Note: Granite Oil Corporation (OTCQX:GXOCF) trades OTC in the US and under the ticker GXO on the TSX. There is significantly higher liquidity on TSX.

Granite Oil Corporation would rather forget about 2018. The company that tried to be investor-friendly by returning cash in the form of dividends found itself at the end of a horrible pricing for its heavy oil. The stock price collapsed, and the negative cash flow caused it to suspend its dividend, and the resulting collapse has left the company trading at a fraction of where it was 7 months back.

Data by YCharts

As investors know well, selling begets more selling, and year end time is notorious for this. This collapse, while justified by changes in fundamentals, is now stuck in the past. The market is failing to appreciate just how much the fundamentals have changed in the past 60 days. We look at what the change has been and why the stock represents a very huge torque on oil prices.

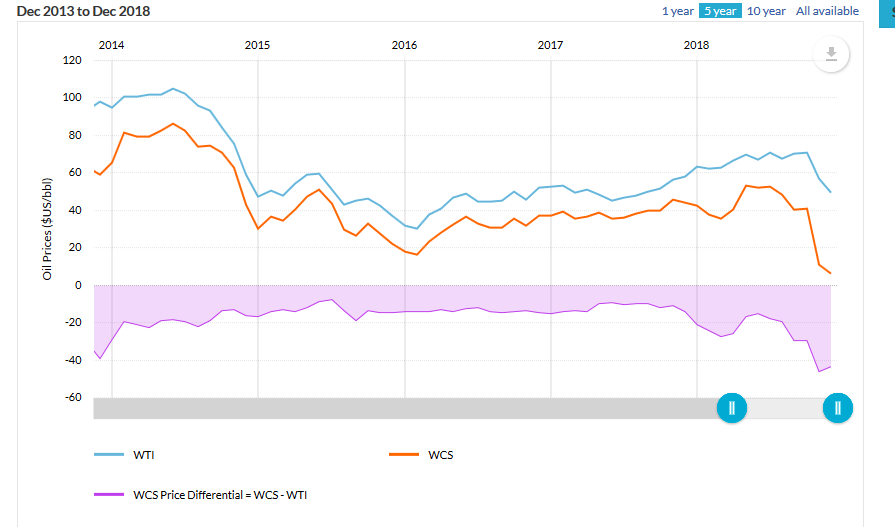

Heavy oil differential blowout

At the heart of the matter was Canadian oil production exceeding pipeline takeaway capacity. The actual amounts of excess were not large, and we estimate that it was less than 5% of total supply. But everything is priced at the margin, and the excess created a local glut pushing down heavy oil prices. Canadian heavy oil differentials, which had been trending higher all year, widened at a crazy pace, and at one point, Western Canadian Select (WCS) was being given away at a US$40 discount to West Texas Intermediate (“WTI”).

Source: Economic Dashboard Alberta

Granite was not only facing a blowup of epic proportions on its heavy oil. It was also facing the ultimate nightmare wherein it had used WTI prices to “hedge” its exposure. This was the worst of both worlds as Granite lost money on its hedges as WTI prices went up and at the same time it lost money on every barrel of crude oil it produced as differentials went up. The company suspended its dividend and even issued equity at rock bottom prices as its very viability was at stake if Q4-2018 conditions persisted.

What changed

The Alberta Government which had been watching this drama unfold from the sidelines felt it had enough of pipeline issues creating a royalty nightmare for it. The integrated companies like Suncor (SU) and Imperial Oil (IMO) were having a feast as they were paying royalties off the low benchmarked WCS price while making money by selling end products at all-time high crack spreads. Rachel Notley, the premier, tried to get oil companies to reach a consensus but failed to get SU and IMO onboard. That is when she exercised Alberta’s right to restrict production via the Alberta Energy Regulator (“AER”). A little known fact here is that pretty much every company that drills for oil in Alberta essentially gives Alberta through AER, unlimited power to restrict their production. Notley would have preferred a voluntary curtailment but knew that would take too long to have an impact. The key issue was the first mover disadvantage, wherein the company cutting first would suffer without any benefit from the cut itself. Also, she felt that there was some serious gaming of the situation by the majors and she needed to put an end to it. The production cut was thus enforced, and the differentials reacted at a torrid pace.

Source: Trading View

The heavy oil barrels are now trading at one of the best prices of the last decade in relation to WTI.

What this means for Granite

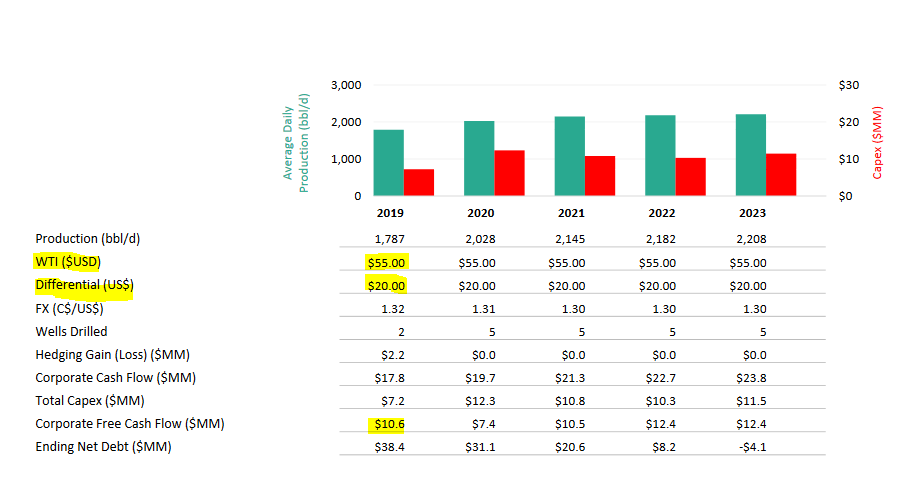

Granite released their outlook for the next five years based on what they felt were reasonable assumptions.

Source: Granite Oil Presentation

At $55 USD WTI oil and a $20 USD differential, Granite produces $10.6 million CAD of free cash flow. That should itself be worth noting with the company’s market cap of under $25 million CAD.

Data by YCharts

Data by YCharts

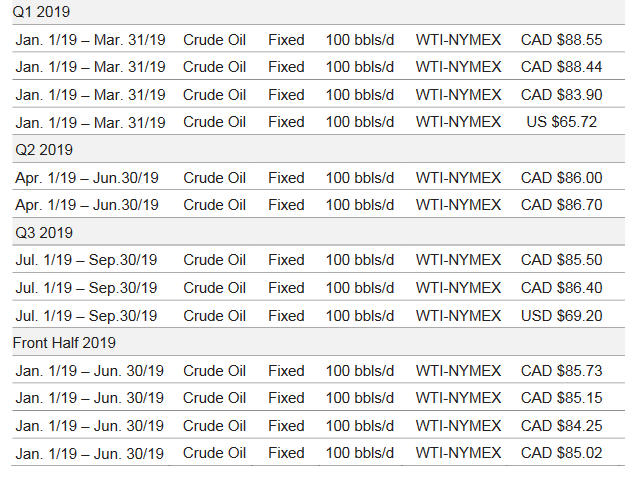

But it does get better. The differentials have now collapsed into the sub $10 zone. Granite has also hedged WTI for 2019 at much higher prices (see chart below), and hence at $55 USD WTI, it will have hedging gains. Excluding hedging gains, Granite is forecasting $15.6 million CAD of corporate cash flow. That is on production of 1,787 barrels per day or 652,255 barrels total. Essentially, the cash flow netback is $23.91 CAD per barrel. A $10 USD differential collapse, which would be about $13 CAD, would add about $10.4 CAD per barrel to cash flow after additional royalties. Granite pays about 18-20% in royalties. The calculations are quite complex, but within this range, the impact is relatively at the same level. To be conservative, we have used the 20% number. At the current level of differentials, we project corporate cash flow prior to hedging gains jumps to $22.77 million CAD ($15.6M+($10.4 X 652,255)). The hedging gain remains identical as it is benchmarked on WTI and not WCS.

Source: Granite Oil Corp Q3-2018 Financials

So, alongside hedges, at $55 USD WTI, Granite should rake in $25 million CAD in cash flow, slightly exceeding its market cap. This should also allow it to reduce its ending 2019 debt to close to $31.5 million CAD. The same numbers give Granite an ending EV to free cash flow of 3.1X (3.4X if you exclude hedging gains).

Why bad differentials are a thing of the past

Rachel Notley is extremely determined to make sure Alberta gets its fair share of royalties and that the heavy oil should not be given away. Her prime political opponent was actually in favor of mandating an even larger production cut, (400,0000 vs. the actual 325,000 enforced), so the risk from the upcoming election is minimal. The excess inventories in Alberta are being rapidly cleared from the rampup of crude by rail and production cuts. Additionally, Enbridge’s (ENB) line 3 expansion will have a pre-fill season from mid-June, wherein the new capacity is filled end to end. This alongside the decline of heavy oil from Venezuelan sanctions means that heavy oil is going from excess to relative scarcity very quickly. Most importantly, as a company producing under 10,000 barrels/day, Granite is exempt from the production cut mandate. The fundamental forces are well aligned for Granite to deleverage in 2019, and the market should give it a better multiple.

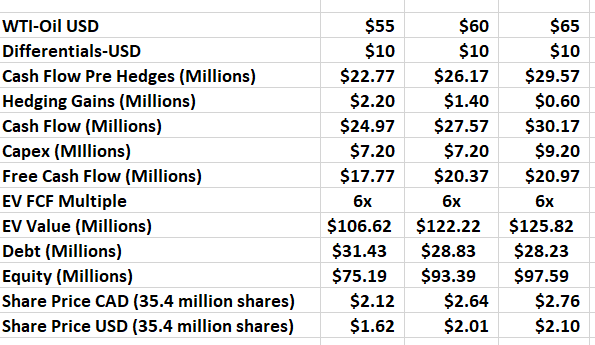

How high can this go

Our longer term case assumes at least $60 USD WTI alongside a $10 USD WCS differential. Further upside in oil prices will not produce much boost to free cash flow as Granite will use excess cash flow to boost production. A 6X EV to free cash flow multiple, which would also be conservative, would translate into a stock price of almost 300% higher.

Source: Author’s calculations, Debt numbers obtained by taking corporate ending projected debt of $38.4 M and reducing that by additional projected FCF ($38.40 + 10.80 – $17.77) at $55 and so on.

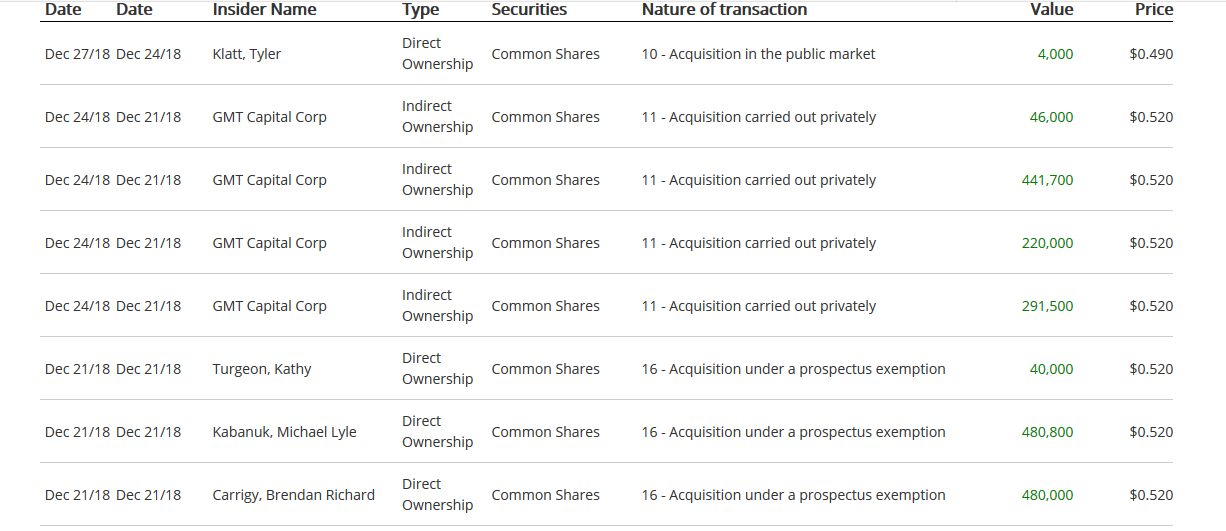

Insiders own 24% of the diluted float and have interests definitely aligned.

Source: Granite Oil Presentation

Further, they have been adding here aggressively.

Source: Canadian Insider

This represents one of the most compelling opportunities where just a matter of time will allow the company stock to move significantly higher. The key risk would be a complete collapse in oil prices as even with narrow differentials, this would hurt the company. We see low risk of that as we believe shale requires a minimum of $60 USD WTI to add necessary production to keep supply in balance for 2019. However, should global supply-demand remain balanced (no substantial inventory drawdowns) at even $45 USD WTI, for 9 months, we would abandon our bullish bias. The sheer asymmetry is pretty phenomenal as even at $45 USD WTI and $10 USD differentials, Granite produces slightly more free cash flow than at $55 USD WTI and $20 USD differentials. The reason is that the $10 drop in WTI is offset partially by more hedging gains, whereas the $10 better differentials flow straight to the bottom line. Hence a worst-case scenario to us is what Granite is already projecting for 2019, a $10.6 million corporate free cash flow. If the worst case is realized, at current price, Granite will still be trading at 6X EV to free cash flow. While the stock could go a bit lower, we feel it is discounting a rather catastrophic scenario.

Disclosure: I am/we are long GXOCF, ENB. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment