Tesla Inc. (TSLA) is entering yet another critical time for the company. After last month’s bizarre “Funding Secured” Twitter takeover saga, followed by the announcement this month that the Department of Justice, in coordination with the SEC, is investigating the company, the company is focusing on trying to meet CEO Elon Musk’s committed targets to be both profitable and cash flow positive in quarters 3 and 4 of 2018.

I believe that the company is truly pulling out all the stops. However, I also believe they are using a substantial amount of “window dressing” to maximize these results. This article will illustrate some of these steps and where we can see them when the company publishes its Q3 financial results.

Q3 Profit

I won’t attempt to re-invent the wheel and project the quarter; there are too many other analysts who have done a far better job than I. I think it is safe to say that I am bearish on the company’s prospects so I want to try to put as many potential estimates up as possible for the quarter:

Source: Author Articles

All the authors have so far projected higher revenues than the current consensus, with a consensus view that Tesla is likely to miss this profitability target. Even in Cooper’s article, he notes there are risks on the Model 3 margin assumptions that could swing the company into a net loss for the month. I am partial to taking CoverDrive’s assumptions as he has a fairly strong track record and is roughly the mean of these projections. All note that the utilization and availability of ZEV credits can substantially impact the results positively, though these are now far from recurring as John Petersen outlined here.

Based on this, the quarter is certain to be a challenge.

Q3 Cash Flow

Tesla finished Q2 with $2.2B in cash. This amount had dropped to $1.69B by August 12 due to a $500m payment on its revolving credit line, according to the WSJ. I find it odd that the company highlighted this as it should be part of normal operations. Tesla’s history of disclosures is somewhat murky, recently describing receiving subpoenas from the SEC as “requests for information”. It could be the bank’s request this payment, but it could simply be a timing difference.

Of greater concern is the negative working capital hole of -$2.0B. This has largely been driven by a sharp increase in the company’s payables, which is starting to impact the company’s operations with a sharp increase in liens filed against the company. The company has also had difficulty getting access to car carriers, per this tweet:

This was contradicted in a Jalopnik article that indicated otherwise. There was also this interesting like by Daniel Faircloth, who runs LNR Auto Transport:

These examples show that the company has stretched some suppliers as far as they are willing to go; combined with the number of part shortages heard anecdotally, it is important for Tesla to have positive cash flow. .

The Quarter End Window Dressing

Sale-A-Thon

As I noted in my previous article, all companies do window dressing at quarter end in order to put forth the best possible result. Tesla is not different. However, based on a lot of anecdotal evidence, largely sourced and collated on Twitter from tweets copied to Elon Musk, I believe Tesla is pushing the envelope to achieve this goal.

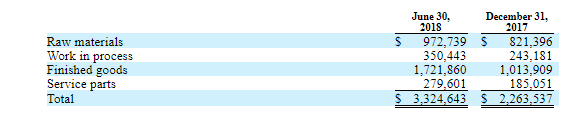

The company had a massive number of cars in transit at the end of Q2, with over 11k outstanding. It also had a giant build in finished goods inventories:

Source: Tesla 2018 Q2 10-Q

The company is prudently trying to move this inventory by any means possible:

- they had a sales event in early September to take cars that were already in inventory

- Offering free supercharging in exchange for purchasing a car

- Offering discounts to list price, a common quarter end practice

- Taking volunteer Tesla fans to help push car deliveries out

The volunteer component is a remarkable display by fans of the company trying to help it succeed. It also may open the company up to liability, in the event representations or work is done by these volunteers that are later questioned by customers. In fairness to Tesla, this is a risk that will be minor compared to others the company may face.

We should see a draw down in inventory based on these efforts; the company’s production rate has varied over the quarter but current estimates have it at 50 to 55k Model 3 in the current quarter. Cooper estimates deliveries of 59k, which would go a long way to reducing the inventory and harvesting the cash from these assets.

Some of these efforts may hamper the margins the company makes, impacting its result; free supercharging is definitely a cost that needs to be accrued, though not paid in the quarter. This would increase the accrued liabilities line, as it uses future costs to incentivize current sales.

Deposits and Deliveries

This is the area that I am somewhat concerned by. Tesla has a very large customer deposits line of $942m at the end of Q2; this has largely been secured (pun intended) by 420k Model 3 reservations. The company recently added an extra $2,500 configuration deposit that was required by holders as well, generating further cash for the company, though pulling revenue forward.

Twitter users @trumpery45 and @elonbachman, among others, review twitter for quality complaints, both through Elon Musk’s twitter account but also through reddit and Tesla Motor Club. I would encourage following them on Twitter as they include screenshots from many of these complaints. More recently, they have been highlighting some delivery issues Tesla has been facing. More and more reports are showing up through Tesla fan websites of full payment being taken by the company. Once payment is received, there is evidence of scheduled and cancelled car deliveries, missing cars and no VINs even being registered for customers. Cars also seem to be more readily available if payment is made by September 30, the end of the quarter, than if not.

This is very troubling for me. It is either the sign of incredible delivery incompetence and disorganization or Tesla is scrambling for as much cash as they can gather. The effect of these is we should see a massive jump in the customer deposits line. If cars are not delivered, this is where the cash should go. However, if they are aggressive from an accounting perspective, they could also show the cars as sold and remove them from inventory, even if they are not actually delivered.

These increased deposits, even if they are full payment for a car, will increase Tesla’s cash which is key for the company.

The Takeaway

Maximizing cash is always a good thing and levering your working capital is good business practice, assuming a strong capital structure. Tesla’s debt levels do not give it this strength as it has a substantial amount of total debt, with $230m due in November (after $82m that I have assumed Elon Musk rolled over in August), another $900m due in March that needs to be posted on December 31, as well $400m as a buffer for the ABL required on January 1. With these requirements, the company needs $1.53B just to meet the debt and covenant requirements to the end of the year. If we add in the working capital hole of -$2.0B at Q2 end, further impacted with reduced inventory, increased customer deposits, and further stretched vendors, we can see the pressure Tesla is under to minimize its cash burn. It has already reduced its capital expenditures for 2018 to an estimated $2.5B, which would require approximately $600m requiring funding in Q3, based on past performance.

If we take the best case scenario profit wise, we can assume a break-even operational performance. Lets assume the company is able to reduce its inventory by with Model 3 deliveries of 59k exceeding production by 50k (9,000 cars) with an average cost of $55k (assuming $60k sales price and 9% margins), this would generate ~$0.5B in cash. I have assumed no real change in Model S/X levels. I don’t believe the company can ring much more from its suppliers but lets assume an additional $200m in unpaid payables. With respect to deposits, let’s assume they can get 1,000 full deposits in advance or prior to delivery in the Q3, which would add $60m to the coffers. Putting it all together we have the following:

| Operating Performance | $0.0B |

| Add: Inventory recovery | +$0.5B |

| Add: Payables Extension | +$0.2B |

| Add: Deposits increased/retained | +$0.06B |

| Less: Capex | ($0.6B) |

| Total Cash Flow, Q3 | +$0.16B |

I believe this to be the best case scenario; however, it is possible, especially with the efforts Tesla has been putting forth. Unfortunately, I don’t believe this to be sustainable. Maybe the operating performance is but I don’t believe they can dodge the capex requirements as many are contracted amounts (ie Panasonic, Gigafactory, etc). They will have also burned through their inventory and further alienated their vendors, and potentially their customers if the delivery times continue to lag.

These efforts I noted above will give Tesla the best chance at meeting its Q3 cash goals. I have two major concerns though. First, these efforts will put them in a truly untenable situation in Q4, especially if their vendors start to exert pressure (COD, further mechanic’s liens, etc.). Second, with building evidence that Tesla is keeping customer money without providing the goods, it becomes a question on whether the company is doing this intentionally or due to logistical chaos. The resignation of its latest CAO in early September after just 1 month on a job gives me a lot of pause as to what could be going on with the company. It did coincide with the $420 takeover debacle, but he also had a job lined up within days of resigning, suggesting he started looking almost immediately, on top of leaving $10m in share comp on the table. By keeping the cars on the books, it would also enable Tesla to maximize the draw on its warehouse facility while also collecting deposits from their customers.

I do hope that this is not the case, but considering:

- Musk’s history of missed promises

- SEC investigations into Model 3 production disclosures

- SolarCity lawsuit over the true state of that company prior to Tesla’s takeover

- DOJ investigation into the taking private tweet

It is impossible to rule out.

This is the true crux of an investment in Tesla; can they survive this liquidity crunch to either ensure their operations are sustainable or to raise sufficient funds to give them a longer runway? I have my doubts.

A special thanks to the $TSLAQ community who have done an astounding amount of research and fact-checking of one another’s efforts into Tesla, notably @TeslaCharts, @Trumpery45, @elonbachman, @wintonCapPtnrs, @orthereaboot ,@paul_M_heuttner and the dearly departed Montana Skeptic among others.

If you see something in this article that you agree with, or even better disagree with, please take the time to comment below. This makes all of us better investors. I predominantly focus my investing in the small- and micro-cap company space but reserve the right to deviate from time to time, including short thesis. If you like what I’m doing, you can follow me by hitting the “Follow” button at the top of this article. Plus, you can follow me in real time by selecting that option.

Disclosure: I am/we are short TSLA.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I am short through a range of Put options expiring out to January 2020

Be the first to comment