, by broadening its pipeline, it’s given itself multiple chances for shots on deck into 2019 and 2020. Here are a few events that we can expect in the near future, per company guidance:

- Clinical trial updates for AFM13, including as a single agent and in combination with pembrolizumab

- IND filing for AFM24

- Initiating studies with Nektar (NKTR) combining NK cell-engaging antibodies with cytokine therapy

- Clinical update of AMV564 in AML

This is in addition to the ancillary benefits that could accrue if it achieves positive results. That could include regulatory designations or other licensing arrangements. I also fully expect that we’ll learn more about the fate of AFM11, for good or ill.

Financial information

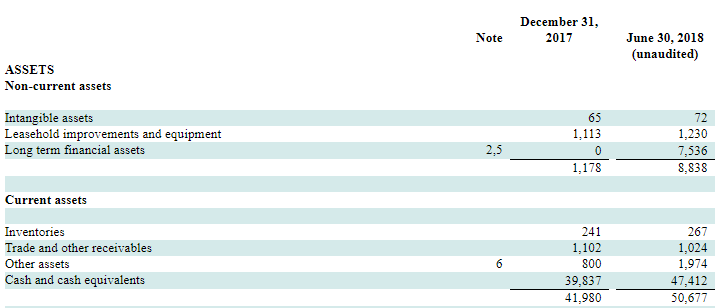

As of the latest quarterly filing, AFMD maintains cash and cash equivalents of 47.4 million euro, with another 7.5 million held in long-term financial assets.

This is checked by a net loss after taxes of 8 million euro, easily giving the company enough to meet its cash demands through 2019. Of course, in order to maintain an aggressive clinical pipeline, the R&D expenditures are going to need to increase, since clinical trials tend to get only more complicated and expensive as they’re pushed forward.

Thankfully, there is a decisive silver lining to the cash burn. AFMD and Roche’s (OTCQX:RHHBF) subsidiary Genentech entered into a research collaboration relating to develop NK cell engagers using AFMD’s ROCK platform. Not many details have been given about the scientific substance of the agreement, but we do know some of the financial terms.

For starters, Genentech provided a $96 million upfront payment, immediately moving the goalposts in terms of cash. Furthermore, AFMD is eligible to collect up to $5 billion more in developmental, regulatory, and commercial milestones, along with royalties on products coming out of the collaboration. The milestones related to development (which are the most important for the near term) total up to $250 million. We don’t quite know exactly what this refers to, as it could relate to initiation of phase 1 studies, or perhaps later time points.

At today’s burn (and exchange rate), this means that AFMD has a maximum of 17 quarters of cash in the tank to fund operations, which is quite a bit more than enough to quell any immediate financial issues for the near term. Milestone payments may well extend this runway even further, but we don’t know what the terms of that arrangement are.

Conclusions

In the case of AFMD, after a deeper analysis, it is clear that this is a company that has become de-risked in a number of ways. In particular, financially, AFMD is in the clear for the foreseeable future, given its collaboration with Genentech. Costs will continue to grow in terms of R&D expense as new products come to human study and advance in the pipeline, and it can be unnerving how quickly the cash runs out if pre-commercial biotechs become too loose with their spending.

However, to date AFMD hasn’t really given much indication that its spending will balloon out of control. Moreover, the acquisition of a licensing agreement with a $5 billion ceiling for a product in very early preclinical development (as far as we know) signals management is savvy in executing its shots on goal. If I were a shareholder, this would give me a lot of confidence.

So as I write this, AFMD trades at a market cap of $220 million, a small premium over its cash on hand. This means that the market is currently valuing its pipeline assets well under $100 million total. This, despite a $5 billion collaboration, encouraging early-stage data in Hodgkin’s lymphoma, and a large number of shots on deck.

So what gives? Certainly, the AFM11 clinical hold precipitated a fairly steep drop, from which the share price has yet to recover. So it seems clear to me that the market is currently taking this news as an imminent shutdown of the AFM11 program, and also that the market is extrapolating this setback to other clinical programs AFMD is working on.

I don’t think that’s appropriate, after taking a deeper dive into what the rest of the company has going on. The toxicity of AFM11 doesn’t come as a major shock, given the experience with CD19-directed immunotherapies that have reached the market. Furthermore, we’ve seen preliminary safety and efficacy for other AFMD therapies emerging out of the ROCK platform, most notably AFM13.

Given that, the market sentiment could turn on a dime with more favorable tolerability data from its other programs. Therefore, would-be shareholders currently sit on an important opportunity to get into AFMD. I don’t think the market is pricing this one very rationally.

That said, we need to acknowledge the very real risks of investing in an early-stage, pre-commercial biotech, no matter how good the results and de-risking look. It could still take a while before AFMD is able to gain results that prove definitive enough to validate its platforms; it takes time. Meanwhile, the money could continue to deplete. As always, caveat emptor when it comes to a company like this.

However, this is one company I would say you should take a serious look into, as there is a lot of potential to be made with a disciplined allocation. I think these prices are worthy of opening a position, while holding back some of your funds to see where it heads in the near term. It’s possible that the market continues to behave irrationally and drive the stock down further. This drop could also be precipitated or augmented by middling or bad news on any of the company’s clinical programs.

In conclusion, AFMD has a lot of encouraging features for shareholders, as well as considerable risk. However, the ceiling is extremely high at these levels, and if the company hits on some of its shots on deck (particularly with respect to its Genentech collaboration), then there’s no reason it can’t reach valuations pushing toward or over $1 billion.

That may take a good bit of time, but the company has bought itself several years to accomplish this. If you have a high appetite for longer-term waiting, this might be a company very much worth the invest-it-and-forget-it approach. In the near-term, there’s also a good chance for significant appreciation. Therefore, I feel it is well worth taking some time for due diligence.

Thank you for taking some time out of your day to read this article! If you liked what you see, I hope you’ll consider becoming a follower of mine on Seeking Alpha, as this will allow you to get real-time notifications when new articles of mine go live. Also, I want to let you know that I am a regular contributor to the Total Pharma Tracker, a marketplace service run by Avisol Capital Partners. If you want to join our conversations about biotech stocks, consider taking part in a free two-week trial today!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Be the first to comment