Hertz is in the middle of turnaround and based on what it’s been doing, I think it’s heading in the right direction with industry veteran Kathy Marinello at the helm. I believe it is a great buy at current price level of $17 based on the expectation that Hertz will likely earn at least $4/share by 2020. The reasons are: debt level is manageable, ridesharing driving car rentals out of business is not real, business environment is improving, all of its U.S. operating metrics are improving, and it’s near the end of its technology transformation.

First of all, Let’s address the main concern of Hertz’s investors, i.e. its high debt level. Looking closely, Hertz’s debt level is not as high as most would think. Most debt is vehicle related and used to purchase fleet, which is backed by the fleet itself, and has AAA credit ratings. Non-vehicle debt is $4.455 billion as of December 2018, of which, $700 million is due in 2020, $500 million due in 2021, and rest are due after. For a company with $434 million of adjusted EBITDA in 2018, it should be easy to refinance a $700 million bond in 2020. Additionally, Hertz has $1.1 billion of cash and $500 million of bank line. As a result, there is no default risk.

Secondly, there are lots of false assumptions around the impact of ridesharing on the rental business. Contrary to popular belief, ridesharing is not driving car rentals out of business as many have suggested. Ridesharing attracts one-way customers who would alternatively hire a taxi or use a mode of public transportation. They did affect a portion of the business, namely the short term corporate riders who needed one-way transportation from point A to point B, which originally weren’t supported by taxi due to area’s remoteness. This indeed had negative effects on the car rental business, but the impact is very small since most rentals are needed by longer days and more frequent travels between locations. Moreover, rental companies have also adapted to the ridesharing since its emergence, namely, partnering with Uber and Lyft by offer rental vehicles to ridesharing drivers at reduced rate, introducing on demand car rentals using apps, and also turning to other online platform such as Turo to address under-utilization.

Thirdly, the business environment is improving as the used car market gradually returns to normal, and in turn, has helped Hertz lowering its deprecation cost. Years of low interest environment resulted in a big increase in 0% interest leasing vehicles. When those vehicles came off lease, in turn, the used car market resulted in a big decrease in residual pricing. As interest rates climb, leasing market became normalized and in turn used car market is gradually returning to its normal state. The increase of used car prices is shown by the Manheim index. This in turn has provided tailwinds in the reduction of Hertz’s depreciation cost.

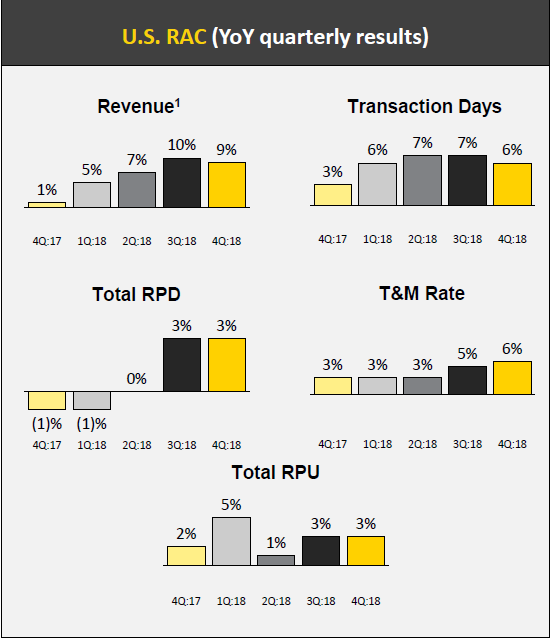

Moving onto Hertz’s operating metrics. All U.S. RAC (Rental of vehicles, as well as sales of value-added services) operating metrics ex-TNC (transportation network companies) are up: RPD (revenue per transaction days, which measures pricing), transaction days (measures volume), RPU (revenue per vehicle unit, which measures revenue productivity), T&M (time and mileages, which measures base rental fees), and vehicle utilization.

(Source: Hertz Q4 2018 Earnings Presentation)

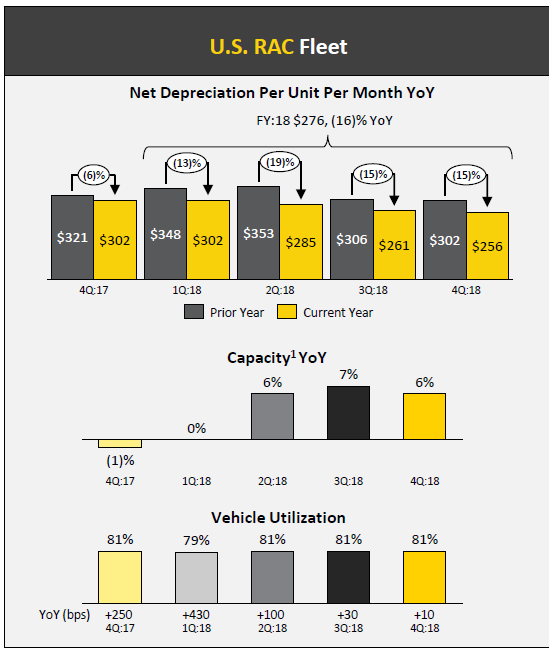

Deprecation/unit/month kept on going down year-over-year for last 5 quarters, driven not only by residual value market strength, but also diverse supply base, growth in TNC extending asset life, and sales through high-return channels.

(Source: Hertz Q4 2018 Earnings Presentation)

The fleet is still tight despite year-over-year capacity growth, since most of the growth came from TNC fleet. The increase in fleet is used to match TNC’s capacity to profitable demand, which is up 76% to 38,000 vehicles. Disciplined management in model year 2019 fleet is illustrated by lower year-over-year acquisition cost on like-for-like vehicles. Going into 2019, Hertz wants to sustain top line growth momentum through growth initiatives: right product, right place, right time, and right price, service excellence, and marketing. Despite having growth in RPD, Hertz’s pricing is still a lot lower than its competitors, especially when comparing at counter prices. Therefore, the top line growth strategy looks very achievable.

Finally, Hertz is about to finish its technology transformation in 2019. As a result that, the company has said that they expect a straight off the top $100 million reduction in operating cost on top of other synergy benefits. Also, as the bulk of turnaround spending is expected to end in 2019 resulting in lower investment cost ($98 million on technology transformation in 2018), which means, at the very least, Hertz is expected to have about $200 million of cost reduction in 2020. On top of that, Hertz should also expect to see stronger revenue productivity resulting from all the turnaround investments and initiatives since 2017. Putting everything together, if Hertz can generate modest growth by 2020, which looks very achievable based on what it’s been doing; the company will likely earn at least $4/share and probably more, translating into $60+/share and a 300%+ return in 2 years from the current share price of $17.

I have also listed 3 scenarios for 2019 to illustrate what I expect earnings could look like based on different top line growth outcomes. In a best case scenario, if Hertz can sustain top line growth near 8% for the first half of 2019 and 5% for the second half, I expect it to earn about $4/share for 2019.

| Forecast | 19 q1 | 19 q2 | 19 q3 | 19 q4 | 2019 |

| Revenue | 2228 | 2580 | 2940 | 2415 | 10163 |

| adj. eps | -0.63 | 1.2 | 2.25 | 1 | 3.82 |

If Hertz only sustains top line growth in the first half of year, and remain stagnant for the remainder of 2019, I expect it to earn about $2/share for 2019.

| Forecast | 19 q1 | 19 q2 | 18 q3 | 18 q4 | 2019 |

| Revenue | 2228 | 2580 | 2800 | 2300 | 9908 |

| adj. eps | -0.63 | 1.2 | 2.14 | -0.55 | 2.16 |

If the top line growth stays stagnant the entire 2019, Hertz should still make more money than 2018 just because of lower depreciation cost due to favorable used car market condition and better sales channel; as well as greater revenue productivity due to 2 years of turnaround initiatives.

In conclusion, I think Hertz is heading in the right direction and a great buy at $17 based on the expectation Hertz will likely earn at least $4/share by 2020. The reasons are: debt level is manageable, ridesharing driving car rentals out of business is not real, business environment is improving, all of its U.S. operating metrics are improving, and it’s near the end of its technology transformation. Additionally, as the above 3 scenarios indicate, it’s possible that Hertz will reach $4/share in 2019.

Disclosure: I am/we are long HTZ. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment