By Ansh Chaudhary

After the market experienced its worst-performing December since the Great Depression, the Dow Jones Industrial Average and the Nasdaq Composite Index have started this year with historic rallies.

According to CNBC, “This is the first time since 1964 that the Dow has rallied in each of the first nine weeks to kick off the year. The previous back-to-back week record was hit in 1964, when the Dow rose in all of the first 11 weeks through mid-March. Throughout those weeks, the Dow jumped 7 percent which was about half of its 14.6 gain for that year.”

Similarly, this is the first time the Nasdaq Composite Index has registered nine weeks in a row of positive performance at the start of a year. The Dow has rallied 11% and the Nasdaq Composite is up 9% thus far in 2019. The S&P 500 Index, another closely watched index, has rallied 18% since its Christmas Eve low.

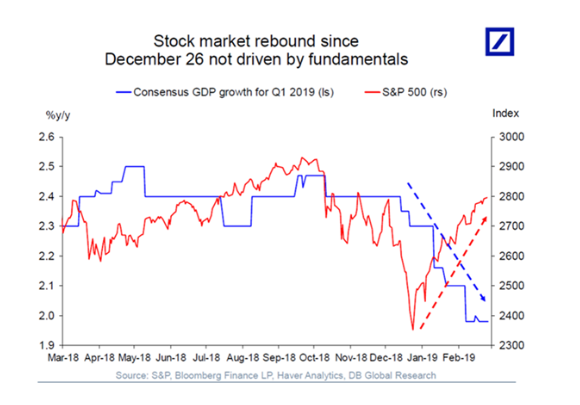

- Economists are concerned about this optimism in markets, however. While the S&P 500 makes a comeback, earnings growth forecasts for S&P 500 firms are turning negative. “Consensus first-quarter GDP growth has also been slashed to below 2 percent,” CNBC reports. The trend can be observed in the following chart. Some attribute the optimism to U.S-China trade talks and the Federal Reserve’s “patient” approach to tightening monetary supply. However, economic indicators show signs of weakness going forward.

Source: CNBC, Deutsche Bank

The National Association of Realtors released its pending home sales index on Wednesday, which showed an increase of 4.6% in January. Reuters interprets this as a loss of momentum in the housing market, considering existing home sales fell in January to their lowest level in over three years with only a modest increase in house prices.

The Commerce Department announced today that the goods trade deficit jumped 12.8% in December, to $79.5 billion. This arises from a 2.8% decline in exports and a 2.4% rise in imports in December, reports Reuters.

The central theme around everything playing a role in the markets right now is “patience.” Federal Reserve Chairman Jerome Powell appeared in front of the Senate on Wednesday for a second day of testimony on the U.S. economy and Fed policy. In Tuesday’s hearing, he described the U.S. economy as healthy and the outlook as good, but he also pointed to some headwinds. Trade uncertainty, global economic slowdown in Europe and China, and U.K’s Brexit have been sending conflicting signals for months. “We’re going to allow… the data to come in. I think we’re in a very good place to do that,” Mr. Powell said. It appears the Fed will be patient in implementing any policy moving forward.

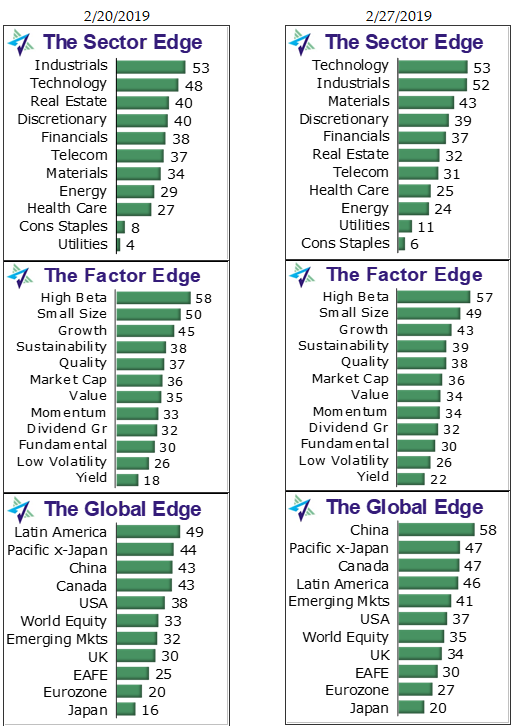

Sectors: The average momentum score for the Sector Benchmark ETFs decreased from 32.55 to 32.09. Eight of the 11 sectors saw a decrease in momentum score last week. Materials had the largest increase in momentum score, gaining 9 points. Materials jumped from seventh place to third, replacing Real Estate as one of the top three sectors. Consumer Staples and Utilities switched positions but remained at the bottom of the list.

Factors: Among the Factor Benchmark ETFs, the average factor score increased from 36.50 to 36.67. High Beta remained in the top spot despite losing 1 point. Small Size and Growth remained in the second and third spots. Low Volatility and Yield continued to lag.

Global: The average Global Benchmark ETF momentum score increased from 33.91 to 38.36 for the week. Momentum in the global sector increased in all regions except the USA and Latin America, which lost 1 and 3 points, respectively. China jumped from third to first with a 15-point increase in momentum score. The EAFE, eurozone, and Japan remained in the bottom three positions.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment