I’ve taken a closer look at Mid-Con Energy Partners’ (MCEP) projected results for 2019 and 2020 at various oil prices. Mid-Con looks capable of generating a decent amount of positive cash flow in both years even if oil prices go a bit lower. However, its upside is also capped by its significant amount of hedges.

The outlook for 2020 may be slightly worse than 2019 (assuming the same oil price) as Mid-Con will need to deal with a full year of production from its high-cost Oklahoma acquisition as well as a slightly larger amount of hedges.

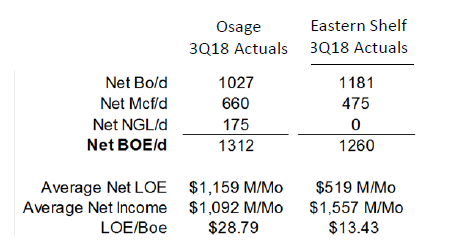

Notes On The Recent Transactions

One thing to note is that Mid-Con’s presentation shows three-stream production data for the Osage (Oklahoma) properties. However, as Mid-Con reports two-stream production data, the Osage properties may actually produce (based on Q3 2018) something like 1,210 BOEPD (85% oil). This would mean that Mid-Con’s projected 2019 production (at guidance midpoint) would be very similar (around 0.7% lower) than its Q4 2018 production, after adjusting for the effects of its transactions.

Source: Mid-Con Energy Partners

The change to two-stream reporting would also increase the lease operating expense to around $31 per BOE for the Osage properties.

Updated 2019 Outlook

I’ve tweaked Mid-Con’s model to reflect its lower (estimated at 90.8% during 2019) oil production due to the effect of its Oklahoma acquisition and Texas divestiture. Since its Oklahoma acquisition involves wet gas with high levels of NGLs, I’ve increased the estimated price it gets for natural gas in 2019 to $3.30 per Mcf.

This assumes that the acquisitions and divestitures close at the end of Q1 2019. Over a full year post-transactions, I’d expect Mid-Con’s oil percentage to be around 90% with a realised price of around $3.50 per Mcf for natural gas.

The revised model results in Mid-Con generating around $68 million in oil and gas revenue at high-$50s WTI oil in 2019, and around $66.7 million in revenues net of hedges.

| Barrels/Mcf | $ Per Unit | $ Million | |

| Oil | 1,192,445 | $55.00 | $65.6 |

| Natural Gas | 729,270 | $3.30 | $2.4 |

| Hedge Value | -$1.3 | ||

| Total | $66.7 |

Mid-Con’s cash expenditures remain at $57.1 million in this scenario, resulting in a projection of $9.6 million in positive cash flow in 2019 with its $9 million capital expenditure budget. EBITDA would be around $25.1 million including hedges.

One other thing to note is that Mid-Con’s lease operating expenses with a full year of the Oklahoma properties would be closer to $24 per BOE.

| $ Million | |

| Lease Operating Expenses | $29.6 |

| Production Taxes | $6.0 |

| Cash G&A | $6.0 |

| Interest Expense | $3.3 |

| Preferred Distributions | $3.2 |

| Capital Expenditures | $9.0 |

| Total | $57.1 |

2019 Results At Various Oil Prices

If we look at 2019 results at different oil prices, Mid-Con appears to be able to generate around $6 million in positive cash flow and $21.5 million EBITDA at $50 WTI oil. At $70 WTI oil, it would generate around $30.7 million EBITDA and $15.2 million in positive cash flow.

A $5 change in oil prices affects Mid-Con’s EBITDA and cash flow by around $2.3 million in 2019. This is after hedges, as without hedges Mid-Con’s cash flow and EBITDA would change by roughly $5.5 million with a $5 move in oil prices.

| WTI Oil Price | $50 | $65 | $70 |

| EBITDA ($ Million) | $21.5 | $28.4 | $30.7 |

| Cash Flow ($ Million) | $6.0 | $12.9 | $15.2 |

A Quick 2020 Model

If Mid-Con’s production stays at 3,600 BOEPD in 2020, its oil percentage may go down slightly to 90% with a full year of production from its newly acquired Oklahoma assets.

This would result in Mid-Con generating around $67.8 million in oil and gas revenue in 2020 if we keep benchmark prices the same (roughly $58 WTI oil). Mid-Con has hedged a slightly higher volume of oil in 2020 at slightly lower prices, and after hedges it may generate $66.3 million in revenue.

| Barrels/Mcf | $ Per Unit | $ Million | |

| Oil | 1,182,600 | $55.00 | $65.0 |

| Natural Gas | 788,400 | $3.50 | $2.8 |

| Hedge Value | -$1.5 | ||

| Total | $66.3 |

Mid-Con’s cash expenditures would increase slightly to $58.6 million in this scenario due to the full year of production from the new Oklahoma assets. This assumes that Mid-Con is not able to meaningfully reduce costs compared to 2019 though, so there may be some upside there. I’ve also assumed that $9 million in capital expenditures will keep Mid-Con’s production at 3,600 BOEPD.

| $ Million | |

| Lease Operating Expenses | $31.5 |

| Production Taxes | $5.9 |

| Cash G&A | $6.0 |

| Interest Expense | $3.0 |

| Preferred Distributions | $3.2 |

| Capital Expenditures | $9.0 |

| Total | $58.6 |

In any case, if nothing else changes, Mid-Con would generate around $7.4 million in positive cash flow in 2020, down slightly from the $9.6 million projection for 2019. At $70 WTI oil in 2020, Mid-Con would generate around $12.1 million in positive cash flow using the other assumptions listed above.

Conclusion

After adjusting the Oklahoma acquisition to two-stream reporting, it appears that Mid-Con is expecting to keep organic production essentially flat with $9 million in capital expenditures. Mid-Con’s oil percentage may go down to around 90% by 2020 though, while its lease operating expenses may go up due to a full year of production from its new Oklahoma properties.

Mid-Con should be able to continue to generate a fair bit of positive cash flow in 2020, even if it doesn’t meaningfully reduce its costs. However, hedges will continue to limit its results. At $70 WTI oil, Mid-Con would be able to generate $22.1 million in positive cash flow without hedges, but only $12.1 million with hedges. Production growth would reduce the relative impact of the hedges, but it appears that significant production growth will need to wait until its credit facility maturity and preferred units are resolved.

Free Trial Offer

We are currently offering a free two-week trial to Distressed Value Investing. Join our community to receive exclusive research about various energy companies and other opportunities along with full access to my portfolio of historic research that now includes over 1,000 reports on over 100 companies.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment