Phillips 66 Partners (PSXP) delivered strong growth in earnings and cash flows in 2018 which fueled the dividend growth, and the master limited partnership will likely continue to do well in 2019 as it brings some major projects online. Phillips 66 Partners will grow volumes, earnings, and distributable cash flows which will pave the way for distribution growth. The MLP’s units will likely continue to outperform this year.

Image: Phillips 66 Partners LP, 4Q18 Investor Presentation.

In the last few years, Phillips 66 Partners has grown significantly after separating from Phillips 66 (PSX) to become one of the largest crude oil, refined petroleum products and natural gas liquids pipelines operators in the US. The volatility in oil prices continues to impact Phillips 66 Partners’ units but it seems primed to capitalize on growing US oil production.

The oil prices have swung wildly in the last few months, with the US benchmark WTI dropping from more than $75 a barrel in early October to $43 in December and have recovered to $58 at the time of this writing. The commodity averaged $65 a barrel last year but analysts are expecting an average oil price of $58.18 for 2019, as per a Reuters survey. The oil production in the US, however, will likely continue growing.

A number of US-based oil producers have slashed capital budgets for 2019 but they are still targeting production growth. For instance, Oasis Petroleum (OAS), which is one of the leading operators at the oil-rich Bakken play in North Dakota and Montana, will spend 40% less CapEx in 2019 as compared to 2018 but it will still deliver a 7% increase in oil and gas production. Pioneer Natural Resources (PXD), which is one of the biggest oil producers at the West Texas and New Mexico’s Permian Basin, will cut its drilling, completion, and facilities capital by 11% but will increase total production by 16%. Meanwhile, the big boys of the industry – namely Exxon Mobil (XOM) and Chevron (CVX) – have actually planned to increase drilling activity at the Permian Basin and will grow production at a faster pace.

The US has already become the world’s top oil producer, with domestic output climbing to over 12 million barrels per day, as per the US Energy Information Administration’s estimates. Although the agency is expecting a slowdown due to persistent weakness in oil prices, total output is still expected to climb by 1.3 million bpd in 2019 and 700,000 bpd in 2020. The growing output will eventually make the US the world’s top oil exporter as shipments to other countries double to 9 million barrels per day by 2024, as per the Paris-based International Energy Agency’s forecast.

This bodes well for Phillips 66 Partners which will have plenty of crude oil flowing through its pipelines. Last year, the MLP posted higher levels of earnings and distributable cash flows, due in part to high levels of pipeline and terminal throughput volumes. Phillips 66 Partners’ adjusted EBITDA increased by 51% to $1.14 billion while DCF climbed 49% to $854 million. Its pipeline volumes gradually increased from 1.8 million bpd in 1Q17 to record levels of 2.08 million bpd in 4Q18 while terminal volumes increased from 1.16 million to 1.3 million bpd in the same period.

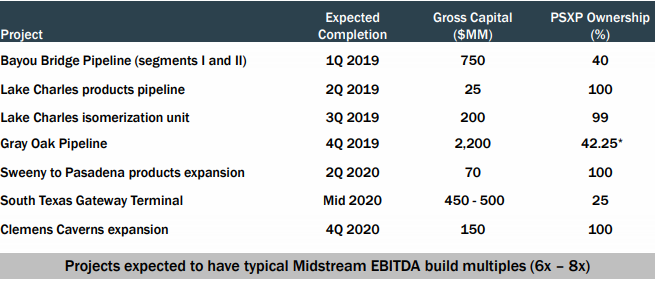

However, Phillips 66 Partners didn’t bring any major project online in 2018. Although the company finished expansion work on the Sand Hills pipeline in 2018 which increased the line’s capacity by 45,000 bpd to 485,000 bpd, that didn’t have any major impact on its annual results since the project got completed just three weeks before the end of the year. Instead, Phillips 66 Partners has been working on a number of projects which will start coming online from the current year, including the giant Gray Oak pipeline.

The Gray Oak, which connects oil producers at the Permian Basin and Eagle Ford with the Corpus Christi and the Texas Gulf Coast market as well as Phillips 66 Sweeny Refinery, is anticipated to be in service by the end of this year. Phillips 66 Partners owns 42.25% of the Gray Oak which has a capacity of transporting 900,000 bpd of crude oil. The line will play a major role in ending the supply bottleneck at the Permian Basin. Gray Oak will also feed Phillips 66 Partners’ South Texas Gateway Terminal located in Corpus Christi. This marine terminal, which is 25% owned by the MLP, will have two deepwater docks and a storage capacity of 7 million barrels and will start up by mid-2020. This will allow Phillips 66 Partners to tap into the lucrative export market.

Image: Phillips 66 Partners [link provided earlier]

Additionally, Phillips 66 Partners is also developing a 25,000-BPD isomerization unit which will serve its parent Phillips 66’s Lake Charles Refinery. The MLP will provide processing services under a long-term agreement with Phillips 66 with a minimum volume commitment. The isomerization will be placed into service in the third quarter of 2019. Phillips 66 Partners has nearly finished work on the extension of the Texas-to-Louisiana Bayou Bridge pipeline. The MLP and its partners extended the Nederland, Texas, to Lake Charles, Louisiana pipeline to St. James, Louisiana. The project, which is 40% owned by Phillips 66 Partners, will start up in the current month.

The startup of these new projects will lift Phillips 66 Partners’ volumes, earnings, and distributable cash flows in 2019 and 2020. This will justify another distribution hike.

Phillips 66 Partners is a great dividend stock which offers a decent yield of 6.5%, which is substantially higher than what investors will get with the dividend-paying companies in the REITs (avg. 3.78%) and utilities (avg. 3.45%) sectors. Phillips 66 Partners’ yield, however, is lower than the MLP industry’s average of 7.92%, as measured by the Alerian MLP Index. But that’s because Phillips 66 Partners offers some of the safest dividends among MLPs.

Image: Phillips 66 Partners [link provided earlier]

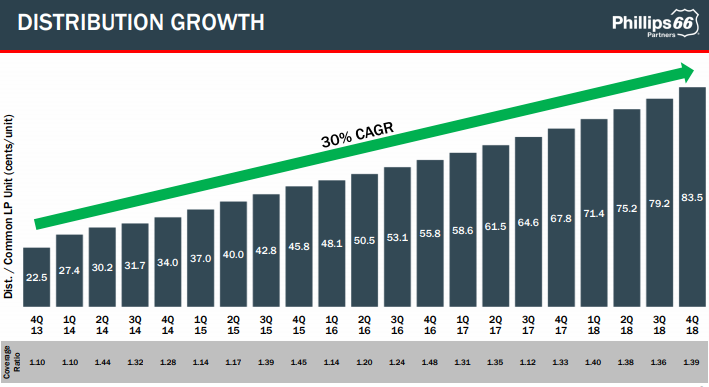

Phillips 66 Partners comes with a solid track record of distribution growth. The MLP has consistently grown its distributions since its inception in 2013 at an incredible CAGR of 30%. The growth has slowed in recent past as the company has gotten bigger but the 22.5% increase in distributions seen in 2018 compared with 2017 should still please unitholders. Moreover, the distributions are safe and sustainable since they are backed by fee-based cash flows, an attractive coverage ratio of well over 1x, and a rock-solid balance sheet.

Even though Phillips 66 Partners has been rapidly growing distributions, it has maintained a healthy coverage ratio. As indicated earlier, the company delivered $854 million of DCF which easily covered cash distributions of $618 million. As a result, the company ended the year with a strong coverage ratio of 1.38 times ($854Mn/$618Mn) or $236 million of DCF in excess of distributions. Furthermore, the company has $3 billion of debt which translates into a reasonable debt-to-EBITDA ratio of 2.8x which is below the company’s long-term target of 3.5x.

Units of Phillips 66 Partners have performed well this year, climbing by 22.6% on a year-to-date basis, easily outperforming the broader MLP space which is up 13% in the same period, as measured by the ALPS Alerian MLP ETF (AMLP). Phillips 66 Partners is well positioned to grow volumes, earnings, and DCF in the future as it brings major projects online which will fuel its growth. That’s going to drive distribution growth. I expect the company’s shares to continue to outperform. Investors should consider buying MLP’s shares while the distribution yield is above 6%.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The article is for information purposes only. It is not intended to be investment advice. The performance of Phillips 66 Partners stock is heavily influenced by movements in oil prices and other factors. Carefully consider your investment objectives, level of experience, and risk appetite before buying the company’s shares. Always perform your own research before making any investment decisions.

Be the first to comment