Note:

I have covered Globus Maritime (GLBS) previously, so investors should view this as an update to my earlier articles on the company.

Globus Maritime is a small drybulk shipping company, incorporated under the laws of the Marshall Islands and headquartered in Greece. The company’s fleet currently consists of five drybulk carriers, four Supramaxes, and one Panamax, all trading in the spot market. The average vessel age is 11.5 years.

Picture: Supramax drybulk carrier “Sky Globe” – Source: vesseltracker.com

The company is controlled by its founder and principal shareholder, Georgios Feidakis and lead by his son, Athanasios Feidakis who holds both the CEO and the CFO post.

Improved drybulk charter rates for the most part of 2018 have resulted in the company generating some cash flow from operations last year, but rates for many routes have collapsed over the past three months which makes the near-term outlook for the company more challenging.

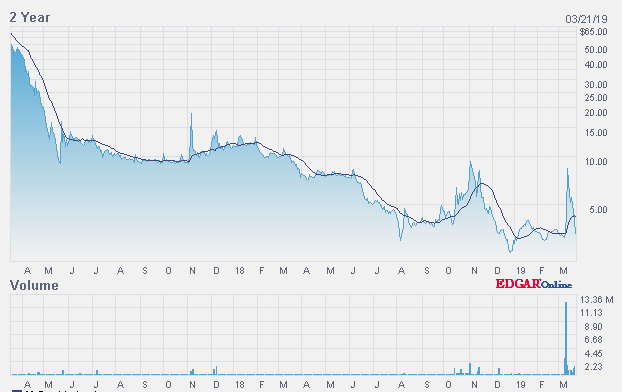

Two years ago, quite similar to shipping peers DryShips (NASDAQ:DRYS), Top Ships (NASDAQ:TOPS), and Performance Shipping (NASDAQ:DCIX), Globus Maritime utilized an infamous toxic financing transaction to recapitalize the company mostly at the expense of outside common shareholders.

While successful from a financial perspective, common shareholders have been paying the price, as very much evidenced by the two-year stock chart:

Source: Nasdaq.com

Looking at the company’s fundamentals, I estimate the value of the company’s fleet at approximately $60 million while total debt as of the end of 2018 was $37.9 million, leaving $22.1 million in net assets. Divided by the company’s outstanding share number of 3.2 million, net asset value per share calculates to roughly $6.90 per 12/31/2018 with the stock currently trading at an almost 50% discount.

On October 15, 2018, the company executed on a 1:10 reverse stock split which reduced the number of outstanding shares to 3.2 million and the free float to just 1.1 million thus making the stock an ideal target for momentum traders again.

As a result, the stock price has spiked several times since then as also evidenced by the six-month chart:

Source: Tradingview.com

As there has been no material company-related news, all of these moves were obviously induced by momentum traders with the latest hype just two weeks ago, causing the share price to explode by almost 100% in a single session on March 11.

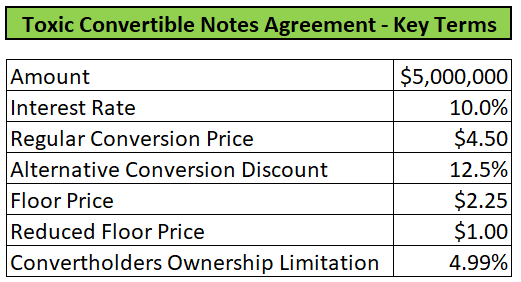

That said, the most recent spike came to an abrupt end after the company announced a $5 million toxic financing transaction on March 13 and the chairman subsequently disclosing the sale of almost 35% of his common shareholdings into the run.

The terms of the toxic financing agreement are pretty similar to many others already discussed by me in the past, incentivizing convertible noteholders to short the stock and subsequently covering their position through newly issued shares at a substantial discount to the average trading price over a certain measuring period:

Source: Company’s SEC-filings

Please note that discounted conversions will only be allowed if the stock trades below the regular conversion price of $4.50 after June 7, 2019. In addition, the company will be able to make interest payments in common stock.

In case of Globus Maritime, an assumed conversion of the notes at an average price of $2.50 would result in more than 60% dilution to current equity holders with the ultimate outcome potentially being much worse given the possibility to reduce the floor price down to $1.00 upon mutual agreement between company and noteholders.

Moreover, in November 2018, the company entered into a $15 million working capital facility with its controlling shareholder of which $2.2 million were drawn at the end of 2018. The company has the right to convert outstanding amounts and interest payments into common stock at any time at the higher of:

- A 20% discount to the value-weighted average trading price (“VWAP”) over a ten-day pricing period

- $2.80

Suffice to say, the conversion feature could result in even more substantial dilution to common shareholders.

In sum, business as usual at Globus Maritime with the company seemingly preparing for some tougher quarters with potentially negative cash flows ahead.

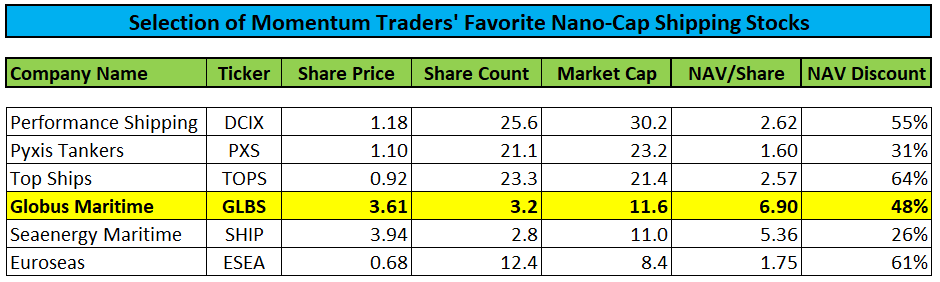

Looking at the company’s peer group of other Greek, mostly family-controlled, low-float, nano-cap shipping companies, the company is sitting right in the middle when considering the current discount to net asset value, but this metric will worsen upon conversion of the recently issued toxic notes and potentially outstanding amounts under the working capital facility going forward:

Source: Companies’ SEC filings, Author’s own work

Experienced traders and highly speculative investors should add all of the above-listed companies to their watch list as momentum traders tend to chase the entire group any time one of these stocks goes vertical on a major increase in trading volume.

Bottom Line:

Quite similar to recently discussed peer Seanergy Maritime (SHIP), Globus Maritime likely faces a couple of challenging quarters ahead due to very weak conditions in the dry bulk markets. That said, the company won’t face liquidity issues given the rather large $15 million working capital facility recently provided by its controlling shareholder. On the flip side, potential conversions of outstanding amounts and interest payments under the credit facility and the newly issued convertible note are very likely to result in renewed, substantial dilution to common shareholders.

Fundamental investors shouldn’t touch Globus Maritime or any other of the above-listed companies with a ten-foot pole, but momentum traders and speculative investors looking for a gamble from time to time should add the company and its peers to their watch list.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment