With clinical data of a Phase 2 study to be released by mid-2019, Anchiano Therapeutics (ANCN) seems a great name to be followed in the next six months. Keep in mind that if the numbers are beneficial, the upward reaction in the stock price could be quite memorable. In addition, the financial statements reported seem also beneficial. In 2018, the company received the attention of several investors that provided money in the form of warrants and shares. Finally, after Merck & Co. (MRK) decided to buy one of the company’s competitors for $394 million, many institutional investors will have Anchiano under the radar.

Source: Prospectus

Source: Prospectus

Business

Founded in 2004, Anchiano is a biotechnology company focused on the development of gene therapies to treat bladder cancer. The company’s biologic agent, inodiftagene, seems to be a solution for patients not responding to other options due to problem of toxicity or effectiveness.

Source: Company’s Website

After obtaining Phase 2 clinical trial results, the company’s research is at an advanced stage. In addition, the results seem quite beneficial. After the company’s treatment, researchers were able to observe substantial anti-tumor activity. According to the prospectus, 33% of bladder cancer patients responded to the inodiftagene treatment. Furthermore, after a time period of one year and two years, the free survival rates were 46% and 33% respectively.

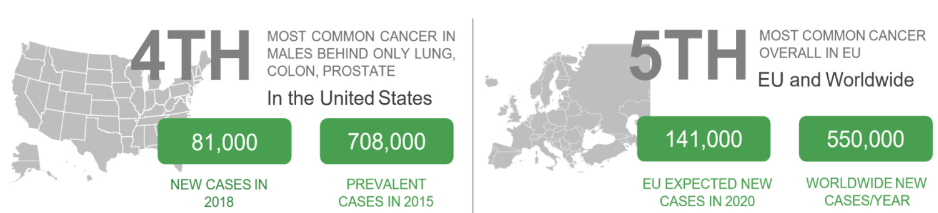

The market opportunity seems huge. Only in 2018, 81,000 new cases of the target medical condition were diagnosed in the US. In addition, in the EU, researchers expect to have around 141,000 new cases in 2020. If the company’s treatment can obtain approval in the US, the EU, and Japan, the total target market for inodiftagene should be close to $1.5 billion. Obtaining approval is a huge challenge as no drug has received FDA acceptance for the treatment of non-muscle-invasive bladder (“NMIBC”) cancer since 1998. The image below provides further details on the total market size:

Source: Prospectus

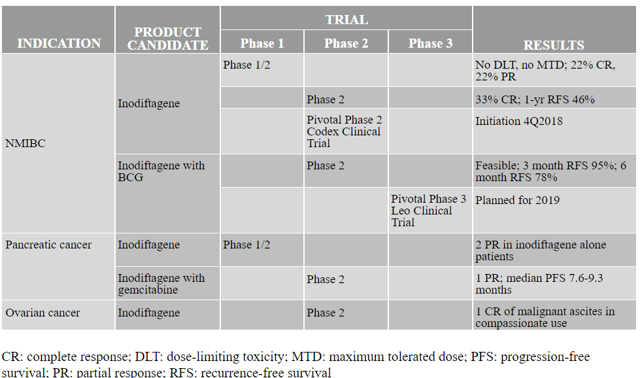

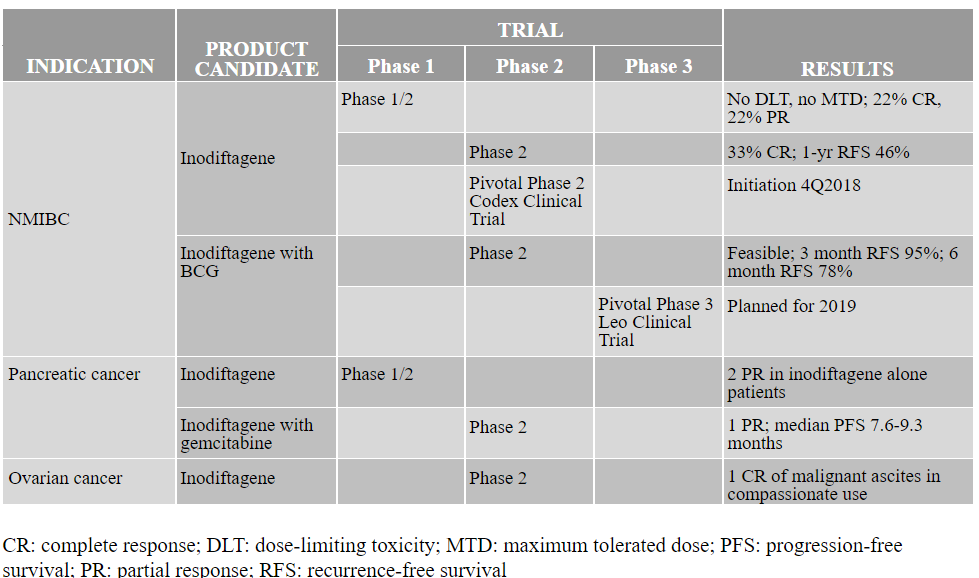

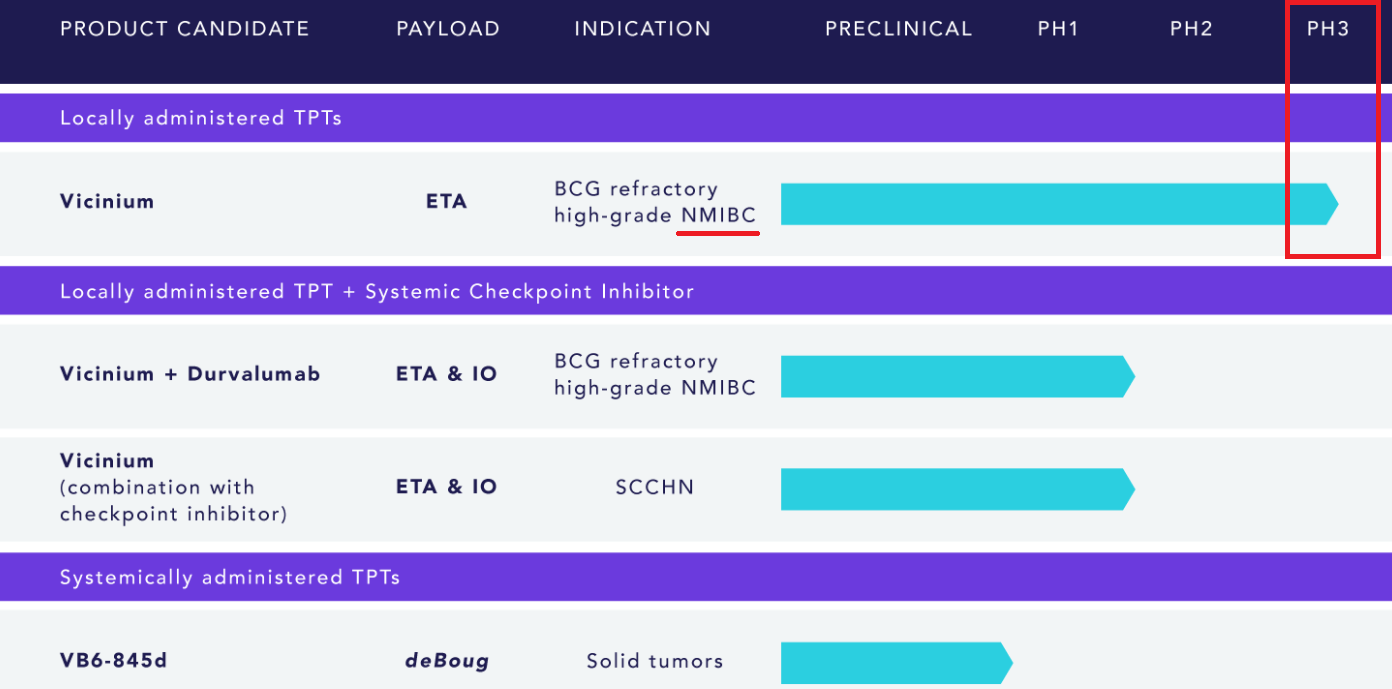

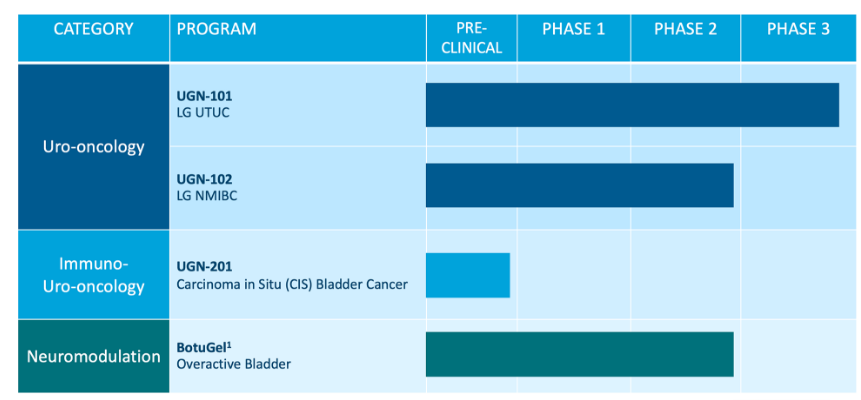

Having said this, Anchiano is targeting other conditions like Pancreatic cancer and ovarian cancer. As a result, the company’s market opportunity could be larger than $1.5 billion. Investors should also appreciate that in 2019, there are events that could make the stock price run. The company initiated a Pivotal Phase 2 Codex Clinical Trial in Q4 2018, and initial data from the study is expected by mid-2019. There is also a Pivotal Phase 3 Leo Clinical trial that is planned for 2019. If the results of these studies are beneficial, shareholders should benefit. The image below provides further details on the company’s pipeline:

Source: Prospectus

Inodiftagene For The Treatment Of Non-Muscle-Invasive Bladder

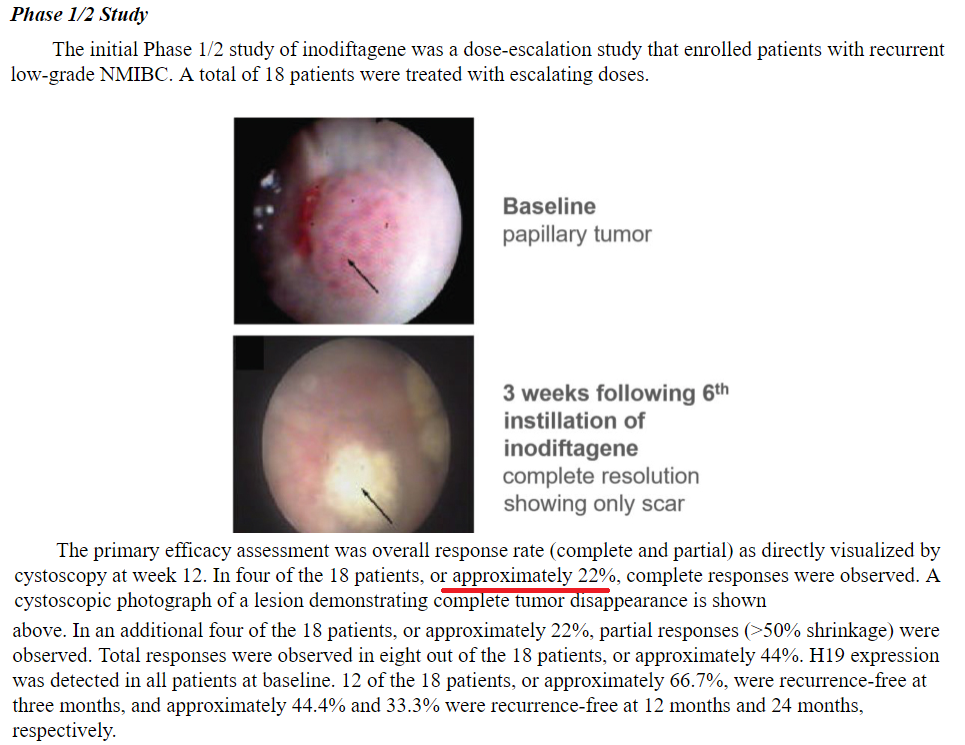

In a Phase 1 study that the company conducted with 18 patients, Anchiano was able to register complete responses in 22% of the cases. While the number of patients was low, these results seem quite interesting. The image below provides further details on this matter:

Source: Prospectus

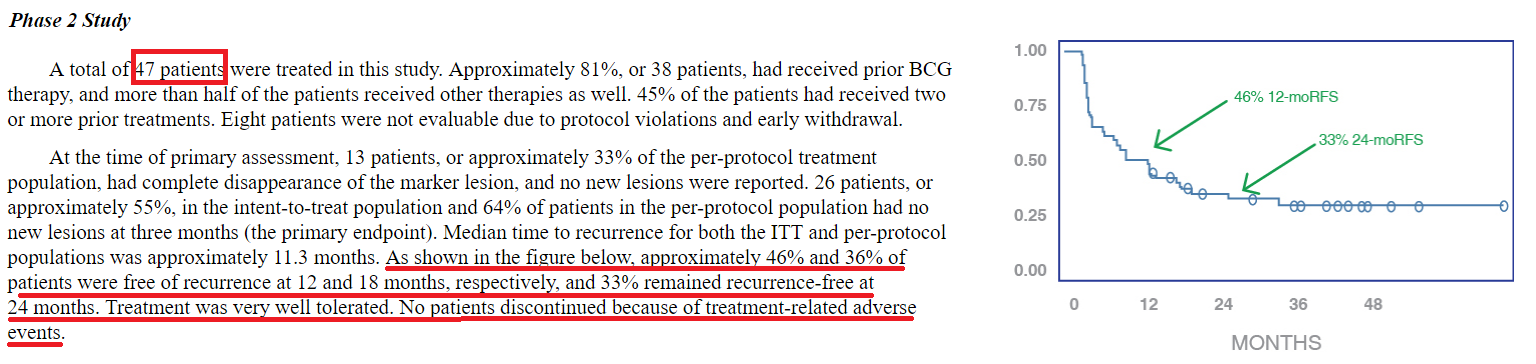

In a Phase 2 study of inodiftagene with 47 patients, no patient discontinued the treatment as a result of adverse events. As shown in the chart below, the results were very beneficial. The company was able to report 46% recurrence at 12 months, and 33% of patients were observed to be recurrence-free at 24 months.

Source: Prospectus

In another Phase 2 study conducted with 38 patients with standard medical treatment Bacillus Calmette-Guerin (BCG) and inodiftagene, Anchiano observed recurrence-free survival rate of 54%. Further details are provided in the lines and the table below:

Source: Prospectus

Balance Sheet And Recent Deal With Warrant Holders

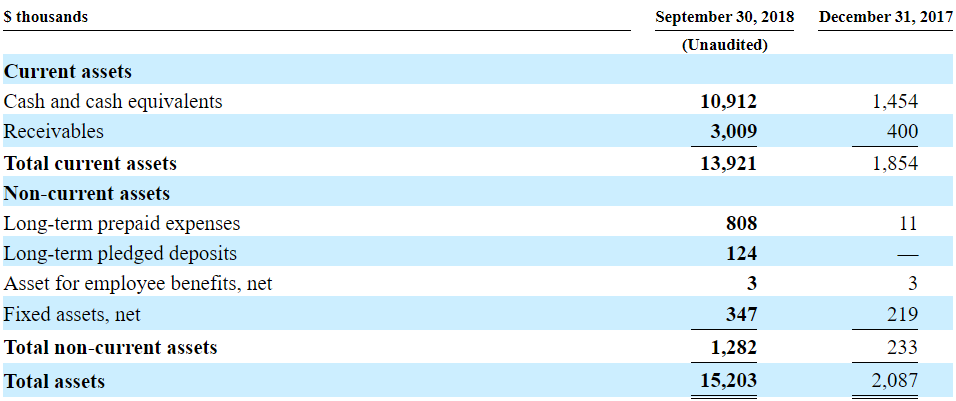

As of September 30, 2018, with an asset/liability ratio of 1.01x and $10.9 million in cash, the company’s financial situation seems very stable. It is interesting to see that the company received interest from investors in 2018. The amount of assets increased by 628%, from $2.08 million to $15.2 million. The image below provides the list of assets:

Source: Prospectus

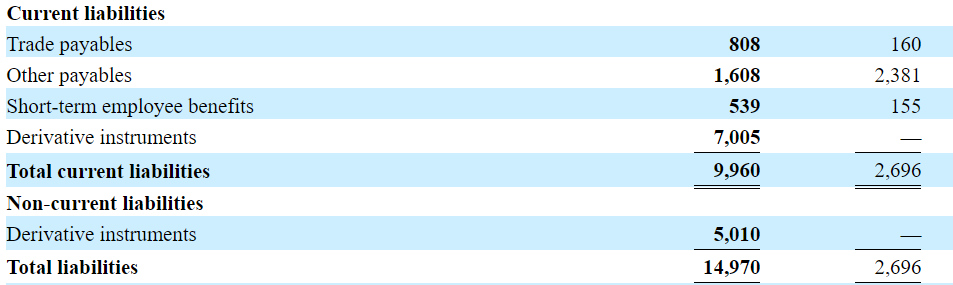

The list of liabilities should be studied carefully as the deal signed recently could have changed the situation of common stockholders quite a bit. Please note that the company reported derivative instruments of approximately $12 million, 80% of the total amount of assets. The list of liabilities is shown below:

Source: Prospectus

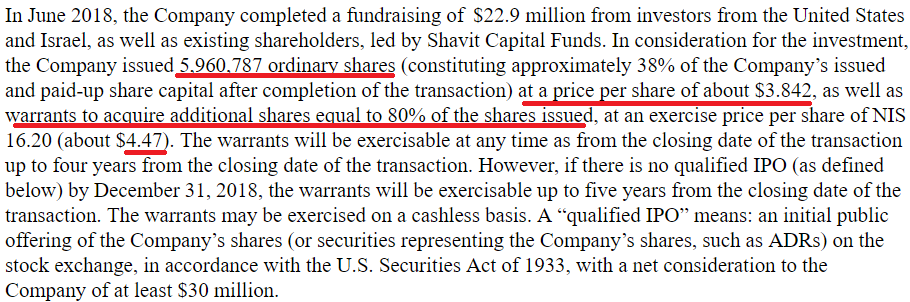

The lines below provide certain information about the total amount of shares sold, approximately 5.9 million at $3.84. In addition, Anchiano sold warrants to acquire shares at $4.47. This information seems quite relevant given the company is about to sell shares in a new IPO. This deal was executed in June 2018.

Source: Prospectus

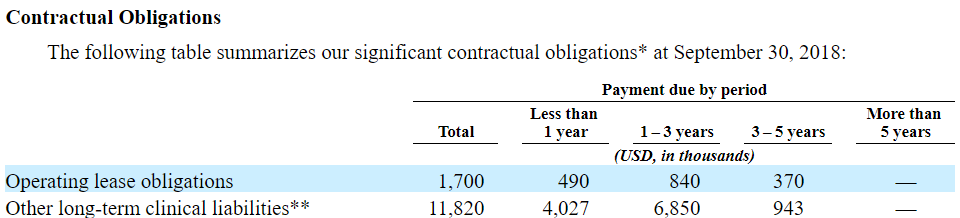

The warrants may not be considered debt. They should not worry investors. With that, it seems worth mentioning that the company has approximately $13 million in total contractual obligations including operating lease obligations and long-term clinical liabilities. The image below provides further details on this matter:

Source: Prospectus

Income Statement

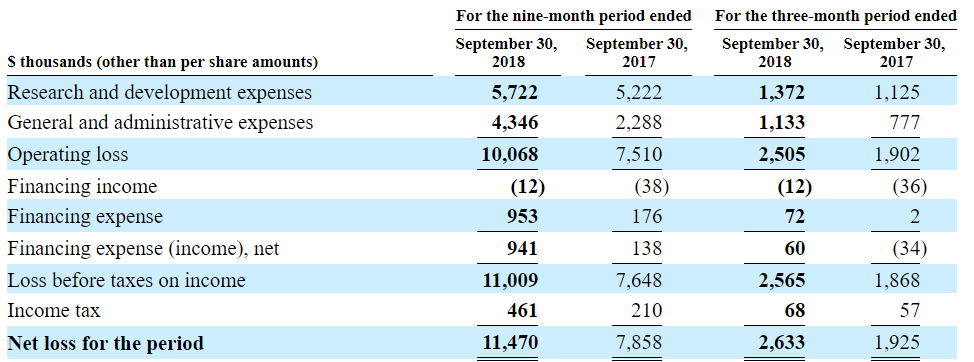

The amount of expenses is quite elevated, which should worry investors. For the nine months ended September 30, 2018, the company lost $11.4 million, which is more than the total amount of cash in hand reported in September. Market participants should understand that running out of cash should be quite detrimental for shareholders. Anchiano may have to sell further equity, which could lead to share price depreciation. The image below provides further details on this matter:

Source: Prospectus

Use Of Proceeds

The use of proceeds is beneficial. The company does not expect to use the proceeds to acquire shares from existing shareholders or to pay debt. The money will be used for the development of the company’s pipeline and for general corporate purposes. The lines below provide further details:

Source: Prospectus

Competitors

Companies that are conducting programs, which could compete with NMIBC, were reported in the prospectus. Have a look at the following list:

-

Merck Sharp & Dohme Corp.

-

Sesen Bio Inc. (SESN)

-

Telesta Therapeutics Inc. (OTCPK:BNHLF) trades over the counter.

-

Viralytics Limited (OTC:VRACF)

-

AADi, LLC

-

UroGen Pharma Ltd. (URGN)

-

Halozyme Therapeutics, Inc. (HALO)

-

Astellas Pharma Inc. (OTCPK:ALPMF)

-

Cold Genesys, Inc.

-

Altor BioScience Corporation

-

FKD Therapies Oy

-

Nippon Kayaku Co. (OTCPK:NPKYY)

-

Spectrum Pharmaceuticals, Inc. (SPPI)

-

Taris Biomedical LLC

-

Handok Inc.

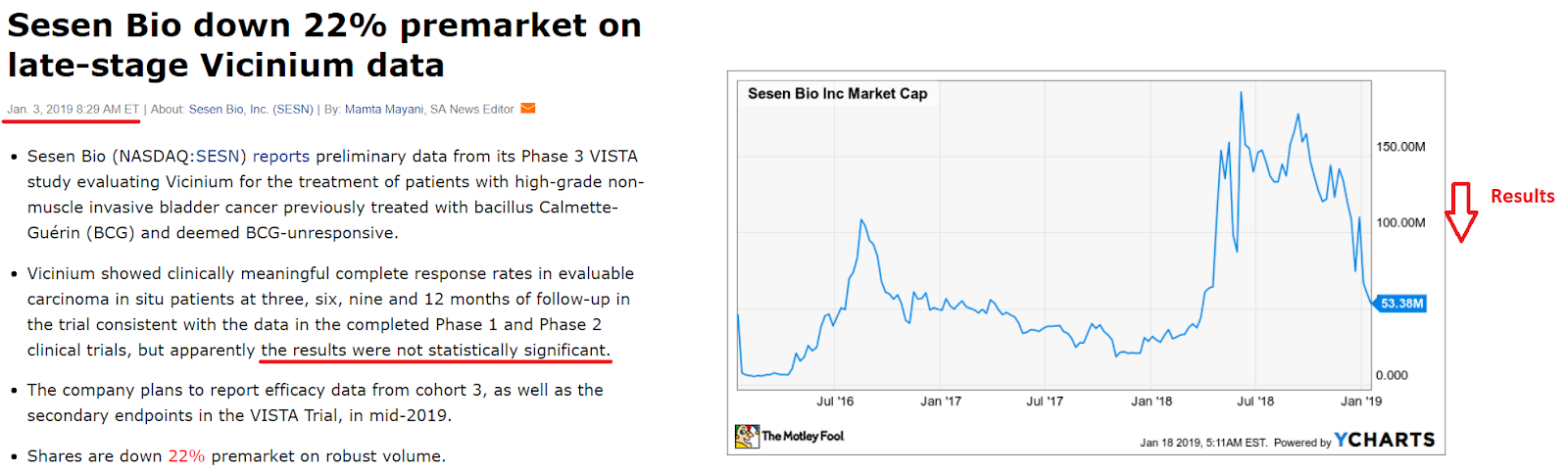

Among the company’s competitors, Sesen Bio Inc. seems to have a pipeline very similar to that of Anchiano. It has one program at Phase 3 of development targeting NMIBC, just like Anchiano.

Source: Sesen’s Website

As of January 18, 2019, Sesen has a market capitalization of $53 million with $57 million in cash and no debt. However, it should be noted that the company released new results, which were not statistically significant. As a result, the market capitalization declined quite a bit. Just before releasing the results, Sesen had a market capitalization of more than $150 million, thus investors should be expecting Anchiano to have a market capitalization of about $100-150 million. The image below provides further details on this matter:

Source: Seeking Alpha And YCharts

Viralytics Ltd. has several clinical trials at Phase 1 and Phase 2 of development, and Merck & Co. has agreed to buy it for $394 million. Investors should not expect Anchiano to report such a high valuation as the acquisition valuation includes the control premium. With that, it is quite beneficial that large groups are buying small companies operating in this space.

As shown below, UroGen has a pipeline much more advanced than that of Anchiano. It makes sense that its market capitalization equals $837 million. The valuation of Anchiano could reach these levels if the results to be released in 2019 and 2020 are beneficial.

Source: Urogen’s Website

Shareholders

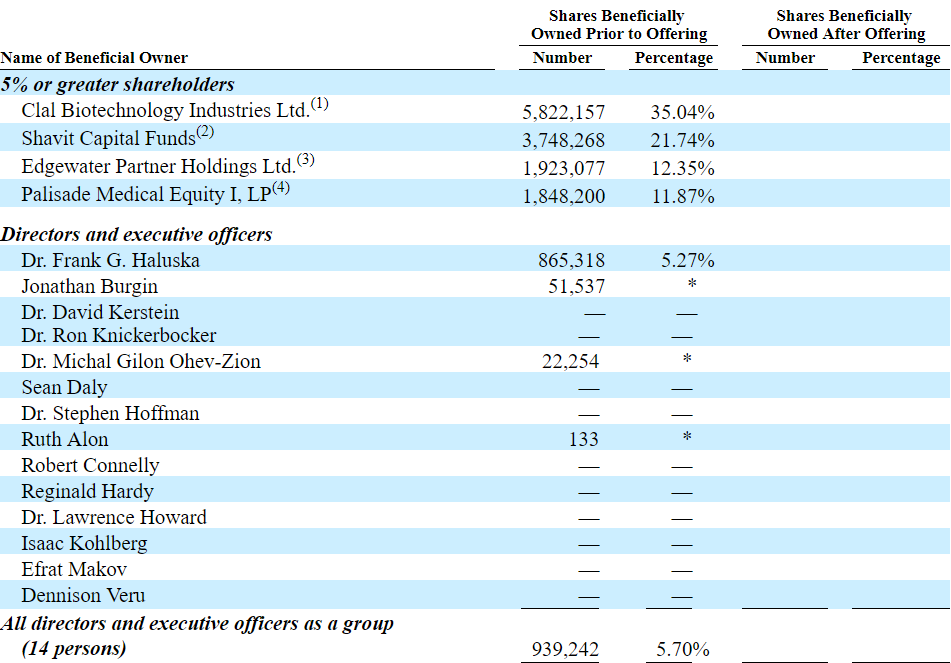

The assessment of shareholders is beneficial. The company was able to retain the attention of institutional investors before launching the IPO. As a result, many other investors will be interested in studying the clinical data obtained so far. The image below provides further details on this matter:

Source: Prospectus

Conclusion And Risks

With beneficial clinical data and two ongoing data to be released by mid-2019, Anchiano seems a name that institutional investors should study closely. After the IPO, the company should have a market capitalization of about $100-150 million like Sesen had right before releasing its results in January. Additionally, from the financial perspective, the company seems beneficial. It does not show financial debt, and the total amount of liabilities and contractual obligations don’t seem worrying.

The largest risk for shareholders is receiving detrimental results from the ongoing Phase 2 study. If the company is not able to report good figures, the market would not trust the company’s drug candidate anymore. Like it happened in the case of Sesen, the share price may decline close to the level of its cash per share.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment