Next week, there were going to be a lot of eyes on Canadian cannabis firm Tilray (TLRY). While the pot stock has been one of the most fascinating names to watch since going public last July, it was about to hit a major point in its history. Fortunately for investors, a major risk that was about to hit has been removed in the short term.

On January 15th, Tilray’s lockup expiration hits. For those that are unfamiliar with the stock, there were 16,666,667 shares of Class 1 stock outstanding as of the latest 10-Q filing, along with 76,498,178 shares of Class 2. It is the Class 2 shares that trade on the NASDAQ. Privateer Holdings owns all of that Class 1 stock, which contains 10 votes per share, along with 58,333,333 Class 2 shares with one vote each, giving it substantial control over the company.

Back in July 2018, the company went public, selling 10.35 million shares at a price of 17.00 per share. Until we hit the date next week, those were basically the only shares that could be freely traded, with the rest “locked up”. Investors have known this for months, and this is normal for any IPO to have a number of shares not able to be sold for a given period (in this case 6 months) after going public.

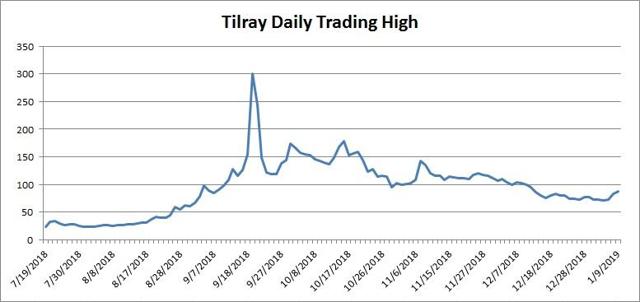

What this means is that Privateer Holdings, along with any other insiders, can now sell those shares freely in the market, which could send the float substantially higher from its roughly 10 million figure currently. Tilray has done extremely well since its IPO thanks to investors flooding into cannabis names, although it is well off its ridiculous high point. The following chart shows the daily trading chart to show the rally and collapse. I used the daily high instead of closing price, because the September 19th close of $214.06 doesn’t show the entire story since the name peaked at $300 that day.

(Source: Yahoo! Finance – last data point on chart is January 10th)

The good news for investors is that Privateer Holdings issued a statement on Friday morning detailing its current plan for its share stake. The firm will not sell any shares in Tilray during the first half of 2019, and the quote below details how things will happen moving forward:

“When we decide to distribute shares, we will do so in an orderly and deliberate manner to maximize tax-efficiency considerations for Privateer investors, while also taking into consideration potential impacts on Tilray’s public float. And we will do it in a way that reflects our long-term confidence in Tilray’s business model and management team.”

The company did take the opportunity when shares rallied, selling convertible notes back in October. The money raised will help with the company’s growth over the next couple of years, which is projected to be astronomical. While the street is looking for about $40 million in revenues to be reported when the 2018 final numbers are in, this year is expected to see the top line soar to more than $134 million. I will also be watching to see how the company does with its margins and operating expenses, because right now the losses and cash burn are terrible. That is to be somewhat expected, however, during this stage of growth, but you’d like to see some improvement over time.

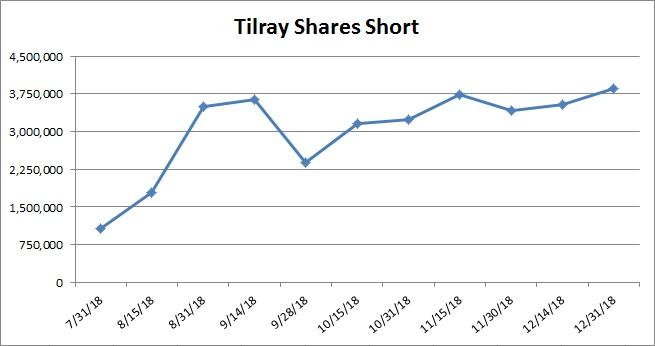

One interesting item to note is that Tilray has had a very high percentage of its float shorted since it started spiking after the IPO. With such a low float, the price to borrow recently soared to 900%, making it very expensive to be on the short side of the trade. As you can see in the chart below, short interest just reported showed a new high hit at the end of 2018, as we approached the lockup expiration. Once the float starts to rise, more shares could be available to be shorted.

(Source: NASDAQ Tilray short interest page)

(Source: NASDAQ Tilray short interest page)

Just a few days before the lockup expiration was due to hit for Tilray, Privateer Holdings announced it would not sell any shares during the first half of 2019. This has Tilray shares soaring in the pre-market on Friday, although they are still well off their all-time high. This news removes a major risk for the short term, basically kicking the can down the road for six months, and investors can now look forward to seeing how the company’s results are progressing. The company still has work to do, especially when it trades for a massive 66 times this year’s expected revenues.

Author’s additional disclosure: Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment