With one product candidate at Phase 3 of development and three product candidates at Phase 2 of development, Stealth BioTherapeutics (MITO) seems very tempting. Having said that, the financial risk is quite elevated. Stealth BioTherapeutics has a large amount of liabilities, which could represent an issue in the future. If the company needs to sell further equity in the future, the stock dilution could make the stock fall. Finally, the company was incorporated in Cayman, where shareholders are not as protected as in the United States. Many things need to change on this name in order to become a low-risk opportunity. Conservative investors and non-institutional investors should avoid this stock.

Source: Prospectus

Source: Prospectus

Business Candidates And Milestones

Founded in 2006 and based in Cayman, Stealth BioTherapeutics is a clinical-stage biotechnology company developing new therapies for the diseases involving mitochondrial dysfunction.

Source: Company’s Website

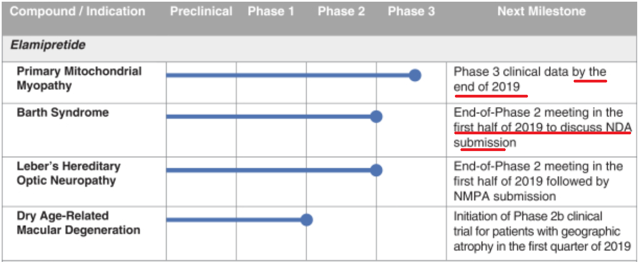

Among the different rare genetic diseases associated with this condition, the company’s lead product candidate, elamipretide, is intended to treat primary mitochondrial myopathy, Barth and Leber’s hereditary optic neuropathy. In addition, the company is also researching treatments for Dry-Age Related Macular Degeneration and Neurodegeneration.

Investors will appreciate that the company’s pipeline shows one candidate at Phase 3 of development and three product candidates at Phase 2 or close to finish Phase 2 of development. With this in mind, shareholders will not have to wait a long time to know whether the products can be commercialised or not.

In addition, in 2019, Stealth BioTherapeutics is expected to release a large amount of results. If the data released is beneficial, the stock price should increase. The image below provides further details on this matter:

Source: Prospectus

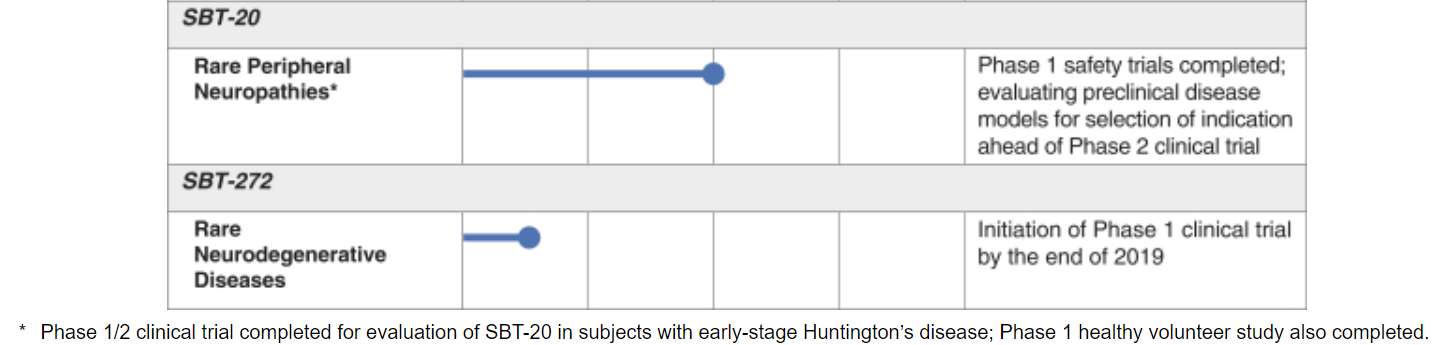

The company has two more product candidates at Phase 1 of development and one candidate at preclinical development. While investors should carefully study the product candidate elamipretide, candidates SBT-20 and SBT-272 are beneficial. If results of elamipretide are not beneficial, shareholders know that the company has other programs that could be approved by the FDA. The image below provides further details on this matter:

Source: Prospectus

Elamipretide To Treat Primary Mitochondrial Myopathy

After the IPO, the company expects to have money to finance the completion of the Phase 3 clinical trial intended to treat primary mitochondrial myopathy. The trial is being conducted in North America and Europe, and data will be released by the end of 2019. With this in mind, assessing this condition and the clinical data obtained so far seems the most relevant on this name.

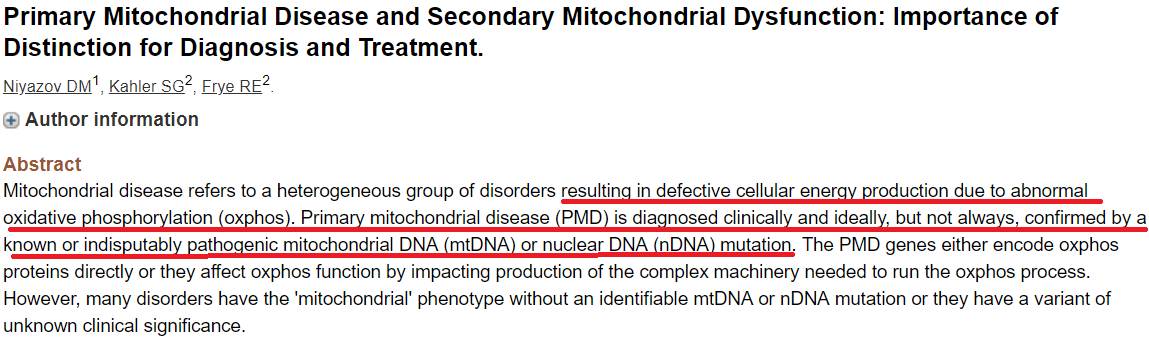

Primary mitochondrial myopathy is characterized by debilitating skeletal muscle weakness, exercise intolerance, and fatigue. The lines below provide further details on this matter:

Source: NCBI

The market opportunity is not that large. The company estimated that approximately 40,000 individuals in the United States are suffering from mitochondrial myopathy. The market for mitochondrial myopathy is expected to be worth $33.6 million by the end of 2020 and should grow at a CAGR of approximately 9.82% from 2017 to 2020.

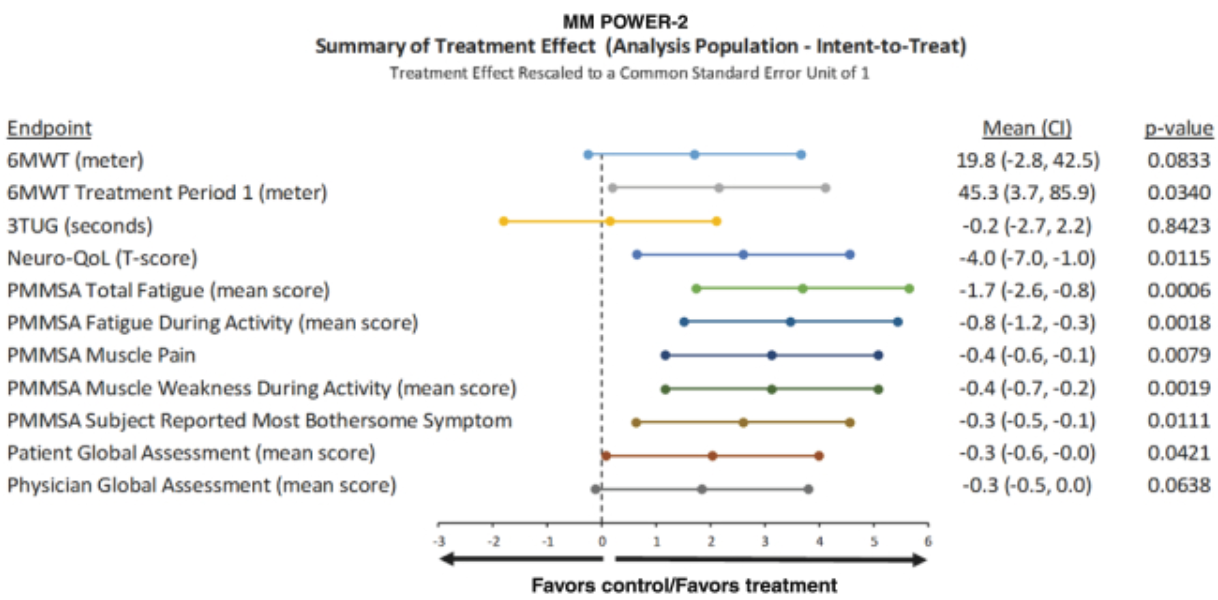

The company has registered over 400 subjects with signs and symptoms of primary mitochondrial myopathy in a multi-national pre-trial registry. As of September 30, 2018, 86 subjects with primary mitochondrial myopathy have been treated. As shown in the image below, the results have been very beneficial:

Source: Prospectus

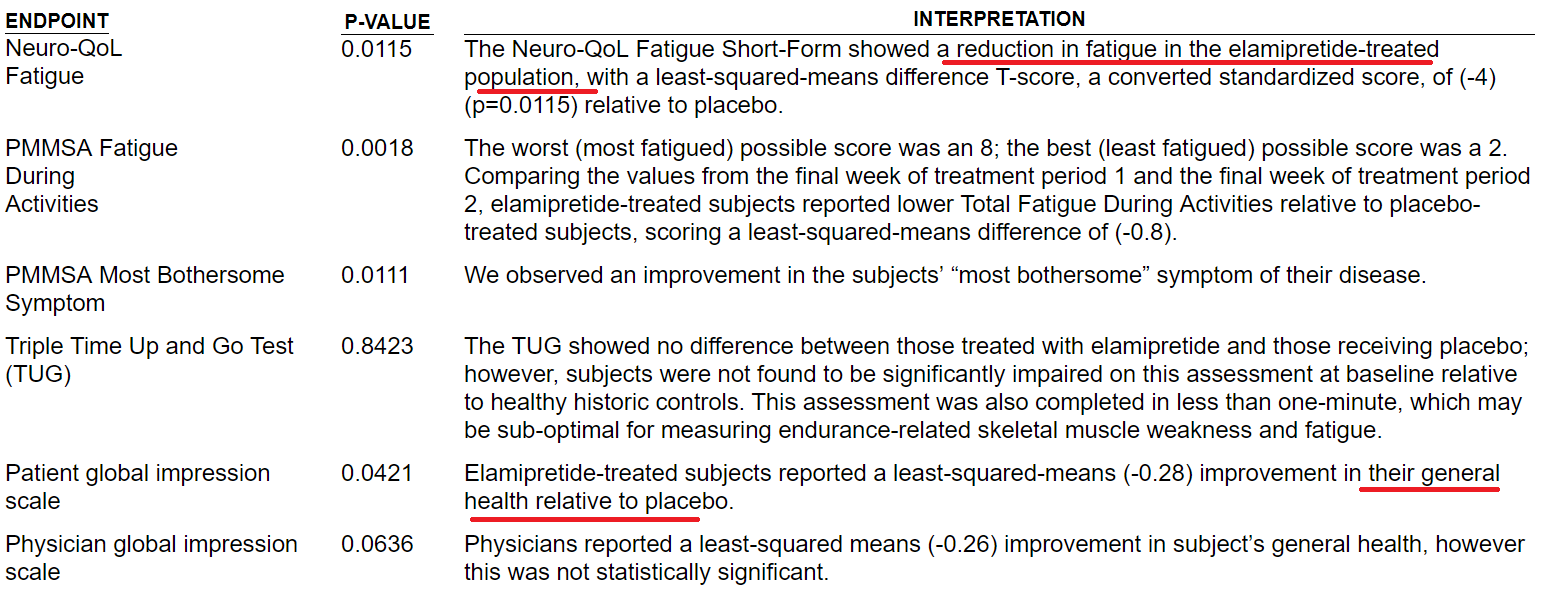

Certain interpretations offered by Stealth BioTherapeutics in the prospectus are given below. The most relevant conclusions were that the treatment helped reduce fatigue with a p-value of 0.0115 and improved the general health of patients with a p-value of 0.0421. The table below provides further details on this matter:

Source: Prospectus

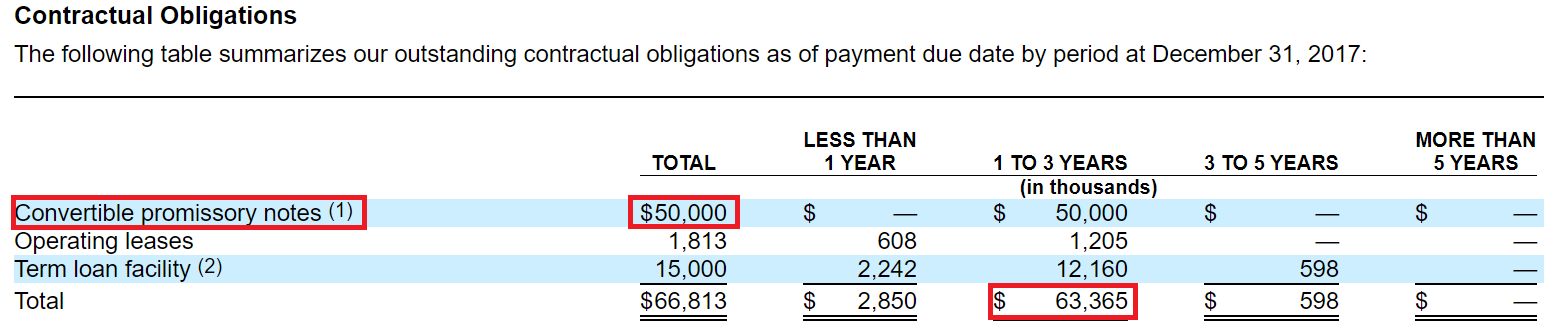

Balance Sheet

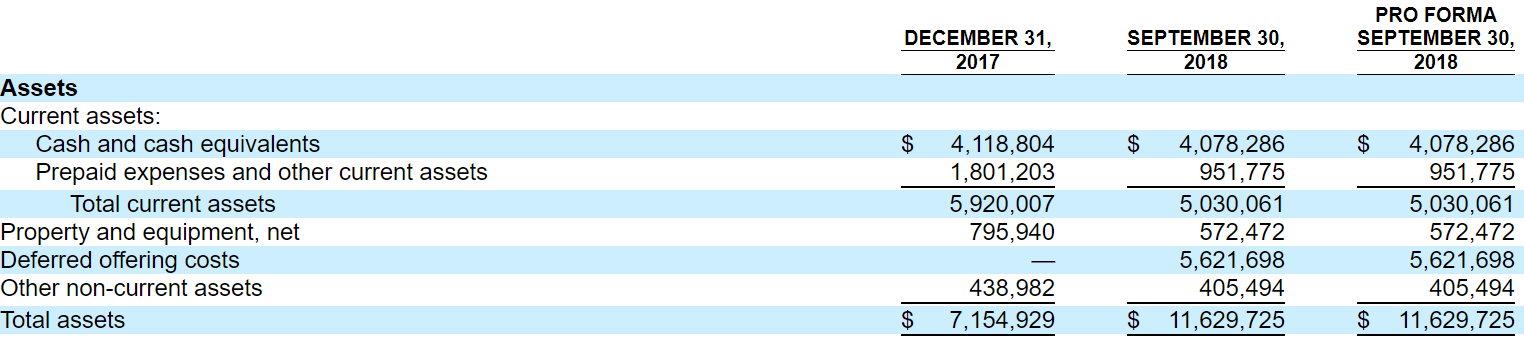

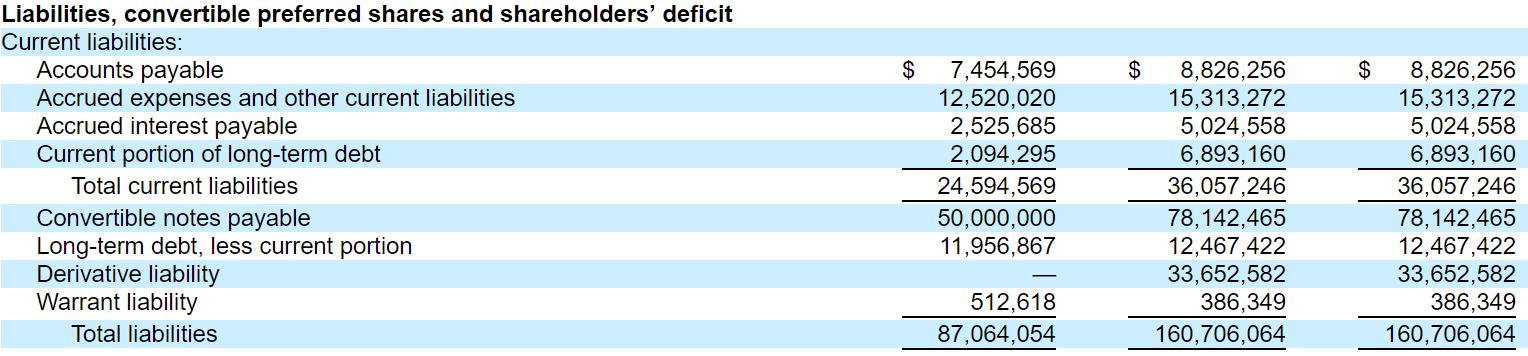

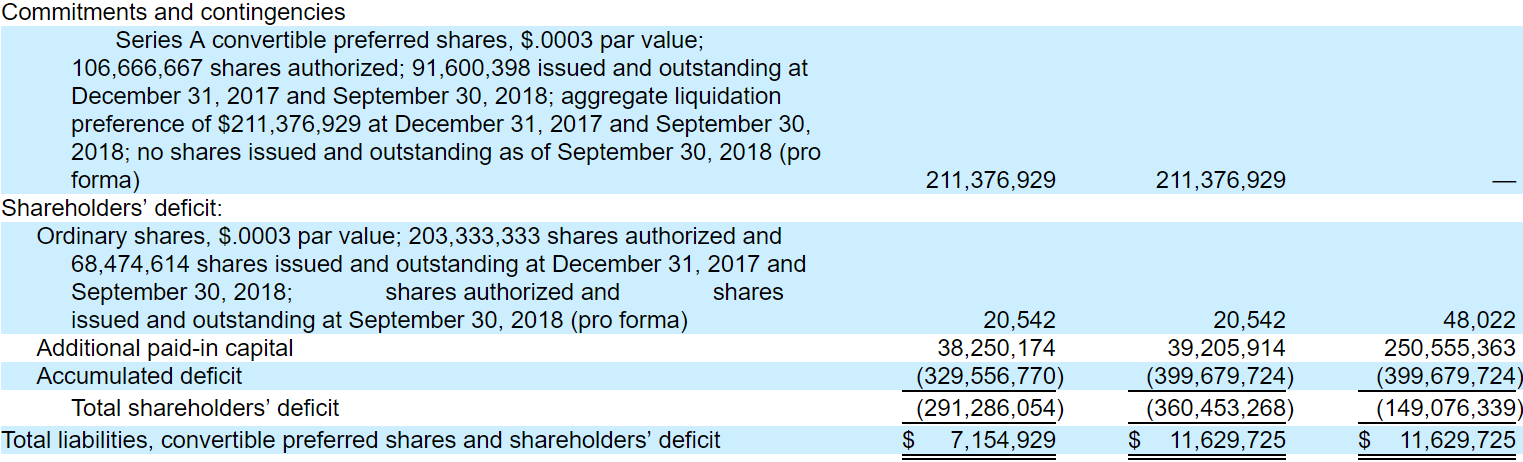

With an asset/liability ratio below one, certain investors may not appreciate the company’s financial situation. As of September 30, 2018, Stealth BioTherapeutics reported $4 million in cash, total assets of $11.6 million, and total liabilities of $160 million. The most worrying are the amount of long-term debt, equal to $12.4 million, its derivative liabilities, and warrants liabilities. Before the IPO goes live, the company does not seem to have enough liquidity to pay its debt. The image below provides further details on this matter:

Source: Prospectus

Source: Prospectus

While the company may not have to pay a lot of money in 2019, it should pay a total of $63.3 million in one to three years. Stealth BioTherapeutics does not say that it will use the money from the IPO to pay the debt. It may look for other financing sources. Investors should be very careful as further sale of equity could lead to stock dilution and share price depreciation. The image below provides further details on this matter:

Source: Prospectus

Having said that, after the IPO, it will be beneficial that the company is expected to convert its convertible preferred shares into common stock. Shareholders will not need to worry about the potential stock dilution from these convertible securities. Note that all outstanding Series A convertible preferred shares will be converted into approximately 91.600 million ordinary shares. The image below provides further details on this matter:

Source: Prospectus

Income Statement

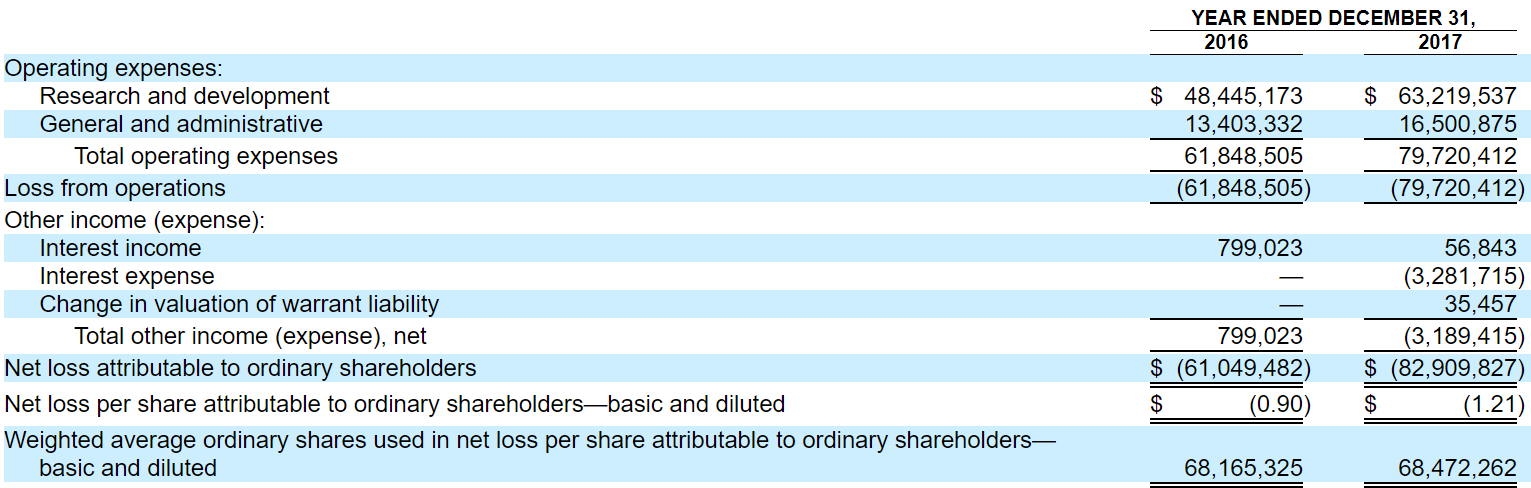

The income statement is another worrying feature. In 2017 and 2016, the company reported $61 million and $82 million, respectively, and in the nine months ended September 30, 2018, the total loss reported was equal to $70 million. With total assets of only $11.6 million, the company does not seem to have liquidity to finance further research. Additionally, if the company raises $86.250 million in the IPO, Stealth BioTherapeutics should not be able to finance its operations for more than two years. The image below provides further details on this matter:

Source: Prospectus

Use Of Proceeds

It is very beneficial that the company does not intend to use the proceeds to pay debt or acquire shares from existing shareholders. Stealth BioTherapeutics will use the money to finance the development of its lead product candidate, the preclinical development of SBT-272 among other general corporate business purposes. The image below provides further details on this matter:

Source: Prospectus

With that said, the lines below are very relevant for investors. Keep in mind that the company expects to be able to complete a Phase 3 clinical trial for elamipretide for primary mitochondrial myopathy. Further cash will be needed to complete other clinical programs:

We anticipate that, assuming our current operating plan, the net proceeds from this offering, together with our existing cash and cash equivalents, will only be sufficient to allow us to complete a Phase 3 clinical trial for elamipretide for primary mitochondrial myopathy, to initiate but not complete our planned Phase 2b clinical trial for the treatment of dry AMD, and to conduct a Phase 1 trial of SBT-272.” Source: Prospectus

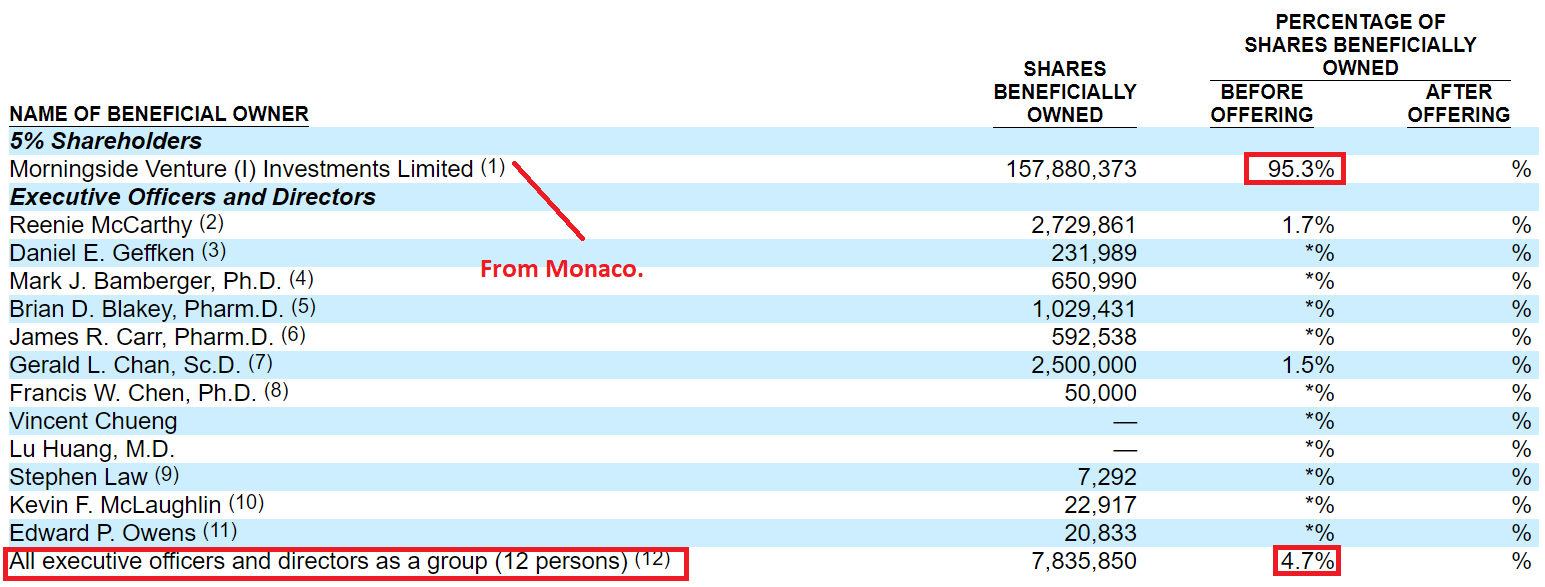

Shareholders

The assessment of shareholders shows that Stealth BioTherapeutics has not been able to sell shares to many venture capital firms. It is not ideal. There is only one fund incorporated in Monaco owning 95.3% of Stealth BioTherapeutics. The image below provides further details on this matter:

Source: Prospectus

Shareholder Rights In Cayman

The company was incorporated in Cayman, where the securities laws are not as developed as in the United States. As a result, shareholders will have difficulties in protecting their interests. It may be difficult for shareholders to take action against the management or the Board of Directors. The lines below provide further details on this matter:

Source: Prospectus

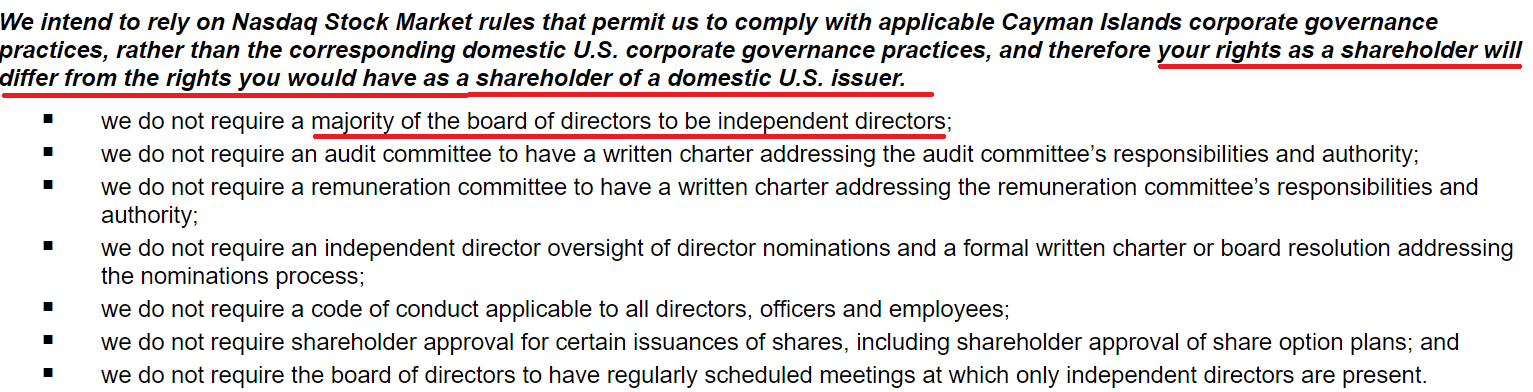

That’s not all. The company does not seem to have intention to form an independent Board of Directors. This is very worrying. Keep in mind that the directors could take decisions to benefit the largest shareholder, which could damage the interest of minority shareholders. The lines below provide further details on this matter:

Source: Prospectus

Conclusion

With very beneficial results from clinical trials, the most worrying is the company’s financial stability. Stealth BioTherapeutics has a massive amount of liabilities and less amount of cash. In addition, the company will only be able to complete the primary mitochondrial myopathy program. Further financing will be needed to finish the other programs. If the company sells additional equity, the stock dilution could make the share price fall. Finally, it is not convenient that Stealth BioTherapeutics was incorporated in Cayman. In this jurisdiction, shareholders are not as protected as in the United States.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment