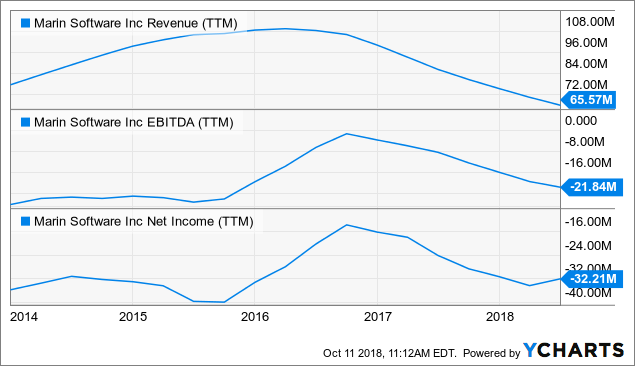

Marin Software (MRIN) is a provider of a SaaS ad management platform, which we featured half a year ago. It’s in a lengthy transition to a new platform (MarinOne) as its old business is losing money, lots of money as it happens:

The five-year development overview doesn’t inspire confidence either:

MRIN Revenue (TTM) data by YCharts

MRIN Revenue (TTM) data by YCharts

There are three traditional businesses:

- Search, which is their biggest business, where churn still outpaced new bookings, despite an upturn in the latter that started in Q1 and continued in Q2.

- Social, which was actually growing during Q1 due to reduced customer churn and increased customer spend.

- Cross-channel search and social revenue, up by 50% in Q1 and a further 36% in Q2, unfortunately, from a small base.

Turnaround?

Half a year ago, we had four reasons to see a possible turnaround in the company’s fortunes, and given that the shares were already very cheap then, any turnaround could lead to substantial share price gains. Here are these reasons, are they still valid half a year later?

- MarinOne

- Cost cutting

- Decline in R&D spending

- Increasing importance of cross-channel search and social revenue

The main reason to still see this as a possible turnaround candidate rests on their upcoming platform, MarinOne. This was formally introduced to the market on June 12 this year:

MarinOne enables the integrated management of search and social advertising, delivering significant incremental performance gains over traditional single-channel management tools. The MarinOne platform enables marketers to integrate all digital advertising data into one central platform, align campaigns across publishers to maximize ROI, and amplify publisher tools to drive the best possible performance.

We’ve already discussed the features of this upcoming platform in our previous article, here just a quick summary.

The main issue which Marin One is addressing is the fragmentation that makes it difficult to measure ad performance on different publishers, as many publisher, most notably of Google (NASDAQ:GOOG) (NASDAQ:GOOGL), Facebook (NASDAQ:FB) and Amazon (AMZN).

These walled gardens don’t share APIs and assessing relative effectiveness of campaigns across these platforms is difficult as a result. Here is management on the Q2CC:

For one, they don’t have access to the API data from their competitors and secondarily, it is not in their business interest to recommend if the next online advertising dollar might be best spent on a competing publisher. Given these realities, the need for an objective independent third party advertising management platform such as Marin’s is quite clear and growing.

MarinOne offers:

- Reporting and analytic tools to measure the effectiveness of ad campaigns.

- Execution tools that automate tasks across multiple advertising channels.

- Optimization tools that maximize revenue across multiple ad channels.

From the PR:

- Integrate: Many marketers are restricted to an inaccurate, myopic view of performance due to limitations and the closed nature of publisher tracking solutions, leading to suboptimal campaign performance. MarinOne makes it easy for marketers to use a wealth of first-party data to leverage more cross-channel insights, create and improve bidding rules, and manage eCommerce and product ads across multiple publishers effectively.

- Align: Google, Facebook, and Amazon have consolidated the customer journey, but they compete directly with one another and lack incentives to make advertising work as effectively as possible across channels. MarinOne provides an independent view of how these channels influence one another with the introduction of TruePath, a proprietary attribution technology that links device-level impression, click, and conversion data to drive accurate measurement, prevent conversion duplication, and optimize budget allocation.

- Amplify: To stand out, marketers need innovation on top of the tools provided by Google and Facebook. MarinOne allows marketers to sync campaigns to manage and expand efficiently across multiple publishers. Search Intent enables advertisers to target new customers on social using intent signals based on search queries. Powerful, AI-driven bidding completes the picture, delivering exceptional campaign performance.

Now, they’re not the only one to offer this. Apart from in-house solutions by publishers, there is competition from DoubleClick, Adobe Systems, (ADBE) and privately held Kenshoo, but Marin should make a useful addition. They are also introducing a fixed fee pricing model (Q2CC):

We also are seeing an ongoing uptick in cross channel new business and growing interest in our fixed fee platform pricing. We believe this shift from a percentage of spend model will prove highly disruptive in the marketplace and be well received by advertisers. This pricing model reduces the friction of integrating all advertising data into a single platform, enabling advertisers to easily adjust budgets, across channels to deliver the best advertising returns.

However, while they officially unveiled the new platform there were some further delays with regard to its actual use (Q2CC):

These daily efforts took us more time than expected and have moved our prior onboarding timetable back by about a quarter. As a result, we now expect to begin onboarding new customers to Marin 1 by the end of Q3 or early Q4 and also to have 75% of our monthly recurring revenue running on Marin 1 by the end of Q4.

You might also remember from the Q1CC that they already onboarded about 80 customers to MarinOne, representing approximately 44% of Marin’s monthly recurring revenue.

And this has us quite worried, to be honest. Even with half of their recurring revenues (we assume there was at least some further onboarding of existing clients during Q2) already on the new platform, they are still losing clients left, right and center.

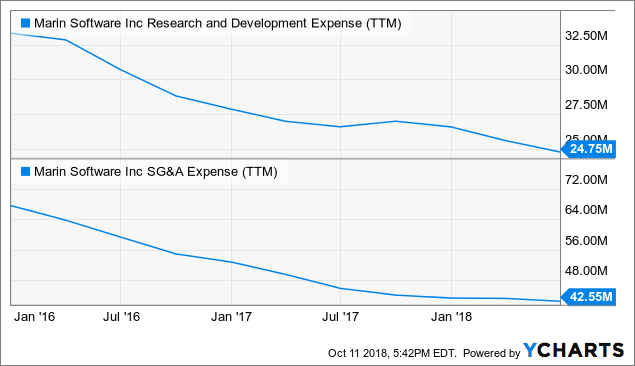

Cost cutting

The company is taking measures to reduce cost, but this is a running target as revenues also keep declining. The aim is to reduce cost by $10M a year, and in order to achieve this, headcount has been reduced from 433 to 335 in H1 2018; 40% of the remaining employees have technical roles.

We assume R&D cost will also decline further now that the MarinOne platform is sort of complete. Costs are declining in dollar terms:

MRIN Research and Development Expense (TTM) data by YCharts

MRIN Research and Development Expense (TTM) data by YCharts

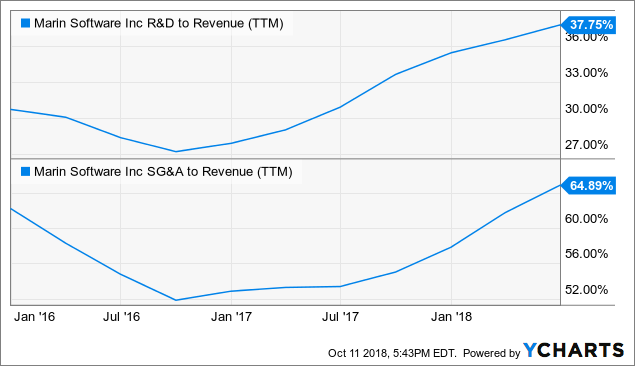

But they’re not declining nearly enough as revenues are declining faster:

Q2 Results and Q3 Guidance

Now, this can only have a happy ending if the decline in revenue stops. From the Q2CC:

our enterprise search business continued to face pressure as customer churn remained higher and outweighed new bookings. Although smaller by comparison, revenue from our social and display product offerings showed growth again this quarter.

A sympathetic view would argue that as the declining bits become smaller and the growing bits bigger, the decline should taper, and perhaps even reverse at some point.

It doesn’t look like we’re anywhere near that point as Q3 revenue guidance again implies a substantial sequential decline in revenues from $14.3M in Q2 to $12.3M-$12.8M in Q3.

Operating losses are not declining either, guided at $6.2M-$6.7M, from a loss of $6.2M in Q2 which was itself a considerable increase from the operating loss of $4.7M in Q2 2017. How long can they hold out?

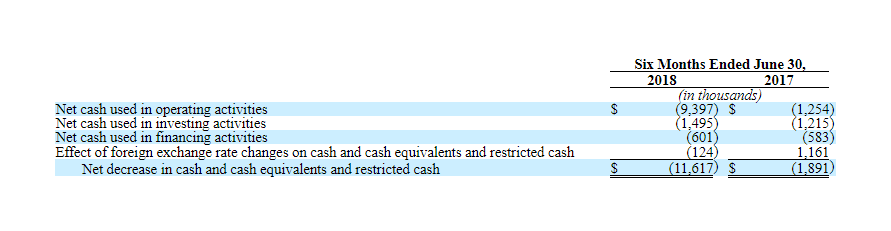

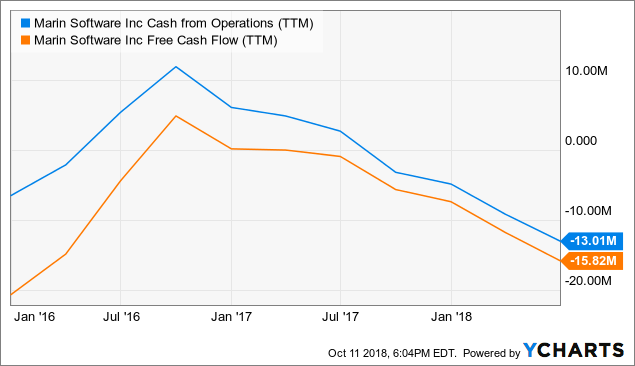

Cash

Cash flows have been deteriorating rapidly, despite the cost cutting. From the Q2 10-Q:

The company still had $17.2M in cash and cash equivalents, burning through $6.1M in Q2. In fact, that cash is almost as much as the market cap of the company, which tells you what investors think. Cash flows have been decreasing steadily with no turnaround in sight.

MRIN Cash from Operations (TTM) data by YCharts

MRIN Cash from Operations (TTM) data by YCharts

Conclusion

While Marin looks like an interesting turnaround with a potentially valuable SaaS platform which helps clients bridge the balkanisation of the ad world into different walled gardens, it’s in dire straits, and there is little to suggest a turnaround is actually imminent.

The situation has deteriorated from the last time we wrote about the company, with half of the revenue (probably more) already coming from their new platform which should be their new growth engine. There is little sign this has made a material difference as churn continues unabated.

True, the MarinOne platform is not yet open to all existing and new customers, and that will take until the end of the year. It’s also true that the company has some growing parts and still has cash for another two to three quarters.

The company could possibly get some additional finance to extent that if there are some signs that their strategy is actually starting to work.

But given the state of affairs today, we can’t recommend the shares, no matter how cheap they are, unless you really like to gamble and are not worried about the money put in. The shares are basically far out of the money options, right now.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Be the first to comment