The latest Eurostat numbers on the European Union’s GDP are less than encouraging. Year-on-year growth in the EU 28 slowed to 1.4%. It was only 1.2% in the euro area, but robust growth within the non-Euro currency East European countries helped push up the EU average a few tenths of percentage points.

(Source: Eurostat)

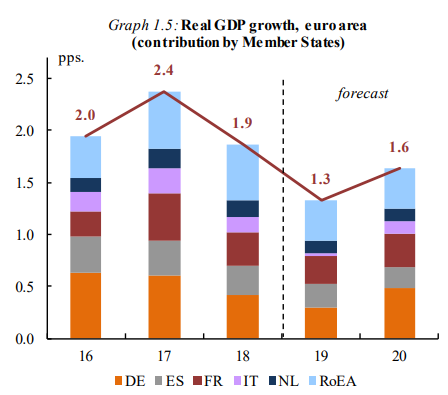

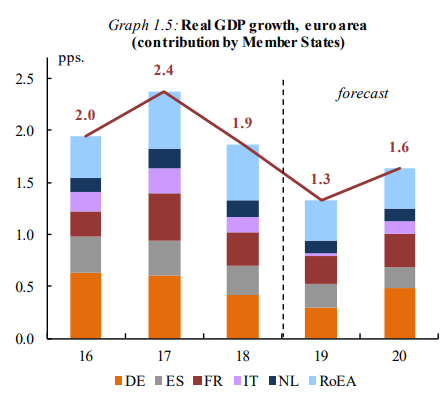

As we can see, this is now the slowest rate of growth within the EU since the second dip ended in 2013. Italy and Germany are countries of particular worry, because together they make up about 40% of the eurozone economy, and Germany’s economy shrank in the third quarter and stagnated in the fourth. Italy’s economy is officially in recession, with two consecutive quarters of decline. France’s economy is not doing much better, with only minimal growth of less than 1% compared with same quarter from last year. Things are already looking bleak going forward as well, with the EC now estimating EU growth for this year to be only about 1.3%, and even that is likely to be a missed forecast given all the potential downward trends.

(Source: EC)

Brexit set to happen as early as next month, if there is no extension

The Brexit saga is just about ready to hit the EU and the world now, with the clock ticking and only a month left and still no agreement in place on some sort of normalized relations between Britain and the EU. The extent of economic disruption that is likely to occur, regardless of whether there will be a deal in place or not, is not clear to anyone at this point. Needless to say, when the world’s fifth-largest economy decides to leave the world’s second-largest economic union, some major economic and global financial disruptions ought to be expected. While the significance of this event will be felt on a global scale, the EU will be at the epicenter – and as we can see, its economy is already looking rather flimsy going into what could become a major crisis.

It remains to be seen whether Britain will leave next month, or whether there will be some kicking of the can down the road, as has been recommended by some EU and British leaders. If it does happen next month, as is currently being planned, I do believe that regardless of whether or not there will be a deal in place, there will be economic disruption, which might just be enough to trigger secondary crises all over the EU.

Italy

About a year ago, France’s president Emmanuel Macron declared that Europe’s political divisions are akin to a civil war. Of course, since then he went on to call anti-establishment movements in the EU “leprosy” and a host of other unkind things. The liberal, pro-globalization forces which currently dominate the political landscape in Europe repeatedly lashed out at countries where conservative political factions asserted themselves, especially in Eastern Europe. They launched infringement proceedings against Hungary and Poland, threatening to take away their voting rights in the EU. But then, an anti-establishment coalition won the last Italian elections, and I do believe the EU establishment will lash out at them as well, which could become very dangerous. France and Italy are already lashing out at each other at a bilateral level, as they are now on opposite sides of the ideological divide.

In the case of Italy, the anti-establishment government took over a country which has been struggling economically for the past decade, and arguably ever since the introduction of the euro in 1999. It currently has the EU’s second-largest debt/GDP ratio after Greece. Because of that, the EU insists that it should stick with austerity, keeping deficits below 1% – far below the 3% threshold, which is when excessive deficit procedures are ordinarily launched. The EU seems to have very little appetite for compromise in the case of Italy, offering limited leeway in allowing it to run a higher deficit in order to restart the engines of the country’s economy. There is a compromise in place, but for far less leeway than the country was hoping for.

The fact that Italy just entered an official recession and the EU is unwilling to budge on deficits could, in my view, trigger a serious economic crisis, with Italy facing the twin constraints of deficit limits as well as the inability to engage in monetary policies, which would ordinarily involve currency devaluation, due to the monetary union. Such a crisis could, in turn, cause a Greek-style financial crisis. It is true that the ECB is now more prepared to intervene in such circumstances than it was back in 2010 when the Greek debt crisis started. At the same time, there are plenty of factors which could impede the ECB from intervening; for instance, a drop in the value of the euro beyond what might be seen as desirable, or perhaps a rise in inflation. There is also only so much that monetary policy can do.

My personal worry is that within the context of what does now seem like a widespread ideological civil war, EU leadership as well as the leadership of several states within the EU might see this as an opportunity to punish a country where the anti-establishment political forces won the national elections. The idea is to discredit the current government and turn the Italian electorate against them. The hope is that the electorate in other countries will be persuaded to refrain from the anti-system vote as well, by reinforcing the perception that such a vote will only lead to disaster. The danger is that such a strategy can easily backfire in countless ways. One of the ways that it can backfire is obviously the fact that it could unleash an uncontrollable, EU-wide economic crisis, leading to even more popular dissatisfaction.

Eastern members, which currently contribute a great deal to overall EU growth rates and momentum, are set to face sabotage

At the moment, the Eastern members of the EU are by far the strongest performers in terms of economic growth. On average, they have been growing at about twice the rate of the EU average since 2013. These countries make up about 10% of the EU economy collectively, while making up about 20% of its population.

The overall impact on the average rate of EU growth is not overly significant, but the region does affect the EU in some other ways. Roughly 75-80% of the region’s trade is happening with the rest of the EU, and the overall volume of trade that Western EU does with Eastern members surpasses the volume of trade that is done with the EU’s number one partner, the US. In 2018, the region imported over 550 billion euros’ worth of goods from rest of EU, while the US imported 406 billion euros’ worth, according to Eurostat. In other words, the economic growth in countries like Germany depends to a great extent on the level of demand growth for goods and services in the Eastern part of the EU. If this region were to see a significant slowdown in economic activity, it would have a major adverse effect on the entire EU. There are a number of EU initiatives which could endanger growth in the region, thus potentially stalling out the EU’s only economic bright spot at the moment.

Global economic turbulence could not have come at a worse time for the EU

For a few decades now, the European continent has been by far the worst performer in terms of economic growth as well as a number of other metrics. This year things are already looking bleak, with economic growth slowing, while tensions ranging from Brexit to North-South or East-West as well as within nations are paralyzing the decision making process, just as solutions are needed with more and more urgency. Even when decisions are made, they are increasingly the wrong ones, causing more economic and social damage rather than providing solutions. Just as the EU is seemingly engaged in a process of self-destruction, the global trade and overall economic situation is worsening.

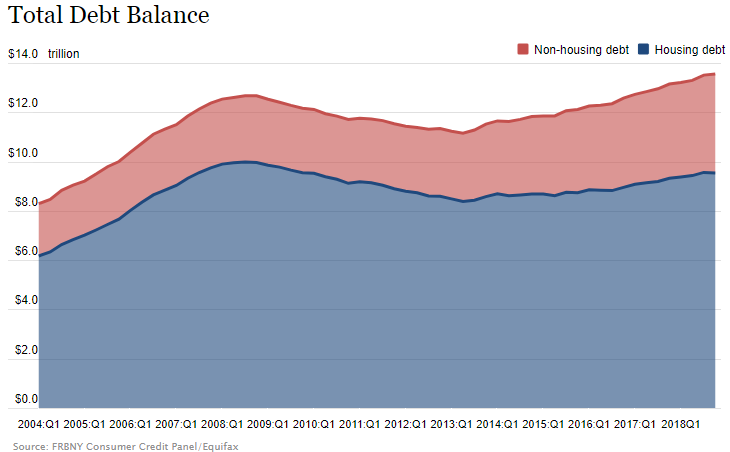

The IMF lowered its economic growth forecast by .2% in its latest assessment of the world, in large part because of trade issues but also because of EU economic troubles. I personally don’t believe it will be the last downgrade, with the EU in turmoil, the world’s two largest economies locked in a continued trade standoff, as well as the US economy slowing after the initial boosting effect of the tax cuts. Ultimately, the fact that the current recovery has gone on for so long now is also a negative, for the simple fact that more and more consumers have been satisfying their needs, while taking on more debt.

(Source: Federal Reserve Bank of New York)

At some point, which I believe is coming soon, consumer demand will stagnate as we become more mindful of the accumulation in debt. In the fourth quarter of 2018, credit card debt increased by $28 billion. That is an average increase of $233 per household in only three months. If we think of it as an extra interest burden, given the almost 17% average interest rate that credit cards carry, it means that on average every household now owes an extra $40/year in interest. We should keep in mind that car loans, student loans as well as other burdens are also on the rise, which will at some point trigger a consumer spending slowdown.

A slowdown in global growth was already evident last year. The fact that the EU economy is almost screeching to a halt, while others are just slowing, is indicative of the fact that it is the weakest major economy. It serves as both an early warning for the rest of the world, as well as being a source of vulnerability for the global economy. At this point, the EC is still forecasting average EU growth of 1.3% for the year. If that level drops below 1% – which I think there is a very good chance that it will, especially given the lack of will to make good decisions at the EU level – it will be the first sign of the start of a global economic slowdown, perhaps not this year but definitely going into the next.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment