The iShares 7-10 Year Treasury Bond ETF (IEF) is up 4.84% since November 2018, though it has mostly been moving sideways since the start of the year. The most predominant drivers of treasuries include actions from the Federal Reserve, and the economic outlook, both of which are currently supportive for medium-term treasuries, and the IEF ETF.

Source: Yahoo Finance

Prospectus Review:

The IEF ETF tracks the ICE U.S. Treasury 7-10 Year Bond Index as its underlying benchmark. The fund’s management uses a “representative sampling” strategy, whereby they do not invest in all 7-10yr Treasuries, but invest in a sample of securities that they believe are representative of the performance and investment profile (e.g. average duration) of the underlying benchmark. This is a fund that uses an “indexing” strategy, and hence it is not actively managed, allowing for most cost-efficiency.

The fund has a weighted average maturity of 8.34 years, and an effective duration of 7.45 years.

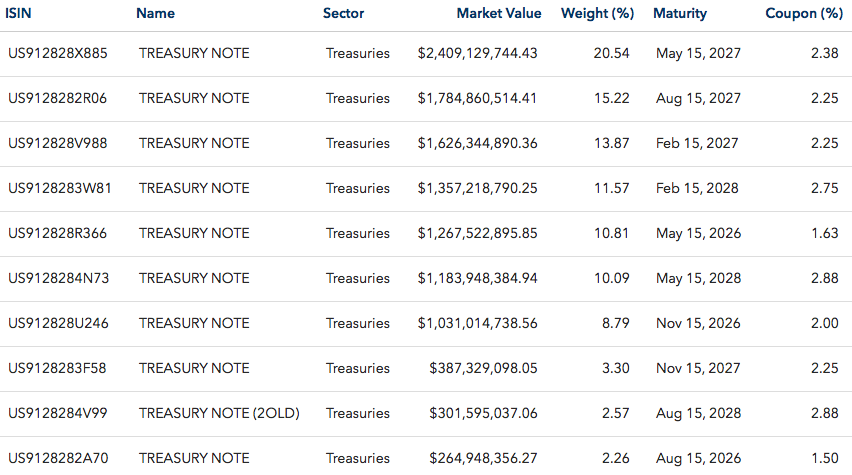

The top 10 holdings of the fund include:

Risk note from prospectus:

There is no guarantee that the Fund’s investment results will have a high degree of correlation to those of the Underlying Index or that the Fund will achieve its investment objective. Market disruptions and regulatory restrictions could have an adverse effect on the Fund’s ability to adjust its exposure to the required levels in order to track the underlying Index.

Moreover, out of all the ETF’s that offer exposure to this section of the Treasury yield curve, this ETF has the highest Assets Under Management (AUM), currently standing at around $11.73 billion, according to data from ETFdb.com. I consider AUM as a good indicator for how successful the fund has been in implementing its strategy to deliver on its objectives for investors. The higher its AUM, the more investors have allocated their capital towards the fund due to effective management. Moreover, it also has one of the highest average daily trading volumes, currently at 5.43 million. Hence this means that the ETF has a relatively healthy level of liquidity. This is a good indicator for how easily investors can buy and sell shares in the ETF. Therefore, the higher the trading volume, the lower the liquidity risks.

Fed could stop balance sheet unwinding sooner

On Jan. 30, 2019, Fed chairman Jerome Powell eased investors’ concerns over the pace of the Fed balance sheet unwinding. The Fed’s current strategy of allowing $50 billion worth of fixed-income securities (including mortgage-backed securities and treasuries), is curbing the level of excess reserves held by depositary institutions, and consequently pushing the fed funds rate closer to the top end of the range set by the Fed.

Powell acknowledged the usefulness for depositary institutions to hold excess reserves in order to meet regulatory liquidity requirements. As a result, he stated that the Fed would end the balance sheet unwinding sooner to ensure there are “ample reserves” for the nation’s banks.

Given that the average maturity of the Fed’s bond portfolio is currently around 8 years. Therefore, if the Fed ends its balance sheet unwinding sooner, it will benefit this mid-section of the yield curve the most, and consequently the IEF ETF (which holds exposure to 7-10 years treasuries only). If the Fed stops allowing these bonds to “roll off”, then it would inhibit the supply of treasuries in financial markets from growing further, and thereby provide support to treasury prices.

Dovish Powell not improving economic outlook

Other than willing to end the balance sheet unwinding sooner, Powell also expressed dovishness through putting rate hikes “on hold” at present, amid growing economic “cross-currents”, which are undermining the economic outlook. Hence, the Fed is avoiding inducing a recession by continuing to tighten monetary policy conditions amid a slowing economy.

Nevertheless, his accommodative guidance has had little impact on easing market participants’ concerns of a potential recession on the horizon. CME Groups’ FedWatch tool is still reflecting a 12.5% chance of a rate cut in December 2019, and a 21.7% chance in January 2020 (at time of writing). This exhibits how fears of a recession on the horizon have not completely vanished following Powell’s dovish guidance. Moreover, the probabilities of rate hikes this year for other Fed meetings, have been declining, while chances of rate cuts have been increasing (though only modestly).

Therefore, given that worries of a recession are still present, and expectations of future interest rate levels continue to slide, yields on medium to long-term treasuries are likely to continue falling, which will allow the inversely correlated treasury bond prices to move higher. Therefore, the IEF ETF could benefit from rising concerns of more economic pain ahead.

Strategy

With the Fed willing to end balance sheet unwinding sooner, the mid-section of the yield curve will witness an easing of ‘supply’ pressure from the Fed, which will support medium-term treasury prices, and consequently, the IEF ETF. Additionally, fears of a recession ahead are still present, even amid a dovish Fed. This is suppressing medium-term yields, and thereby allowing treasury prices to move higher. Hence, these two factors provide compelling reasons to buy into the IEF ETF. While certain positive economic data releases induce yields to move higher (and bond prices lower), I believe the predominant trend for the economy is ‘weakening’. Therefore, I believe any such dips in the 7-10yr treasury bonds and IEF ETF are buying opportunities.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in IEF over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment