HCP, Inc. (HCP) is an attractive income vehicle for dividend investors, but only if the price and risk/reward are attractive. HCP benefits from an aging U.S. population and rising healthcare expenditures, and has a strong portfolio and moderately attractive dividend coverage stats. That being said, though, the valuation is stretched, which exposes new investors to downside risks. Investors may want to wait for a drop before gobbling up some shares for a high-yield income portfolio.

HCP – Portfolio Overview

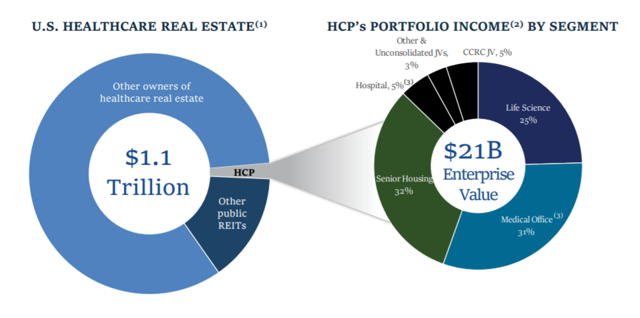

HCP is a dominant player in the U.S. healthcare industry. The company has large investments in senior housing properties, medical office buildings, and life science facilities. At the end of the December quarter, the healthcare REIT’s real estate portfolio was comprised of 744 properties (including joint venture facilities).

Here’s a portfolio snapshot by asset type:

Source: Q4-2018 Earnings Supplement

Medical office buildings represented 29 percent of the REIT’s portfolio income in the fourth quarter, followed by life science buildings (25 percent), and senior-housing facilities (23 percent). HCP produces ~$288 million a year in portfolio income from its mix of senior-focused healthcare facilities.

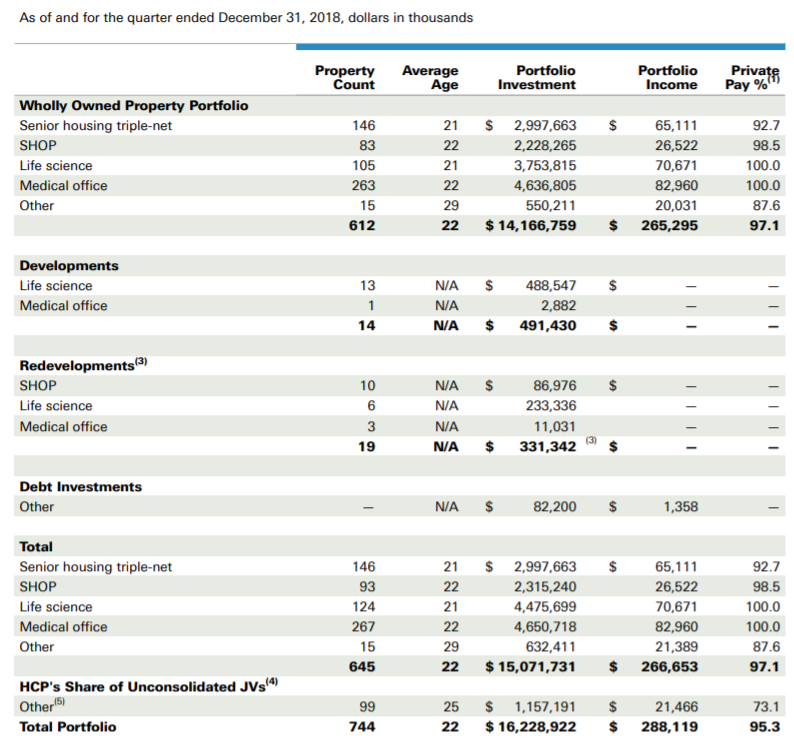

Here is a more detailed breakdown of the REIT’s property portfolio:

Source: HCP

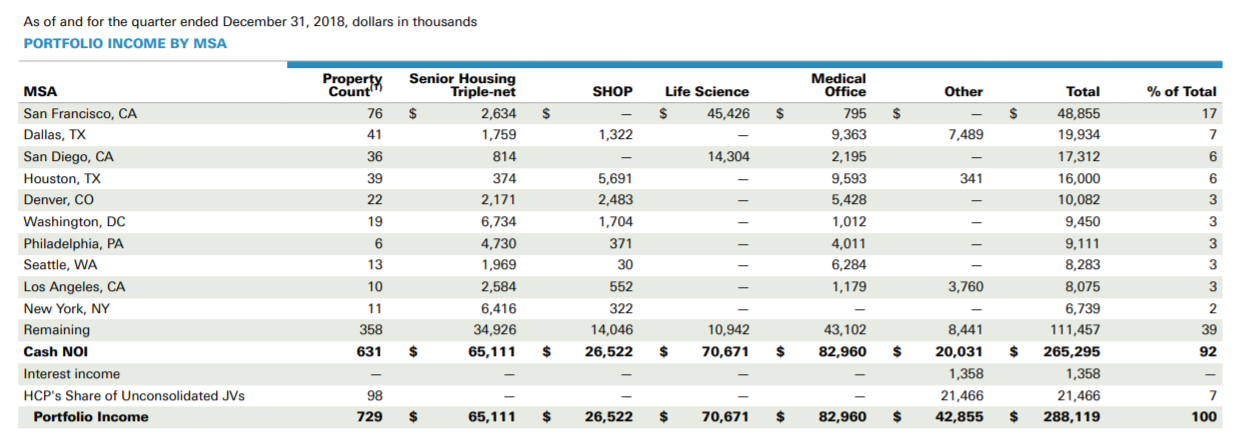

HCP’s properties are spread out across the United States, but are nonetheless concentrated in major urban areas. San Francisco and Dallas are the two most important cities for HCP, consolidating 17 percent and 7 percent, respectively, of the REIT’s real estate investments.

Source: HCP

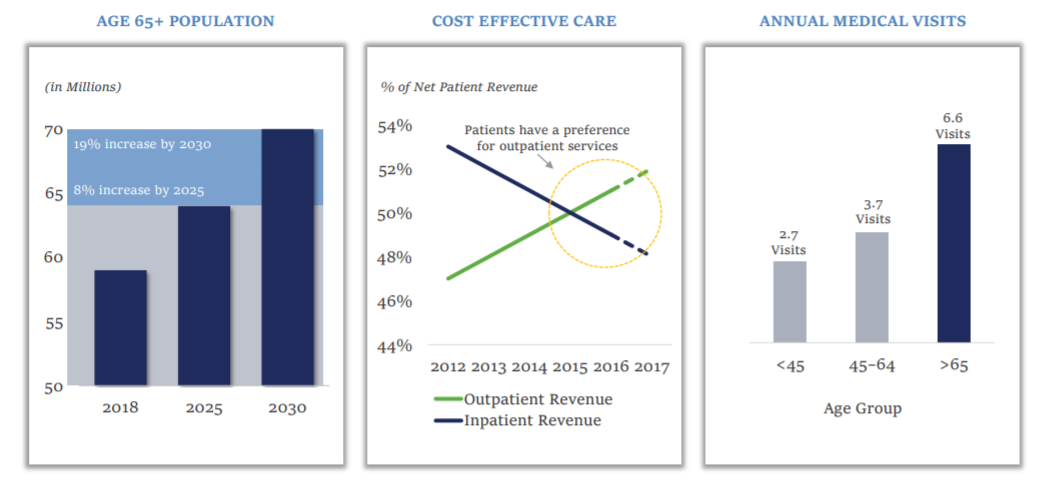

Two major trends generally support the investment thesis in HCP:

1. The U.S. population is aging at a rapid clip. Elderly demographics (65+ age cohorts) are going to make up a larger share of the U.S. population going forward.

2. Patients are demanding more cost-efficient outpatient procedures than in the past.

Source: HCP

Source: HCP

HCP benefits from these long-term trends in the healthcare industry through its diversified facility portfolio.

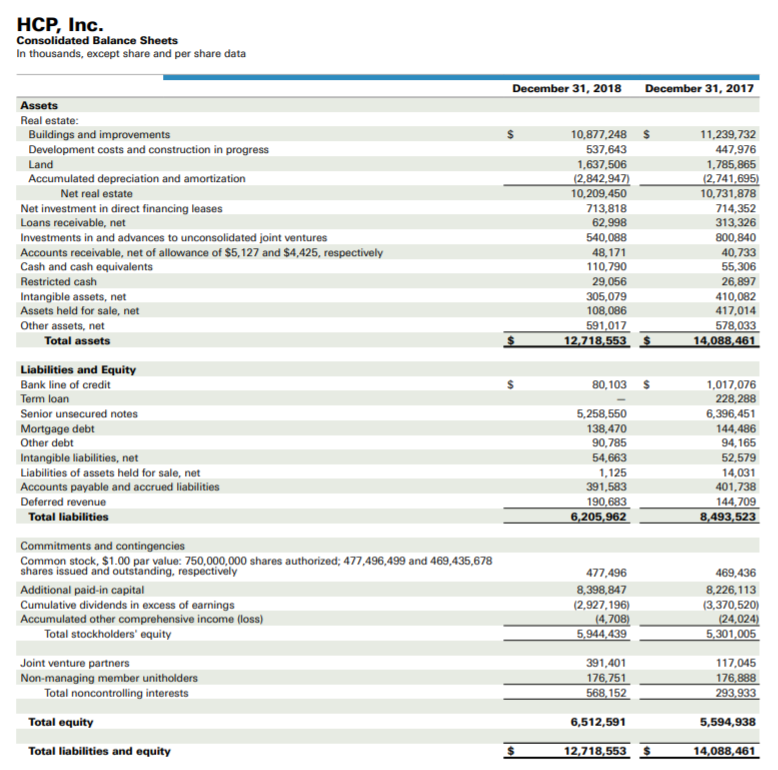

Balance Sheet

HCP has an investment-grade balance sheet that adds another layer of protection in the event of an industry downturn or a U.S. recession. HCP has investment-grade credit ratings as follows:

- S&P: BBB+ (Stable)

- Moody’s: Baa1 (Stable)

- Fitch: BBB (Positive Outlook)

Here’s the latest balance sheet:

Source: HCP

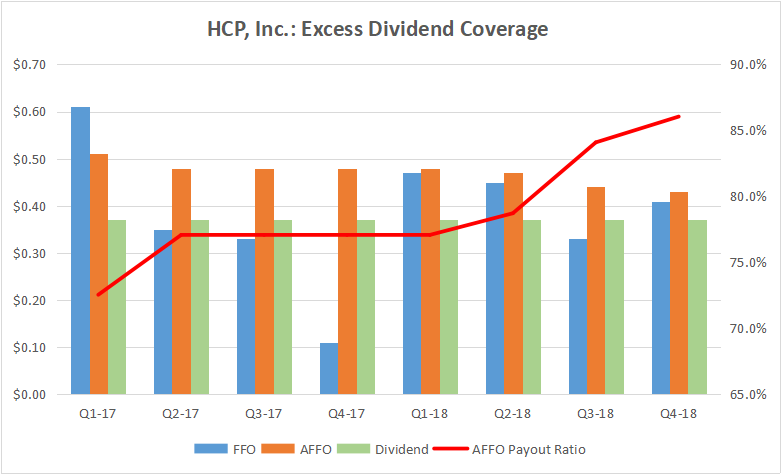

Distribution Coverage

HCP managed to cover its dividend payout with FFO and AFFO, on average, in the last eight quarters. The healthcare REIT pulled in an average of $0.38/share in FFO and an average of $0.47/share in AFFO in the last eight quarters, which compares against a stable quarterly dividend rate of $0.37/share. The AFFO payout ratio has averaged 78.7 percent, but has increased rather consistently in the last two years.

Source: Achilles Research

HCP does not currently grow its dividend, which is why the healthcare REIT would be an unsuitable investment for DGI investors. The yield is moderately attractive, but investors should not expect the company to change its dividend payout policy going forward.

Data by YCharts

Data by YCharts

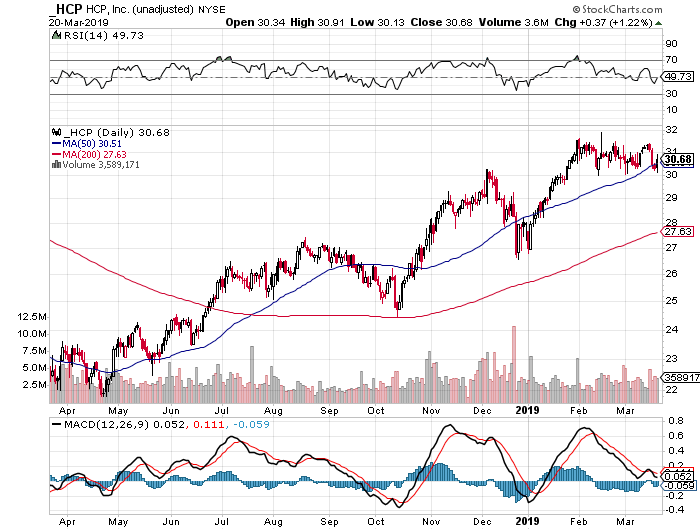

Valuation

The share price has recouped all of the losses sustained during the sell-off in December, and then some. Year-to-date, HCP’s share price has risen 9.9 percent.

See for yourself.

Source: StockCharts

Today, HCP’s dividend stream is quite expensive, in my opinion. Since shares change hands for $30.68 at the time of writing, an investment in the healthcare REIT effectively costs income investors ~17.8x Q4-2018 run-rate AFFO, which is a high multiple to pay for a REIT that doesn’t grow its payout.

Risk Factors Investors Need To Consider

The high valuation multiple is a reason for concern to me: HCP’s share price has surged in the last couple of months, exposing investors to growing correction risks. While I don’t think that the dividend is at risk over the short haul, the valuation is stretched, implying an unattractive risk/reward for new investors.

Your Takeaway

HCP benefits from long-term trends in the healthcare industry. The healthcare REIT further has an investment-grade balance sheet, a diversified property portfolio, and covers its dividend payout with (adjusted) funds from operations. That said, though, the payout ratio has been rising in the last two years (implying a decreasing margin of dividend safety), and shares are probably fully valued at today’s price point. Though I own HCP (at a lower cost basis), the healthcare REIT is not a Buy right now.

Disclosure: I am/we are long HCP. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment