Introduction

Part of being an investor is to locate opportunities for above-average growth. Since timing and beating the market is practically impossible, these opportunities are rare and usually very risky. In 2008, during the financial crisis, American banks suffered from deteriorating fundamentals, lack of liquidity, and plunging share prices. Citigroup (C) suffered from being too leveraged and lacking the necessary amount of liquidity, and for several reasons, the stock price was depressed.

The bank had to deal with bad debt, massive share dilution in order to achieve funding, and billions of dollars in fines by the regulators. Since then, the stock managed to offer tremendous growth. The company has ample liquidity, debt levels are reasonable, and with litigation mostly behind it, Citigroup offers EPS growth and returns billions of dollars to its shareholders.

This is hindsight, obviously, but I try to learn from this situation. I try to look for corporations, especially banks, that are in a similar situation. This is, of course, not part of my traditional dividend growth portfolio. This is the part of my portfolio where I look for small opportunities to achieve some additional alpha. Finding a company now in a similar situation to Citigroup may offer additional returns.

Banco Santander (SAN), for example, is another example for a European bank in distress. I analyzed it in 2018 and found it to be a risky addition to dividend growth portfolios. This time, I am going to analyze Barclays (BCS), one of the largest banks in the United Kingdom. I will look at the fundamentals and the valuation. In addition, I will look at the Brexit situation and try to understand how it deals with its debt, liquidity, and stress tests.

Barclays operates as a bank holding company that engages in the business of providing retail banking, credit cards, corporate and investment banking and wealth management services. The company operates through two divisions: Barclays UK and Barclays International. Barclays was founded on July 20, 1896, and is headquartered in London, the United Kingdom

(Source: Wikipedia.org)

Fundamentals

The company suffers from declining sales as the banking giant is lowering its leverage and focusing on its core business. The company is less focused on increasing sales and more focused on increasing earnings and profitability. Therefore, they become a leaner bank and offer more conservative services. In the long run, the company will have to increase sales, but focusing on liquidity and profitability makes sense since the bank still struggles to achieve decent returns.

Data by YCharts

Data by YCharts

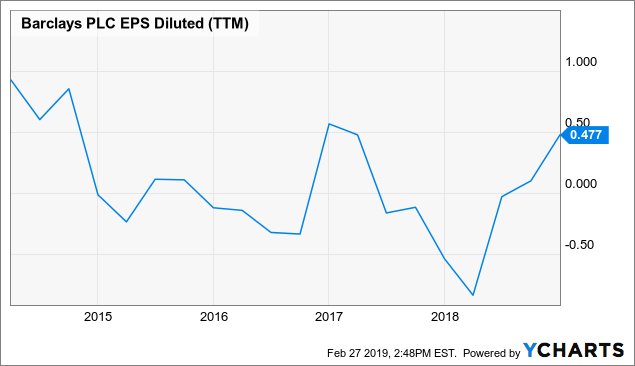

While revenues were flat in 2018, profits soared by 20%. The EPS was erratic in the past several years, but in 2018, it managed to show healthy growth despite the uncertainties in the UK regarding the Brexit. The return on equity has improved, and this includes the impairment of 150 million GBP due to the Brexit-related uncertainty. It seems like Barclays found its balance with stable liquidity and higher return on equity with EPS growing by 35% and forecasted to grow in 2019 as well.

Data by YCharts

Data by YCharts

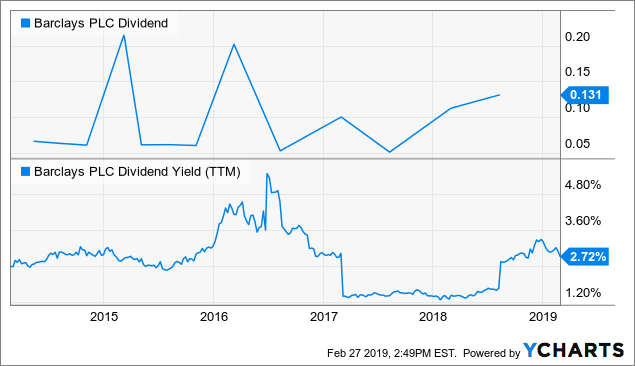

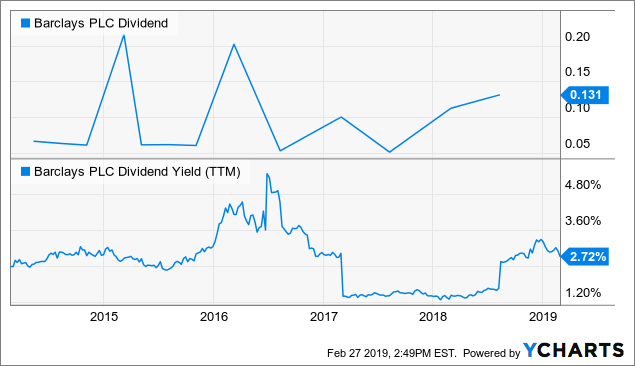

The dividend was frozen in the past two years but was raised significantly lately. The latest payment was 2.5 pence per share (in the UK), and it was more than double the dividend payment a year earlier. In April 2019, investors will receive 4 pence per share, an amount that hasn’t been seen since the financial crisis in 2008. With EPS exceeding 21 pence per share, and the dividend instated at 6.5 pence, the dividend is safe and represents a meaningful increase.

Data by YCharts

Data by YCharts

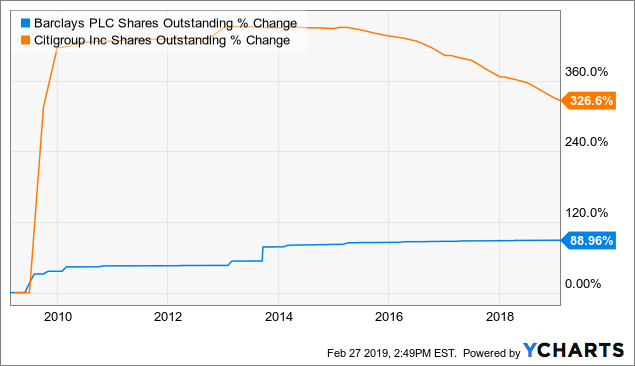

The company, like Citigroup, has issued billions of shares to achieve liquidity. While Citigroup started to buy back its shares in order to lower the share count and support EPS, Barclays is not there yet. However, the company issues less shares to fund its operation, and the management announced that, with enough liquidity, it will start buying back its shares soon. The combination of a progressive dividend and share buybacks may be very attractive in the medium and long term.

Data by YCharts

Data by YCharts

Valuation

The forward P/E ratio is at its lowest point in the past three years. Investors are still skeptic regarding the ability of Barclays to heal and keep growing its earning. The macro environment with Brexit coming at the end of next month also pressures the valuation. In my opinion, the current valuation offers a decent margin of safety. The valuation implies that the stock is risky, but rewards don’t come without risk.

Data by YCharts

Data by YCharts

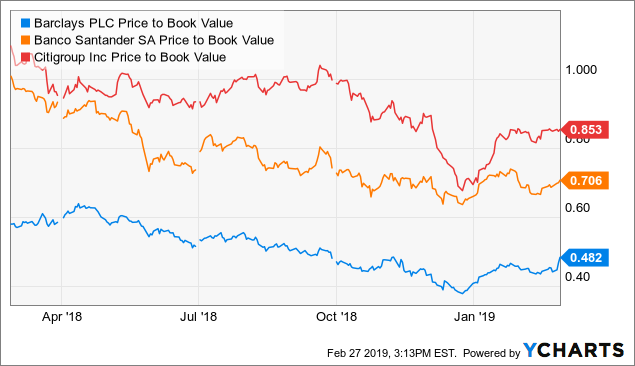

My favorite metric when I look at the valuation of banks is price to book value. I added for comparison the P/B ratio of Citigroup and Santander. I believe that the current valuation Barclays represents a very pessimistic view of the British economy. I believe that it should trade at a similar valuation as Santander. Santander has some weaknesses just like Barclays, and Barclays has exposure to more stable markets.

Data by YCharts

Data by YCharts

Barclays showed poor fundamentals over the past decade. However, it seems like the management finally managed to stop the bleeding. Liquidity has stabled and is more than enough. The earnings are growing quickly, and with them, the dividend payment. In addition, the company is looking for buybacks in the near future. This entire package comes with a very low valuation. The question is whether such a low valuation is still justified. Personally, I believe that it does offer some margin of safety.

Brexit

Brexit is a main threat for Barclays. The uncertainty regarding the UK leaving the EU makes investors less interested in stocks that may be affected. However, it is important to note that companies, Barclays included, have prepared for the Brexit. It was even noted by the credit rating agencies that the impact on Barclays in the worst-case scenario will be small.

Prime minister May is now considering delaying the Brexit, while the labor, the opposition party, is in favor of a new referendum. It means that both parties are uncertain whether the whole Brexit process is a good idea. For banks like Barclays, no Brexit is the best option, but the thing it needs the most for short-term gains is higher certainty. As we get closer to Brexit day, the level of uncertainty will decrease.

The Brexit poses a risk on British stocks, but it should be taken in the right proportions. We all remember how stocks plunged the day after the referendum and how they have recovered since. Long-term investors can take advantage of the uncertain times ahead. The risk is here and shouldn’t be ignored, yet it should be analyzed and understood in order to be able to asses it.

Leverage

The company still relies on high level of debt in order to finance its operation. The debt to equity and debt to capital level are still very high compared to healthier banks. However, the company is working on lowering the leverage and improving its funding sources. In their latest annual report, the company emphasized the need to diversify the funding of the operation focusing on deposits.

We can see the improvement in the liquidity and leverage in the British stress tests. The company now is very stable, and according to the Bank of England:

“The 2018 Stress Tests shows the UK banking system is resilient to deep simultaneous recessions in the UK and global economies”.

Together with the Brexit impairment, I believe that Barclays has what it needs to survive the hardships ahead.

The company also maintains CET1 ratio of 13.2%, which is higher than Barclays’s target of 13% and higher than the regulatory demands by the Bank of England, which stands at 11.7%. It means that the company maintains a liquidity level which is even higher than the regulatory demands. The company has sufficient capital to return to its shareholders and unlock more value.

In its latest presentation, the management stated that it is ready to reinstate a progressive dividend policy and start buying back shares. This, in my opinion, is one of the best signs of the health of a corporation. The management believes that the leverage is manageable, and there is enough capital to reward shareholders while improving the business, as in 2018, the company invested heavily in it.

Conclusions

In many ways, Barclays resembles Citigroup several years ago. The share dilution, the high leverage, the value destruction, and the uncertainty regarding its future. Since Citigroup was in this position, it has grown significantly, and it shows healthy growth on a yearly basis. Barclays has just raised its dividends and implied that buybacks will return soon. It may imply that just like the case of Citigroup, the worst is behind it.

However, investors should know how risky investing in Barclays is. In the past, there were several moments when investors believed that the worst is over, only to find out that there are still hardships ahead. Therefore, the valuation is so depressed. I believe that the current valuation is depressed enough to suit the risks and offer an interesting risk reward ratio.

The best way to invest in this kind of securities is to allocate a very small percentage of the portfolio to them. There are several European banks that are in a similar position to Barclays. Santander is one of them, and several Swiss banks resemble this situation as well. Making a basket of several European banks from several major European countries can offer a significant return potential with limited risks.

Disclosure: I am/we are long C. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment