Nordea – it’s a second bank stock, and it may flounder short-term

In this article, I go to my roots of event-based article writing and show you, the reader, an article on the Scandinavian bank Nordea (OTCPK:NRBAY) (OTCPK:NRDEF). I will show you the banks profile and activities, it’s fundamentals and why I believe them to be appealing.

I will then go into why I believe that the current drop in valuation represents an opportunity to invest in this Bank, through one of two ways. I will show you why I believe the bank is investable at this price and why I believe you at the very least, should put Nordea on your watchlist and keep an eye on drops in the near future.

(Source: Nordea Homepage)

A quick overview and history

History for Nordea began in 1974 when state-owned PK-banken is created through a merger between Postbanken and Svenska Kreditbanken. This becomes the embryo of today’s Nordea. During the financial crisis of 1990, PK-banken acquired Nordbanken (which was in effect, failing) and during October of the year, the real estate company Nyckeln is declared bankrupt, causing a general collapse of other real estate and financial companies in the sector. This collapse would eventually pull larger banks, including PK-banken into its whirlpool, causing ripples across all of Sweden’s economy that would last for years, and give rise to newspaper headlines such as this one.

(Source: Dagens Nyheter Archive)

To clarify, there was a period during this crisis when the Swedish Central Bank due to the exchange rate collapses/FX speculation set the prime rate/key rate at 500%. It certainly was a time to be alive.

Credit losses of the time are estimated to have been upwards of 200B SEK (The historical SEK naturally having more value at the time). In 1995, following the crisis, the Swedish government introduced Nordbanken to the stock exchange and sold 34.5% of its ownership stake. In 1998, Nordbanken and Finnish bank Merita Bank merged, creating Merita-Nordbanken in a new, Scandinavian banking group. Little over 2 years later, Merita-Nordbanken merged with Danish Unibank, creating a merger with assets of roughly 1600B SEK. In succeeding fusions the same year with Christiania Bank and Kreditkasse, the new bank is made the largest in Scandinavia. As a result of these transactions and M&A, the governmental stake in the new bank was diluted to 18.1%.

The bank took the name “Nordea” in 2001.

Over the coming years, the Swedish government would decrease its stake in several companies, including Nordea. It completely left its stake in the bank in 2013, when it sold its remaining shares for roughly 20B SEK (Source)

Nordea today

(Source: Investor Presentation, Q4/FY18)

(Source: Annual Report, 2018)

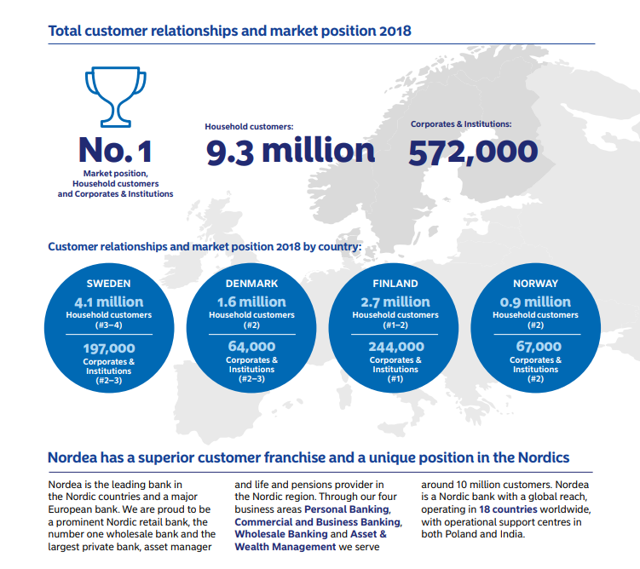

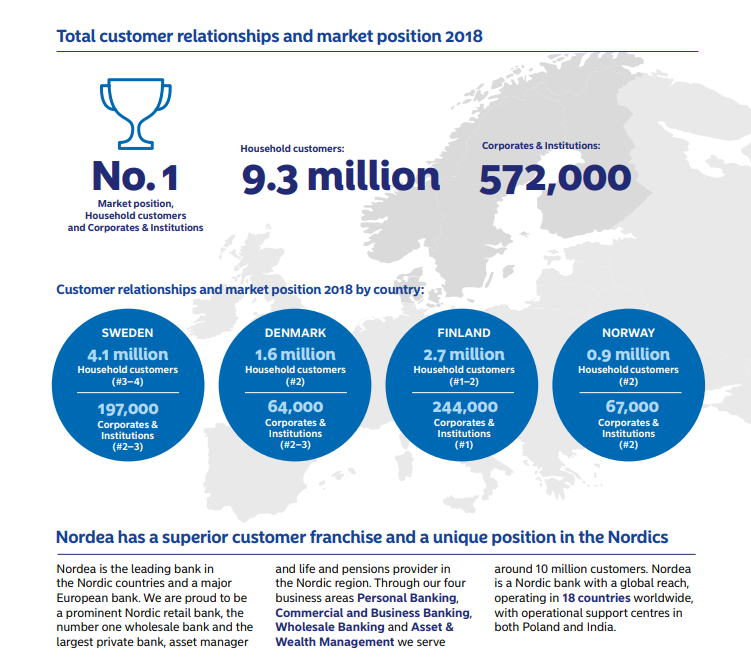

The bank has just delivered what I consider to be an acceptable FY18. It, as the largest financial services group in and the third-largest company in terms of market capitalization (€29.8B) in all of Scandinavia, serves approximately ~9.3 million household customers and 0.6 million corporate customers in key markets (Nordics). It has 450 branches and calls centers in all of the Nordic countries, and service key markets with a highly developed lineup of online and mobile banking platforms.

I wrote in my previous article about Swedbank(OTCPK:SWDBY), the bank, due to its nature has a competitive advantage in the Swedish/Scandinavian market due to the system integration that they’ve achieved over the past few decades, making themselves hard to replace for governmental organizations, and making them a primary choice for both household and corporate customers in the Swedish and Scandinavian market.

Well, the same is true for Nordea. The part of the market that isn’t taken by Swedbank, is taken by Nordea. This leaves very little for other banks in Sweden, such as Handelsbanken(OTCPK:SVNLY). Nordea is a first or at least second choice for many Swedish consumers, and a lot of us, including me, actually have accounts and services in several of the large banks at once. The Swedish banking oligopoly, similar to Canadas, comes with its own subset of characteristics – which are important to understanding if you mean to invest in the bank. Simply put – Nordea is part of Swedish banking culture, and it’s roots go deep into every portion of our system.

The bank has ~29000 full-time employees and currently has total assets of €551B, making it a major player in Europe and internationally, but the absolutely biggest player on the market in Scandinavia in Scandinavia.

(Source: Investor Presentation, Q4/FY18)

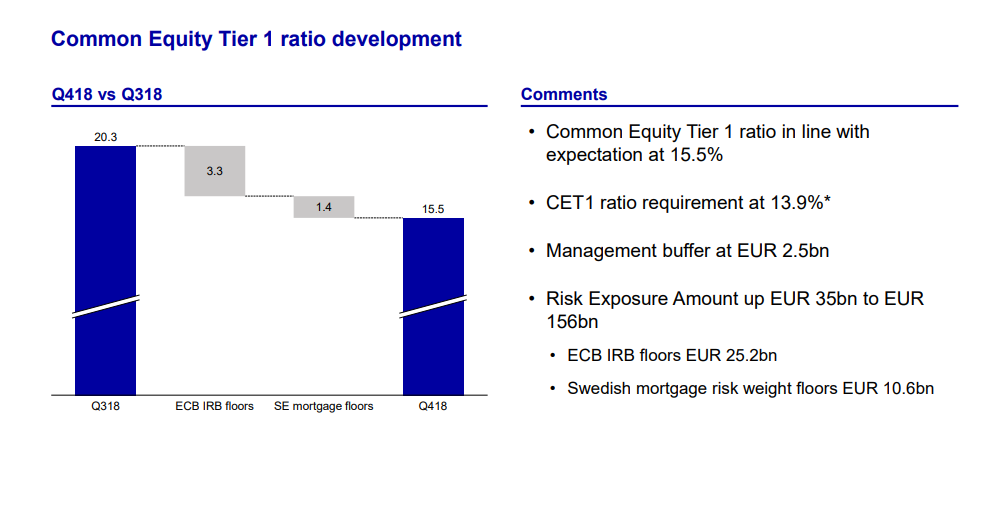

Nordea also has, like many European and all Swedish banks, an extremely conservative CET1 ratio, and is one of the few banks in Europe to achieve an AA credit rating from Fitch Ratings, and an a3 BCA from Moody’s (Source).

All in all and despite a partially-rocky road during 2018 with shifts in the workforce, reductions in spending and divestment of previously key business areas (private banking international), Nordea is one of Scandinavia’s strongest finance groups.

So, as with Swedbank – what’s happening?

Tonight, Finnish media/public service company Yle is going to be sending an episode entitled Nordea ja Kremlin pyykkärit (Rough translation: Nordea and the village cookers/chefs in Kreml) accusing the bank of laundering hundreds of millions of Euro in the latest line of money-laundering scandals in Sweden and Scandinavia.

The TV-show, MOT, has cooperated with an international consortium of journalists, the OCCRP, to obtain said data. The CEO of Nordea and the police chief responsible for the money-laundering unit will be participating in a TV-show tonight, at 21.00 GMT+1 in order to answer a question posed by the program – “Why is it possible to launder money in Finland?”.

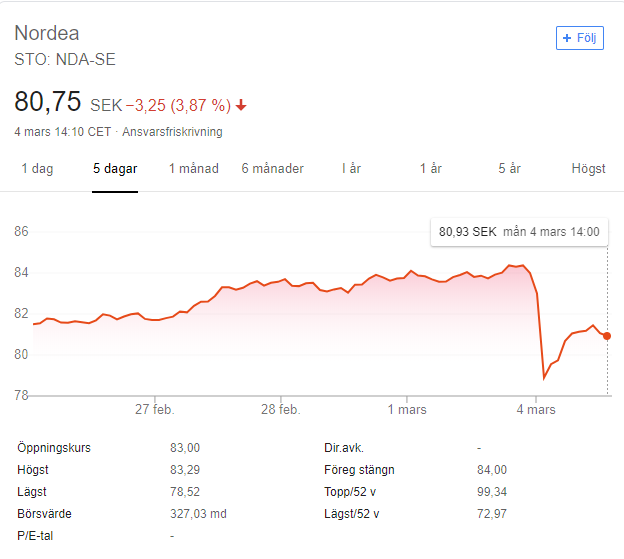

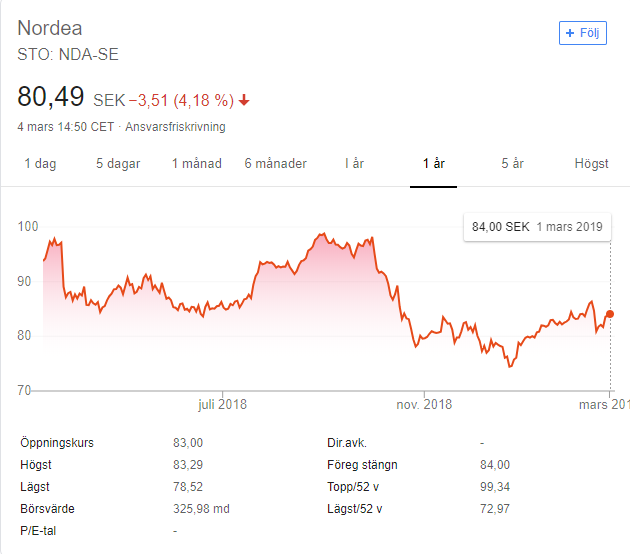

I want to emphasize that at this point, there is no evidence of any foul play or money-laundering done by Nordea. However, the stock has already reacted to the news.

(Source: Google Finance)

A 4%-drop may not be considered very much in this context, but it’s likely only a precursor to further drops over the coming days as the news regarding this story breaks. As with my article on Swedbank, my stance is that if the bank has indeed laundered money and the stock price takes a hit, you as the investor should be prepared to capitalize on this potential valuation opportunity.

The TV show says…

(Source: YLE MOT)

And so, the TV-shows has been published. Because the article wasn’t reviewed/submitted yet, I took the opportunity to go back in and edit things.

The leak, that’s been taken part of reveals the following:

- The leak consists of emails and corporate documentation

- It shows hundreds of billions of euro being moved back and forth between different accounts.

- The most important part of the material are transactions being made between Lithuanian banks Ukio Banka and Snoras. These banks have since lost their banking license.

- The material was released to international journalist organization OCCRP and Lithuanian news page 15.min.It.

- This TV program in Finland, MOT, is the only news office in Finland who’s been allowed to take part of the information.

- The leak shows approximately €700M being transferred to accounts in Nordea – much of it from accounts deemed suspect.

- Nordea’s customers during this time included 300 shell companies – the histories of which is dubious.

- 26 of these companies can be connected to the Magnitskij.

The fact seems that Nordea, in their role as the bank for these customers, should have paid closer attention to the people and companies they were doing business with. Tens of millions of euros in the transaction can be directly traced to people connected to Vladimir Putin and people known to be involved in money laundering scandals.

So. €700M worth of suspect transactions involving 300 shell companies between the years of 2007-2015. It’s similar, if not identical to Swedbank and Danske Bank. Now Nordea is being implicated as well. (Source)

What’s the opportunity?

(Source: Investor Presentation, Q4/FY18)

The bank has, as I wrote earlier, delivered an acceptable FY18. However, there are certain risks to factor in. Being smaller risks, I don’t consider them to impact the thesis in such a way as to change it or discourage from an investment in this bank – but they need to be exposed nonetheless.

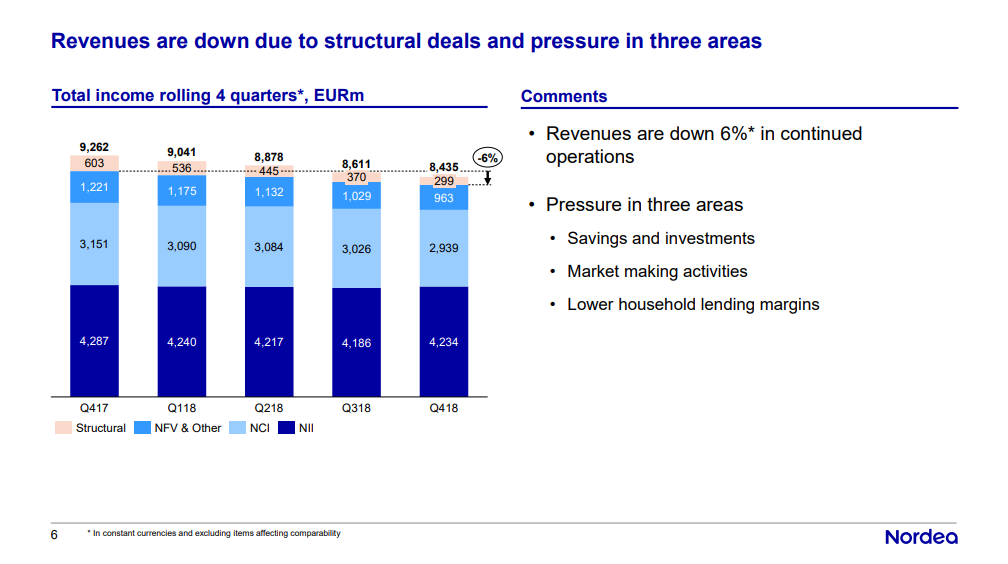

Bank revenues are down due to pressure (margins and otherwise) in areas of savings/investments, market making, and lending. Most Swedish banks face this, so this is nothing unique to Nordea. Nor is this likely to stop, as consumers are met with an increasing number of options for their banking and lending needs, in particular, the Millennial generation. The current job market and employment structure has created a need for new solutions with regards to credit and lending, and in this, I believe Swedish banks to be behind their Canadian counterparts.

(Source: Investor Presentation, Q4/FY18)

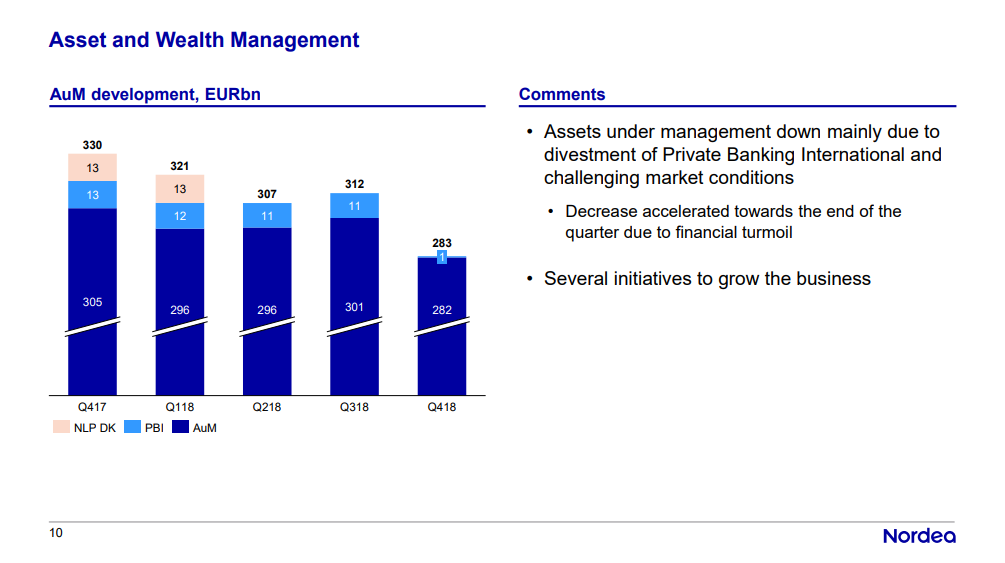

Asset and Wealth management posted abysmal numbers for 4Q18 as well, related to the company’s divestment of Private Banking international and challenges described as “general”.

(Source: Investor Presentation, Q4/FY18)

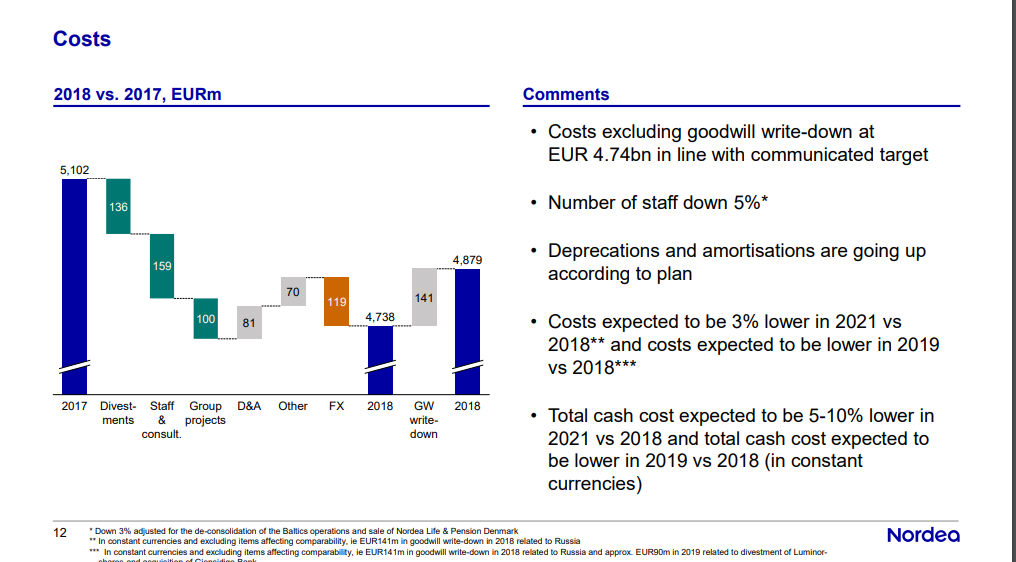

The bank is currently in the midst of a restructuring program aimed at cutting cash costs and unnecessary personnel. During 2017, the bank reduced staff by almost 6000 people, which for a company with 30 000 employees is a sizeable number. These cost-cutting endeavors will continue, aiming to make the bank more lean/streamlined. As of yet, however, we’re not seeing much of the effects of this streamlining.

All in all, Nordea has more things going on in terms of structural changes in comparison to Swedbank. They did not post the numbers that Swedbank did for FY18, and the bank’s share price history seen on a 1-year basis in part reflects this.

(Source: Google Finance)

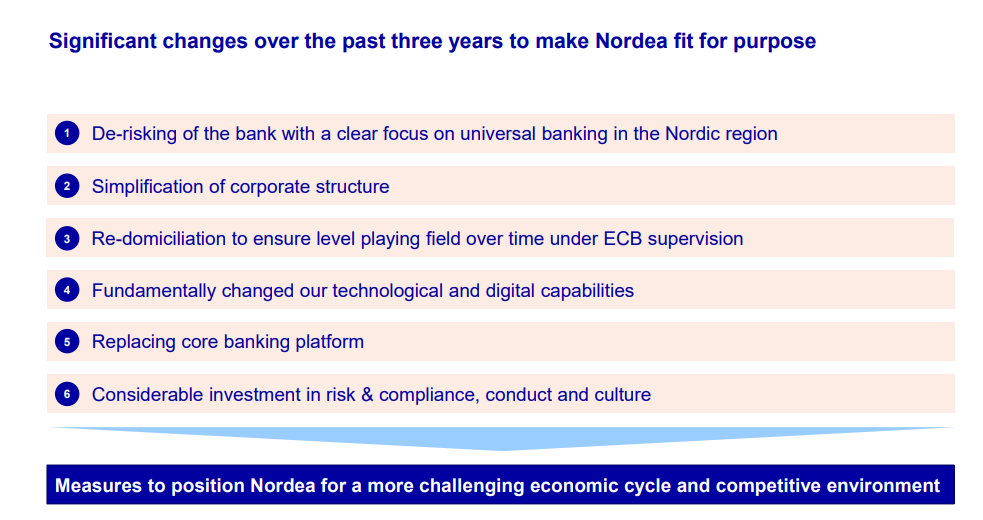

The bank’s goals for restructuring can be seen below, which in part addresses what the bank is being accused of doing.

(Source: Investor Presentation, Q4/FY18)

(Source: Investor Presentation, Q4/FY18)

The opportunity – Valuation and Stability

Despite the above-mentioned challenges, the opportunity here is, as most times, in terms of valuation.

(Source: Börsdata)

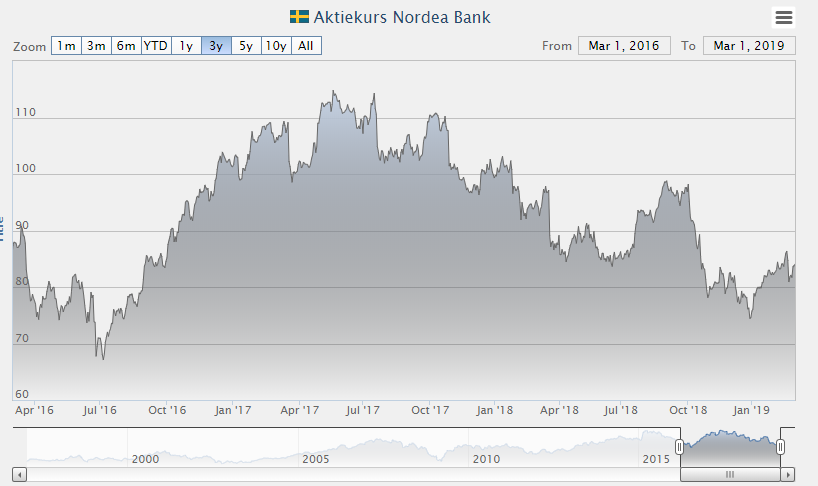

I argue that the opportunity is presented for an appealing entry into Nordea, and that entry is likely to grow even more appealing over the coming weeks as the story unfolds. On a 3 year basis, we’ve had share prices below 70 SEK – and it’s likely we could see these prices again.

(Source: Börsdata)

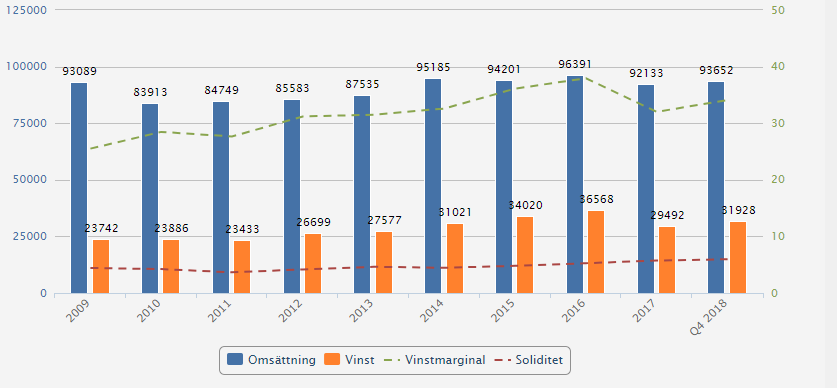

Nothing has changed with regards to the bank’s profit or revenues. The red flag is the payout ratio, which has grown from the mid-’40s to high-70’s and beginning to approach the 90’s. However, the bank’s margins are solid, even by Swedish standards, and they posted a profit margin rising from the already high levels of 32.0% during 2017 (Source).

(Source: Investor Presentation, Q4/FY18)

In terms of their own goals, Nordea has already managed to achieve several of them. They still have some way to go, and the negative impact on lending margins and with distinctly less return on invested capital than it’s peers, the bank has work to do in making their operations more efficient.

(Source: Annual Report, 2018)

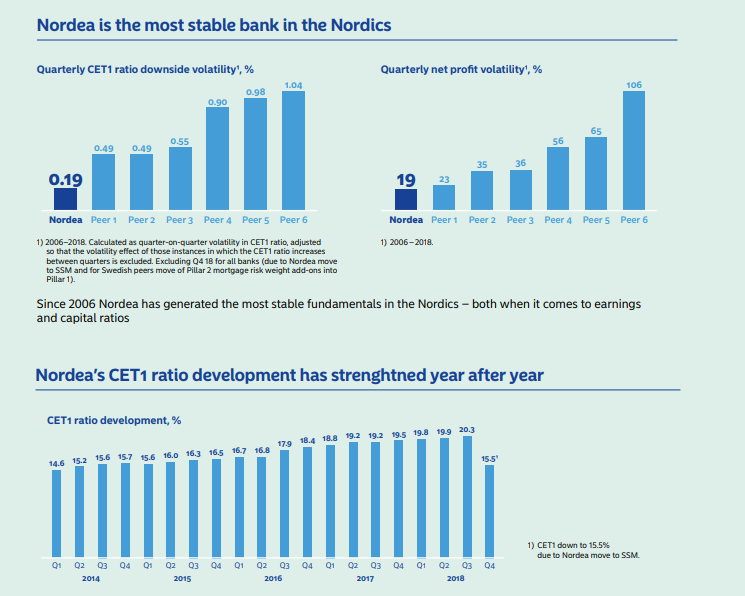

As I wrote in the previous section, Nordea is a very stable and risk-averse bank. Above we see some color to these claims, confirming their position as the most stable finance/banking group in the Nordics. This in itself is an argument which in my mind makes an investment into Nordea, if not a no-brainer, easily justifiable. There’s simply a lot of things working here, even including the allegations of hundreds of millions of euro in potential money-laundering.

(Source: Annual Report, 2018)

(Source: Annual Report, 2018)

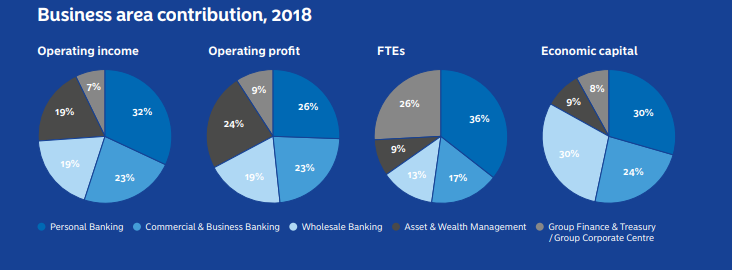

Additionally, the business areas that provide the profit for the valuation are well-diversified, with no area holding an overwhelming part of the business area contributions. Nordea is, in this, better diversified than it’s peers, who rely to a heavier degree on house lending/mortgages.

So, to summarize

Nordea is the largest financial group in the Nordics, with diversification into Norway, Denmark, Sweden, and Finland. It’s extremely well-capitalized and stable in relation to both its peers and from an international perspective. While it’s payout ratio may be high at this point, at an 8.8% yield, you may take a dividend freeze or cut into account and still come out on top.

The bank is about to become, and already to a certain point is, undervalued in relation to its performance and history (though historically, we can see a certain amount of stock price volatility). Furthermore, a coming report on money laundering which is broadcasted today, Monday, March 4th, 2019, is likely to put further pressure on the stock price.

This leads me to my strong belief that you should prepare to invest in Nordea. The bank, valued at P/E of 10.6, is valued slightly lower than their peers (apart from Swedbank), and this valuation is likely to drop further.

And this is how you can own Nordea

![]()

(Source: Sampo homepage)

Now, here’s where things get a bit trickier. I don’t own Nordea common stock directly – I instead own shares of Sampo Oyj (OTCPK:SAXPY)(OTCPK:SAXPF), which in themselves own roughly 21.2% in the bank, making it the largest shareholder by far. Sampo itself is then owned up to 10% by the Finnish State (Through Solidium), and to 4% by one of the largest Finnish private pension insurance companies in the nation. Sampo also grants me exposure to multiple insurance companies, through ownership of If P&C Insurance Holding Ltd, Mandatum Life Insurance Company Ltd, and Topdanmark, all of which are Sampo subsidiaries, and all of which are major players in the Nordic insurance market.

In short, owning the stock through major shareholder with a 6.5% yield grants me further diversification and lowers both my geographical and currency risk than owning the Nordea share directly. Sampo also owns 36.25% of Nordax, a leading, niche bank in Northern Europe.

Sampo’s Share mirrors Nordea’s development in part, and so today the share has lost almost 2% (at the time of writing the article). My cost basis on Sampo is, to put it simply, awesome. So awesome that at this time, investing in Sampo doesn’t really call to me, as my exposure to the company is already at its limit, and I feel that further Nordea share price depreciation may justify an investment in the common share itself. This especially because the common share provides an almost 2% higher yield.

It is my belief that you as an investor should consider the possibility of owning Nordea through Sampo, and the exposure it grants or owning Nordea stock directly.

Both of these are viable alternatives, and there are valid arguments for both ways here. Sampo’s stock at the current price is equally appealing, should you not already suffer from overexposure as I do. Even if you don’t want to own Sampo however, you should take a look at Nordeas common stock, as it could prepare to plummet further than today’s 3-4% once the story breaks.

I write this article to prepare you – and to tell you to watch the stock. As I will. I believe anything under a 10.8 P/E Valuation for this stock is investable, and though my own preferred cost basis for Nordea is closer to 70 SEK, it’s not impossible that it will reach these levels, and even current levels represent an excellent valuation.

Thank you kindly for reading.

Disclosure: I am/we are long SAXPF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment