PUMP may not carry on its strong run in the short-term

ProPetro (PUMP) is a Texas-based oilfield services company which provides hydraulic fracturing and other related services. Its operations are primarily focused in the Permian Basin, but it also operates in some of the key unconventional resource basins in the U.S. I do not think PUMP’s stock price will continue to hold on to the gains over the past year and may weaken in the next couple of quarters. However, its long-term agreement with PXD and a much robust asset base will boost its top and bottom line in the medium-to-long term.

As hydraulic fracturing activity plateaus and completion activity recedes in the Permian, ProPetro took to cost reduction to improve margin. However, the lack of pressure pumping demand could affect its short-term prospects. Its ability to protect margin through cost reduction alone may not be sufficient to improve margin. PXD’s asset acquisition will place PUMP as one of the top pressure pumpers in the Permian Basin. Over the past year, PUMP has also added to its legacy pressure pumping as well as cementing and coiled tubing fleet. In the past year, ProPetro’s stock price has gone up by 17%, and significantly outperformed the VanEck Vectors Oil Services ETF (OIH) which declined by nearly 28% during this period.

Analyzing PUMP’s Q4 2018 drivers

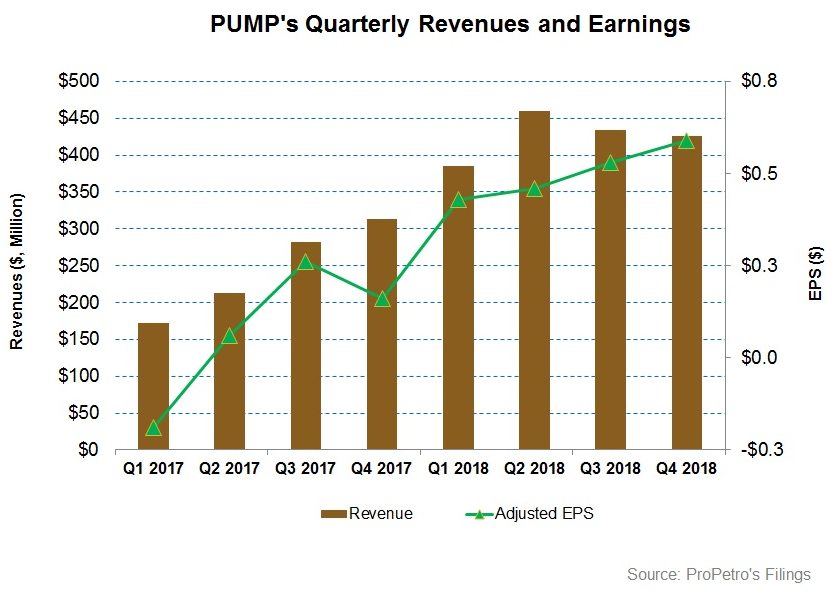

In Q4 2018, ProPetro’s top line declined marginally compared to Q3 2018, while its bottom line improved. On a year-over-year basis, its performance was even more impressive in Q4 2018. From Q3 to Q4, its revenues decreased by 2%, while from Q4 2017 to Q4 2018, the revenue growth was 36%. While lower pressure pumping demand during the winter season affected the Q4 revenues negatively compared to Q3, the year-over-year growth was primarily a function of a higher base following higher hydraulic fracturing activity. By the end of 2018, PUMP’s asset base increased significantly following the acquisition of Pioneer Natural Resources’ (PXD) pressure pumping assets which was completed on January 1. Read more on this in my previous article here. I will discuss more on this later.

From Q3 to Q4, PUMP’s adjusted earnings increased by 11% as its operating earnings improved. This is because its cost of services decreased steeply (6% down), driven by the use of cheaper regional sand volumes in Q4. The profitability growth from Q3 to Q4 was more of a cost-reduction function rather than the result of an efficiency gain. While an efficiency gain from zipper frac did increase, it was inherently a matter of higher state count. So, PUMP could not improve its pumping fleet efficiency during Q4.

Regarding this, PUMP’s management commented in the Q4 call,

I guess I would term our fourth quarter efficiencies as relatively flat relative to the third quarter in all of the metrics that we use to judge that, zipper frac percentage was very consistent at 83% to 84%. I will say that the stages — our total stages that we pumped in Q4 over Q3 was up about 4%, but we also added a fleet. So you have to take that into consideration. When you look at the actual stages pumped per fleet, we’re probably down about 1%, but there’s nothing strange about that considering the seasonality of the holidays. So in total, I guess, we considered efficiency to be relatively flat quarter-over-quarter, the enhancement to our profitability in Q4 over Q3 was primarily driven by our cost structure in a couple of line items, specifically sand and fuel, that is how we gained that additional profitability.

Analyzing PUMP’s FY2018 drivers

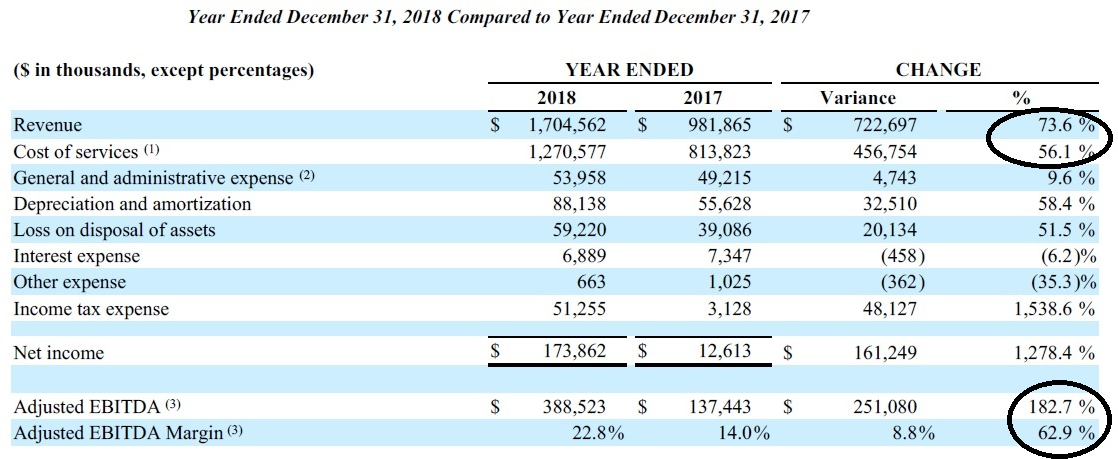

In FY2018, ProPetro’s revenue growth was remarkably higher than FY2017 (74% up) after its legacy business fleet capacity increased sharply. At the operating margin level also, PUMP’s performance improved. Its cost of services increased by 56%, which was considerably lower than the revenue growth. The pressure pumping cost of services decreased to 74.5% of its revenues in FY2018 from 83% a year ago, due primarily to operational efficiencies and PUMP’s cost control initiatives. During Q4, ~71% of the sand the company used was sourced locally as compared to 57% in Q3. As a result, the company’s EBITDA margin inflated by 8.8% during the year.

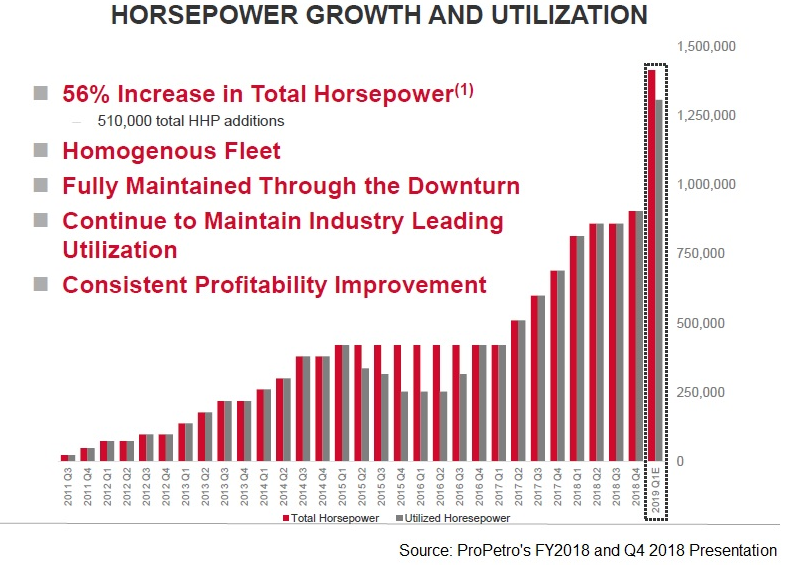

From FY2017 to FY2018, PUMP’s legacy pressure pumping fleet increased from 16 to 20, which resulted in a 31% horsepower capacity addition. In Q4, it added new build fleet dedicated for long-term use by a new customer. This took the company’s legacy pressure pumping capacity to 905,000 horsepower. PUMP also deployed two new-build cementing units in the past few months, which brought the cementing fleet count to 21.

As far as PUMP’s future plans go, it aims to add two new build cementing units. During 2018, it added a large diameter coiled tubing, which took the number of legacy coiled tubing units to four. According to PUMP’s management, it has drilled out plugs on two of the most extended laterals in the Permian. The laterals stretch beyond three miles in length and five miles in measured depth.

ProPetro’s asset acquisition deepens its Permian hold

Following PXD’s asset acquisition, ProPetro now has a 10-year strategic service agreement with Pioneer Natural Services. As a result of the deal, approximately 30% of PUMP’s total fleet will stay contracted to PXD. PXD has robust growth plans in the Permian. Currently, PXD is operating 22 rigs in the Spraberry/Wolfcamp field. It expects to place between 250 and 275 horizontal wells on production in 2018. Besides PXD, PUMP’s key customer base includes ExxonMobil (XOM), Diamondback Energy, Parsley Energy (PE), Concho Resources (CXO), among others.

PUMP will have 28 frac fleets with 1,415,000 HHP capacity, which would be an increase of 56% compared to its current base. On top of that, the new asset base includes 20 cementing units, six coiled-tubing units, and flowback operations. Not just an added figure, PUMP and PXD’s pressure pumping units have a homogeneous fleet. Because of lower costs, it can be relatively easily maintained during a downturn. Also, PUMP will have a strong utilization. With increased scale, the PUMP will likely generate greater purchasing power. The combined workforce is likely to share techniques and operations, improving service quality offerings. Also, the additional HHP can be utilized to limit maintenance capex.

PUMP’s management expects the deal to be accretive on a cash flow basis. This will flow from the higher exit revenue rate per fleet following the transaction. Also, EBITDA per fleet will increase from the current range of $14 – $16 to $16 – $18 by 2019.

Permian has been the leading driver and will continue to grow

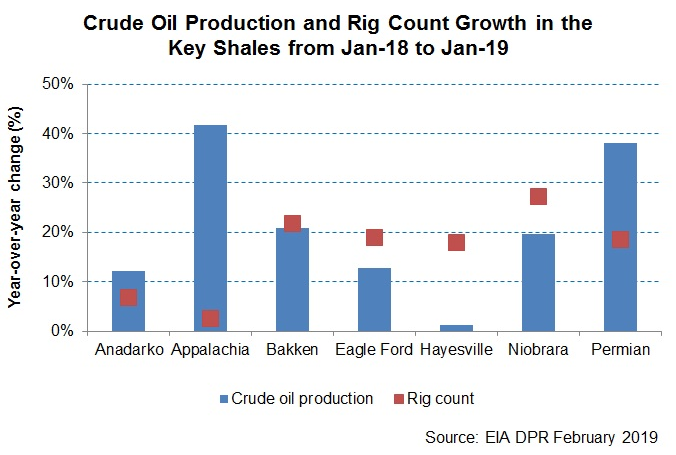

PUMP is a Texas-based oilfield services company. Its operations are primarily focused in the Permian Basin, but it also operates in some of the key unconventional resource basins in the U.S. Over the years, PUMP has built relationships with some of the most active and large E&P companies operating in this region. EIA’s data shows that the Permian Basin accounts for 48% of total crude oil production in the key unconventional shales identified by the EIA. The Permian crude oil production increased by 38% in the past year until January 2019. Rig count in this region, during the same period, increased by 19%. EIA’s estimates also show that Permian crude oil production is expected to grow by 2.3% by March compared to January.

PUMP’s debt level is manageable

In FY2018, PUMP generated $393 million in cash flow from operations (or CFO). On top of the 74% rise in revenues, PUMP’s remarkable improvement in CFO in FY2018 was aided by working capital improvement, primarily from lower accounts receivable. In FY2018, the company’s capex was $284 million.

PUMP’s total liquidity as of December 31, 2018, was $258 million, which included $125 million of borrowing capacity under the revolving credit facility. It has $70 million long-term debt which would be due for repayment in the next four to five years. With the available liquidity (cash balance and revolving credit facility), and at the current cash-flow-generation run rate plus no debt repayment obligations in near-term, PUMP’s balance sheet looks comfortably placed.

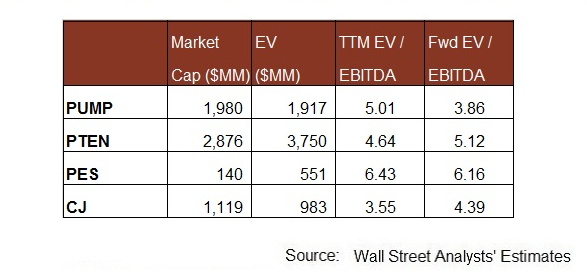

PUMP’s debt-to-equity ratio (0.18x) is lower than its peers’ average of 0.76x. Pioneer Energy Services (PES) has much higher leverage (2.6x). C&J Energy Services (CJ) had no debt.

What does PUMP’s relative valuation say?

PUMP is currently trading at an EV-to-adjusted EBITDA multiple of ~5x. Based on sell-side analysts’ estimates, as pulled from Thomson Reuters, PUMP’s forward EV/EBITDA multiple is lower, which implies higher EBITDA. PUMP is currently trading at a steep discount to its EV/EBITDA average of 52x, which was recorded from Q1 2017 through Q4 2018.

PUMP’s EBITDA is expected to improve more steeply than the rise in the peers’ average in the next four quarters, which typically reflects in higher current EV/EBITDA multiple compared to the peers. PUMP’s TTM EV/EBITDA multiple is only marginally higher than its peers’ (PTEN, PES, and CJ) average of 4.9x. So, PUMP can be considered relatively under-valued at this level.

Analysts’ rating on PUMP

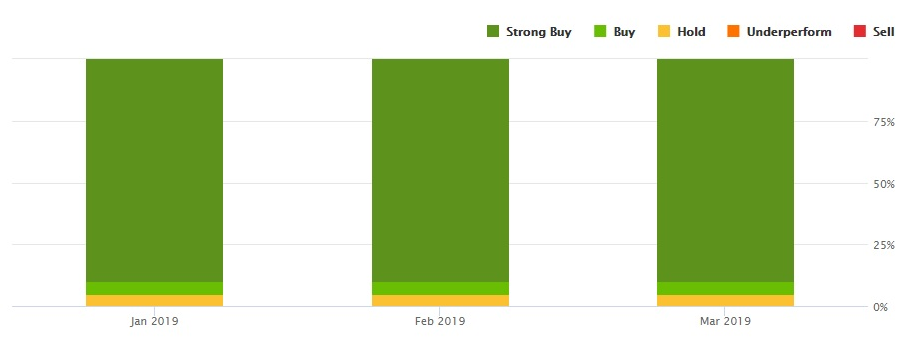

According to data provided by Seeking Alpha, nighteen sell-side analysts rated PUMP a “buy” in March (includes strong buys), while two of the sell-side analysts rated PUMP a “hold”. None of them rated it a “sell”. The analysts’ consensus target price for PUMP is $24.95, which at PUMP’s current price yields ~22% returns.

What’s the take on PUMP?

As hydraulic fracturing activity plateaus and completion activity recedes in the Permian, ProPetro took to cost reduction to improve margin. PXD’s asset acquisition will place PUMP as one of the top pressure pumpers in the Permian Basin. PUMP should benefit from a stable revenue base in the new venture following a ten-year agreement for 30% of the increased asset base. The transaction is expected to be revenue and EBITDA accretive.

Over the past year, PUMP has not only broadened its asset base through acquisition, but it has also added to its legacy pressure pumping as well as cementing and coiled tubing fleet. However, the lack of pressure pumping demand could affect its short-term prospects. Its ability to protect margin through cost reduction alone may not be sufficient to improve margin. PUMP has a strong balance sheet and its cash flows improved substantially in FY2018. I do not think PUMP’s stock price will continue to hold on to the gains over the past year and may weaken in the next couple of quarters. However, its long-term agreement with PXD and a much higher asset base will boost its top and bottom line in the medium-to-long term.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment