Investment Thesis

Canadian Western Bank (OTCPK:CBWBF) [TSX:CWB] delivered a good fiscal 2018. However, its top and bottom line growth rates are expected to moderate in 2019 due to a weak economic outlook in Alberta, slow real estate activities in Ontario and British Columbia, and flat net interest margin outlook. The company’s share price is significantly undervalued. However, given the bank’s much higher exposure to Western Canada, we think conservative investors with a long-term horizon should choose other alternatives.

Source: YCharts

Q4 2018 Highlights

Canadian Western Bank delivered a solid Q4 2018 with revenue growth of 7% year over year driven by 11% growth in its net interest income. Its fiscal 2018 total revenue increased to C$803 million (for growth of 11%). Its adjusted cash EPS also increased to C$0.78 per share in Q4 2018 (an increase of 5% year over year). In fiscal 2018, the bank delivered adjusted cash EPS of C$3.01 (or growth rates of 14%).

Reasons why we think investors should wait on the sidelines

Despite strong growth in 2018, we believe Canadian Western Bank’s 2019 growth may moderate in 2019 for the following reasons:

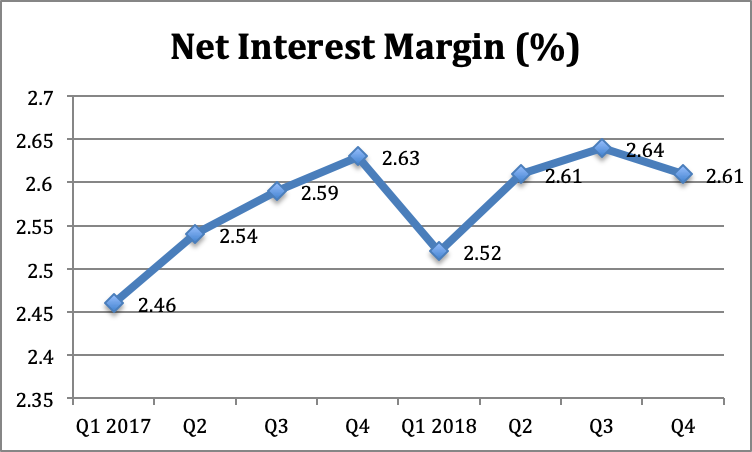

Net interest margin expected to remain flat

Since mid-2017, the Bank of Canada has raised its overnight interest rate 5 times. This has helped Canadian Western Bank to increase its net interest margin from 2.46% in Q1 2017 to the high of 2.64% reached in Q3 2018. This has been quite helpful to Canadian Western Bank, as about 90% of its revenue came from net interest income. However, we saw a decline in NIM of 3 basis points sequentially in Q4 2018 (see chart below). The decline was primarily due to competition for deposits.

Source: Created by author; Q4 2018 Supplemental Information

Looking forward, we believe the pace of rate hikes will slow down. This is because Canada’s central bank has recently switched from a more hawkish tone back in October to a much more dovish tone on Dec. 5, 2018. In the statement that BoC released, it says:

Signs are emerging that trade conflicts are weighing more heavily on global demand… the global economic expansion is moderating.

Many analysts believe that the message is quite clear: Rate hikes are off the table for now. Therefore, we believe it will be a challenge for Canadian Western Bank to expand its NIM in 2019. If competition for deposits intensifies, the bank may even see its NIM compress in 2019.

Higher loan exposure to Alberta

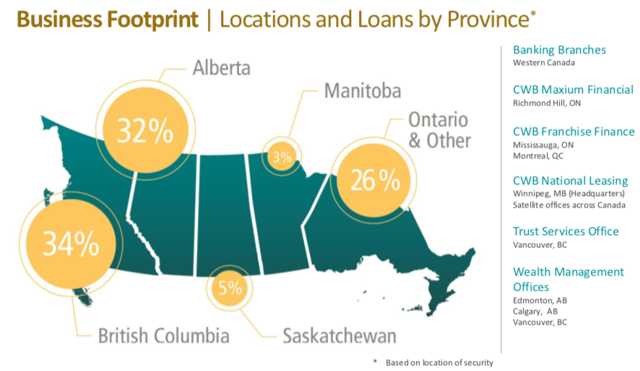

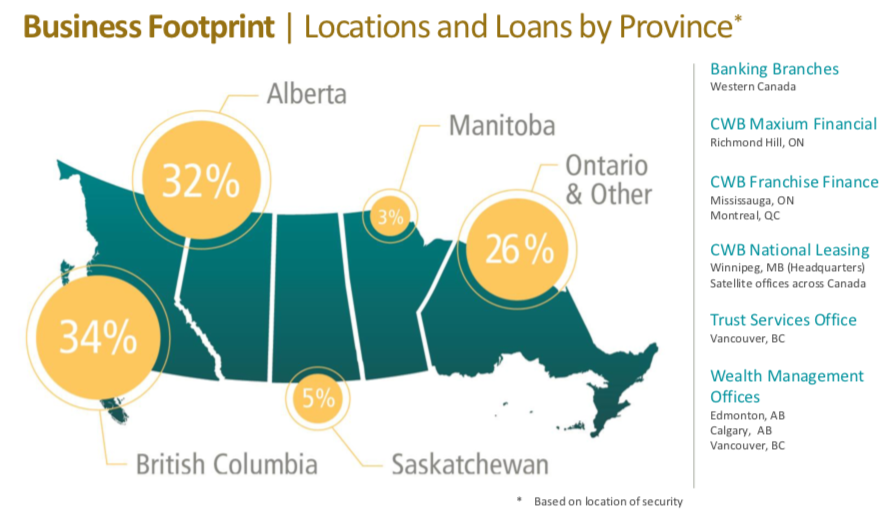

The map below shows Canadian Western Bank’s business footprint in Canada. As can be seen from the map, about 32% of its loans are from Alberta and about 5% of its loans are from the province of Saskatchewan. These two provinces’ economies are closely related to the prosperity of the energy sector.

Source: Q4 2018 Investor Presentation

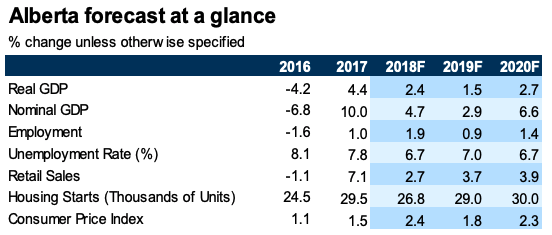

On the one hand, just as Canadian Western bank should enjoy relatively good loan growth during the energy boom, it can also be seen that its loan growth diminished during an energy market downturn. While Alberta’s economy has recovered strongly in 2017 and in the first half of 2018, this growth rate is expected to moderate considerably in 2019. There are two factors that will likely impact the province’s GDP growth in 2019. First, Alberta continues to face pipeline bottlenecks as it struggles to ship its oil to markets overseas. Second, the recent decline in energy prices will likely weigh on business investments. RBC Economics put this quite well in the following quote:

Pipeline bottlenecks and soft prices add to oil and gas woes. Those woes will cause growth to decline to 1.5% in 2019 from 2.4% this year. But there is light at the end of the tunnel. An expansion in pipeline capacity bodes well for growth in 2020, with the economy bouncing back to 2.7%.

Hence, we believe the slowdown in GDP growth in Alberta will likely limit its loan growth in 2019.

Source: Provincial Forecasts by RBC Economics

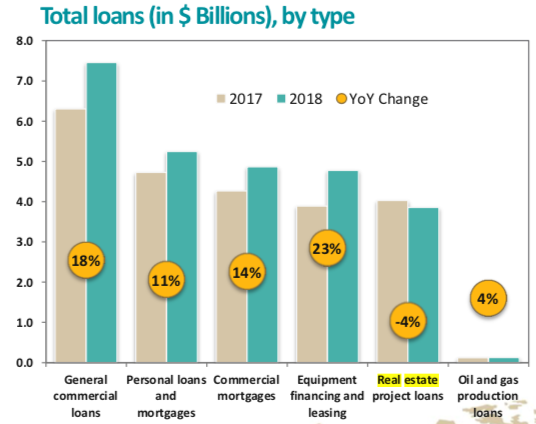

Real estate project loans may continue to decline in 2019

Real estate project loans currently represent about 15% of Canadian Western Bank’s total loans. However, this is the only type of loan that saw a contraction in volume. As can be seen from the chart below, Canadian Western Bank’s real estate project loans declined by 4% in 2018.

Source: Q4 2018 Investor Presentation

Looking forward to 2019, we think it will remain a challenge for Canadian Western Bank to grow its real estate project loans. In British Columbia, we are already seeing declines in housing starts in 2018. The province’s 2018 projected housing starts are expected to decline by 9.2% year over year (see table below). This number is expected to decline to 38 thousand (or by 4.3%) in 2019. In Ontario, new housing starts are expected to decline by 10.7% in 2019. Therefore, we think it will be a challenge to grow its real estate project loans in 2019. The most likely scenario will be a decline.

|

(Thousands of Units) |

2017 |

2018F |

2019F |

|

British Columbia |

43.7 |

39.7 |

38.0 |

|

Ontario |

79.1 |

78.4 |

70.0 |

Housing Starts (Source: Created by author; RBC Economics)

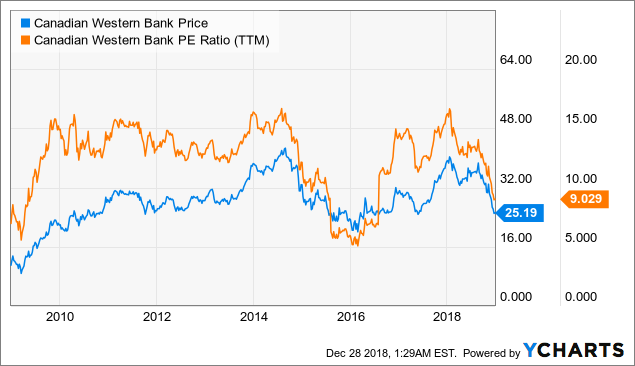

Valuation Analysis

Canadian Western Bank is currently trading at a P/E ratio of 9.0x. This is significantly lower than its 5-year average P/E ratio of 12.6x. As the chart below shows, the bank’s P/E ratios fell back down to near 5x twice. The first time was back in 2009 during the Great Recession. The second time was in 2016 when the energy market crashed. Other than these two events, shares of Canadian Western Bank have usually traded at P/E ratios above 12.0x. Therefore, we think its share price is significantly undervalued.

Source: YCharts

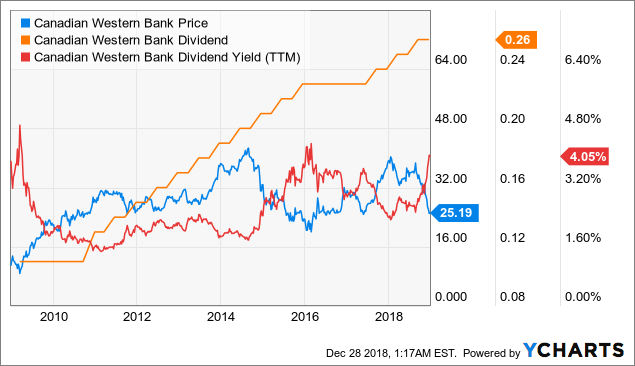

4.1%-yielding dividend

Canadian Western Bank currently pays a quarterly dividend of C$0.26 per share. The company has frequently increased its dividend in the past 10 years except during the aftermath of the financial crisis in 2008/2009 and the crash of crude prices in 2015/2016. As can be seen from the chart below, its current dividend yield of 4.1% is towards the high end of its 10-year yield range.

Source: YCharts

Risks and Challenges

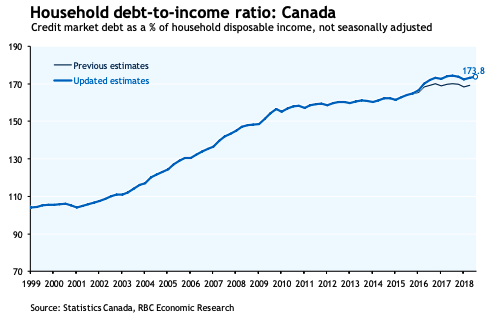

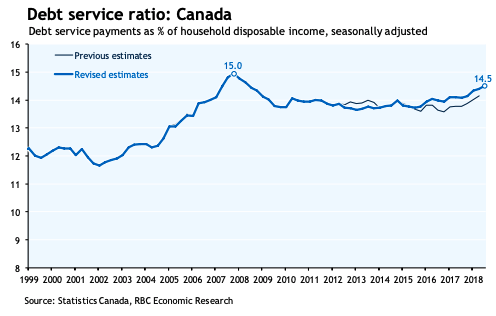

Canadian Western Bank’s business can be impacted negatively in a recession. In a recession, it’s likely that Canadian Western Bank will experience higher credit losses especially due to its higher exposure in Western Canada. In addition, the bank’s business can be impacted negatively if Canada’s housing market declines further. This is because the Canadian household debt level already is quite elevated (see chart below). In fact, its household debt-to-income ratio is now the highest in decades. A drastic decline in house prices might cause a spike in its mortgage default rate.

Source: RBC Economics

Source: RBC Economics

Investor Takeaway

Like many other Canadian peers, Canadian Western Bank faces the challenge to maintain its top and bottom line growth rates. Although the bank is significantly undervalued, we prefer other Canadian banks that have less exposure to Western Canada because the economy in the region is heavily dependent on the volatile energy sector. Therefore, we think conservative investors should seek other less risky alternatives.

Note: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment