So far, we have analyzed the performance of Core Retail and Core Office segments of Brookfield Property Partners (BPY) and the related REIT BPR and delved into financial results. This part is devoted to the excessive debt as one of the possible reasons for very poor unit price performance.

How BPY got into debt

The management summarized during the 2018 Investor Day how the debt has grown to exceed their targets by 20-30% (debt/EBITDA 13x instead of 10-11x and debt/capital 60% instead of 50%). I will paraphrase it here.

So, the good news is … those five transactions that I spoke about earlier [privatizing Canary Wharf, Brookfield Office Properties, Rouse Properties, GGP] required significant amounts of capital to get them executed. As a result of that, in our own capital allocation decisions, we had to make decisions between doing things like buying back our units or reducing leverage, versus doing these strategic transactions. They’re all done. We’re finished. We’ve completed all of those transactions. The business looks the way that we want it to look.

A notable disadvantage of excessive leverage is that it is hard to get away from it – the higher risk increases borrowing rates which digs the company into an even deeper hole and leads to a depressed share price which makes issuing equity very uneconomical. It is thus much easier to avoid such troubles beforehand than to get out of them when one is already struggling. BPY has failed to do so and is now in a position where they basically have to rely on a long period without significant turmoils to get back on track. This is their plan:

We are now in a position to improve these [credit] metrics. In the short term, this will come from selling incremental malls and repaying the acquisition debt that we put in place to acquire GGP. It has already come from converting some of our capital securities into units of BPY and allocating any available capital that may come from our recycling of capital activities to reduce corporate debt.

In the near-term, this will come from adding over $500 million of earnings from the completion of our development pipeline. At 11 times debt to EBITDA, that’s almost $6 billion of debt, most of which is on our balance sheet already today without any associated earnings.

We’re also going to convert the $1.8 billion of capital securities that we issued in 2014, when we acquired Canary Wharf into units of BPY. And, allocating the liquidity that we generate from our LP investments over the next few years, we’ll allocate a good portion of that to incremental deleveraging.

So, if you combine that with an increase in equity as a result of our increased earnings outlook, during that period, that will put us in a great position to meet or beat our targets by 2022, if not sooner.

As for the preferred shares, these are convertible in 2021, 2024 and 2026 (depending on the series) and amount to only $1.8B, so we can safely forget them as a means of reducing leverage. The other means are more useful, but I find targeting 2022 woefully inadequate in light of the numbers discussed later.

Scenarios

When thinking about the future, I like the probabilistic paradigm often promoted by N. Taleb: the future is a range of scenarios, some of them more likely than others. Any action you do at present has different consequences in different scenarios, and it is usually very useful to avoid focusing on a single scenario as people typically do (confusing probable with sure to happen and unlikely with impossible).

Let’s have an example of such thinking. When I buy a life insurance policy, it will detract a bit from my financial well-being in most scenarios, but incredibly help my family in some dire ones, and will not help at all in some very unlikely scenarios that are excluded from common life insurance coverage (e.g. terrorism or war). If the insurance company has not failed their job, then on average I am losing a bit of money which they earn as a profit. That might not be my primary concern and I may be willing to pay that small sum for the ability to shift outcomes between the scenarios.

In this way, one can analyze education, having children, or, of course, investments. There are many companies with fortress balance sheets which will have no trouble surviving adverse conditions. There are others that have tried to minimize the probability of debt killing them, but are not willing to entirely sacrifice its usage and the resulting enhanced returns for survival in the most dire scenarios (probably a majority of companies belong to this category). And then there are those that care only a little about surviving and are mostly focused on enhancing returns in good times (e.g. some leveraged closed-end funds). It is just up to the investor to combine possible investments into a portfolio that are most suited to his goals.

What I am quite sure about is that I care a lot more about surviving hard periods than about maximizing returns. Consequently, I want to own excessively leveraged companies only in limited amounts.

As for BPY, we will see that their debt load is really excessive and it belongs to the third category mentioned above. Without being backed by BAM, it would be a doubtful investment. The unit price is so low, however, that the expected return is quite attractive compared to most other options. I am therefore using it to enhance my returns (especially cash-flows) in good times, but do not rely on it at all during bad times.

Opportunistic LP investments

Over the last 5 years, a significant drain on BPY’s cash flow was created by their investments in Brookfield Asset Management’s (BAM) opportunistic real estate funds in which BPY is a limited partner (30% share in BSREP I, 25% share in BSREP II; and a similar share in a couple of other funds, see pages 50-53 in ID 2018 presentation or pages 27-28 in the 3Q18 report). Altogether, $2.7B was invested and only $1B has been paid back yet. Both of the BSREP funds are now fully invested. Over the next 5 years, net cash inflow of $5.8B from LP investments is anticipated, and that could really help to delever. Unfortunately, this cash flow is back-end loaded, that is, of little help at present, especially if a recession strikes and the monetization of the opportunistic portfolio slows down.

Borrowing strategy

Since 2016, BPY is rated BBB (recently reaffirmed), and S&P is content with their debt levels even around 13x debt/EBITDA:

The stable outlook reflects our expectation that pro forma for the GGP acquisition consolidated BPY credit metrics will improve modestly with debt to EBITDA declining to 13x area and FCC strengthening to about 1.5x. …

We could downgrade BPY if credit metrics deteriorate because of a delay in asset sales, weakness in the portfolio performance, or if BPY pursues more aggressive financing to expand their portfolio through debt financed acquisitions such that debt to EBITDA weakens toward the 15x area, pro forma for the GGP acquisition, or if the company does not maintain FCC of at least 1.3x over the next year. (source)

It is interesting that the rating agency is so agreeable. When I am thinking about debt as an owner, I like to imagine various stress-test scenarios and ask questions like “How long can the company go without issuing new debt?” or “What happens to distributions if interest rates go up this much?”. This does not seem to be what rating agencies are doing (we will discuss it later).

Before asking such questions for BPY, it should be noted that most of BPY’s debt is asset-level and non-recourse. The CEO’s words make their leveraging strategy sound quite reasonable:

Of course, our businesses do fund themselves by putting investment grade debt on almost every asset they own, but they do that to achieve the best risk adjusted return on your equity. I think this is indicative of the quality of the assets and the liquidity of the markets that we operate in. With 50-60% loan to value on every asset, our leverage targets are really set using a bottom-up approach not a top-down approach.

The fact that the debt is non-recourse does not mean they can just walk away from it. Legally, they could, but the reputational risk is high and they might face various restricting covenants in the future if they did. Well, it is also true that institutional memory is sometimes very short, so they might easily find new willing lenders, but I think BAM would make every effort to avoid denting their reputation in the first place. S&P obviously thinks that too and the rating is actually one notch above what they would assign if there was no BAM parenting BPY.

I mostly consider the non-recourse nature of the borrowings as a protection from major catastrophic events like, say, Brazilian government expropriating their assets (in which case they can just walk away from the locally issued debt, too).

Cash flows vs. debt

BPY has a policy of distributing most of its earnings. At the first glance, it looks a bit like they are distributing even more than the earnings. It is actually quite hard to find a suitable cash flow measure to judge this. For instance, they explicitly state in annual reports that they do not consider FFO to be a measure of cash flow, but then use CFFO, guess what, as the basis for the proportionate cash flow statement (page 17 in 2Q18 supplemental info). That statement essentially only demonstrates that the cash flow is totally distorted by at least three different components: divestitures/acquisitions, debt repayment/issuance, and changes in working capital. All of these are prone to timing differences that make quarterly or even yearly data meaningless, and the GPP acquisition just kills any attempt at analysis. One has to wait for the 4Q18 results to have at least a quarter of data to crunch, but even then I am skeptical.

The accounting itself does not help either: cash flows from equity-accounted subsidiaries do not show in operating cash flow and accounting for the LP investments in funds with kind of random realization of gains only adds to the murkiness.

I have decided on the following: I will use CFFO plus interest expense as a proxy for EBITDA and then add $500M of anticipated realized LP gains on top of it to have some estimate of the cash flow generated by BPY that is available to service debt. Let’s call it total cash flow (TCF). (Caveat: we don’t care about any asset maintenance here, this is only for the purpose of checking solvency.)

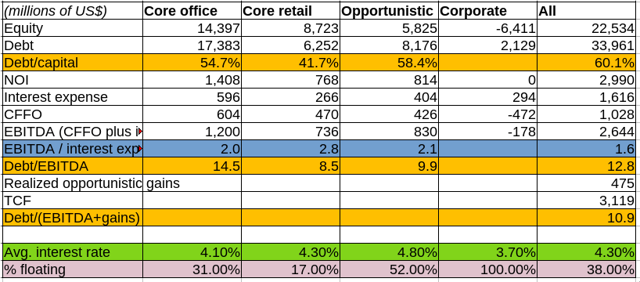

I think that the most useful data are those reported in 2Q18 for individual segments. The GGP acquisition has shifted the mix more towards retail which helps the credit metrics. I will annualize the numbers for 1H18 (multiply them by 2) to get yearly figures.

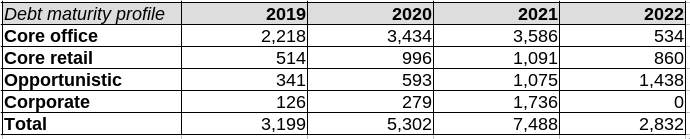

The conclusion is that we have ~$3.1B of TCF, of which $1.6B goes away just to pay interest on the debt, which leaves only $1.5B for distributions ($0.9B), maintenance ($0.5B) and all other purposes. When we compare this to the debt maturity profile (see the table below), we see that BPY is in a position quite precarious: even if they did not pay any distributions or maintenance, they will still have to issue at least $1.5B of new debt in 2019 to refinance the maturing portion. It gets way worse in 2020 and 2021. They might call their maturity profile laddered, but that will only refer to relative sizes of annual maturities; the fact is that every year they have to repay much more than they earn over that year. In other words, they are extremely heavily reliant on access to credit markets.

I have not seen such a company in quite some time. Compare it with Kinder Morgan (KMI) that was threatened by the loss of investment-grade rating in 2015: they had more than $4B of yearly DCF, that is, cash flow available after paying interest expense (and most of that secured by long-term contracts), and only $2-3B of debt maturing each year – it looks like a financial fortress compared to BPY. It is true that BPY has properties to put a lien on, and nice ones, but imagine that cap rates go up a percent or two in a downturn. Consequently, values of those properties will go down perhaps 20%, and BPY is already at about 55% debt to capital within the office portfolio – would the banks be likely to extend that even further, lending more than 70-80% of the market price of the mortgaged property on favorable terms?

I have not seen such a company in quite some time. Compare it with Kinder Morgan (KMI) that was threatened by the loss of investment-grade rating in 2015: they had more than $4B of yearly DCF, that is, cash flow available after paying interest expense (and most of that secured by long-term contracts), and only $2-3B of debt maturing each year – it looks like a financial fortress compared to BPY. It is true that BPY has properties to put a lien on, and nice ones, but imagine that cap rates go up a percent or two in a downturn. Consequently, values of those properties will go down perhaps 20%, and BPY is already at about 55% debt to capital within the office portfolio – would the banks be likely to extend that even further, lending more than 70-80% of the market price of the mortgaged property on favorable terms?

As far as I know, the asset-level debt is mostly comprised of mortgages (i.e. it is amortizing), and apparently with a rather short term (5 years on average). The $3B of NOI is much smaller than the cash flow required for servicing the mortgages. Such short maturities might fit into their operating model based on extensive asset recycling, but I do not understand why they did not utilize the last decade to get at least some very cheap really long-term debt. (For instance, only 4 U. S. office properties have debt maturity extending beyond 2025.)

On credit ratings

I have spent some time trying to figure out why a rating agency would approve of this. It seems to me that they base their conclusions on their models and assumptions (see below) and do not assign the rating on anything resembling a worst-case scenario. Essentially, the rating is descriptive, not predictive – they will just lower it if conditions worsen and tick their “well done” box. They did the same with CLOs in 2008 – they kept them at AAA based on some model assuming mild future growth and then suddenly downgraded them to junk as the bottom fell out in real estate markets.

Their assumptions for BPY are as follows:

- real global GDP growth of 3.8% in 2018 and 2019;

- real U.S. GDP growth of 2.8% in 2018 and 2.2% in 2019;

- total same-store revenue growth in the 3.0% area in 2018 and 2019;

- acquisitions of approximately $1.0 billion to $1.5 billion in 2018 and 2019, excluding the acquisition of GGP;

- development funding of approximately $1.0 billion per year;

- dispositions of approximately $4.0 billion in 2018 to fund the GGP acquisition, and $3.2 billion in 2019.

Thus they are basically only saying that “if the economy grows nicely and everything goes according to the management’s plans, it would be fine”. This is not exactly how an investor should assess risks, in my humble opinion. When have you last met a CEO anticipating that his strategy will lead to a default?

The problem with such model predictions is pervasive in economics. We are good at projecting the past and present into the near-term future, but spectacularly fail to predict disruption and sudden changes. In contrast, Buffett takes an arguably reasonable stance of avoiding macroeconomic models and predictions altogether and thinking about risk in terms of what can go wrong and how likely it is instead.

A simple exercise of this kind shows that if interest rates rise to ~6%, BPY will not have enough money to pay its distributions. When we take into account maintenance-related expenses, which were about $0.5/unit over the last 12 months (see “Payout” in supplemental info), or $350M a year, we get to just 5%. With ~38% of their debt in floating rate, just a 2% increase in rates will immediately raise their average cost of debt from 4.3% to 5%, threatening the distribution.

I actually do not believe that even then the distribution will be cut – they will try to increase it as planned, but the reason for that is definitely not a strong financial position but the fact that such an action will benefit BAM in the long term. (For the short term, BAM can help to decrease the debt burden, e.g. by waiving some fees as they did at the time of the GGP acquisition, or by a cheap temporary loan.)

The partnership has a number of alternatives at its disposal to fund any difference between the cash flow from operating activities and distributions to Unitholders. … The partnership may access its credit facilities in order to temporarily fund its distributions as a result of timing differences between the payments of distributions and cash receipts from its investments. Distributions made to Unitholders which exceed cash flow from operating activities in future periods may be considered to be a return of capital to Unitholders as defined in Canadian Securities Administrators’ National Policy 41-201 – Income Trusts and Indirect Offerings.

(source: 3Q18 report, page 34)

Liquidity

I do not want to create an impression that BPY is going to go belly up soon; that is definitely not so. Their business might deteriorate during a recession, but only a small portion of leases expire in any given year, so occupancy or NOI would only decline slowly.

At the end of 3Q18, liquidity stood at $6.5B (including construction credit facilities and funds in investments that BPY does not control). This is sufficient to fund near-term debt maturities (~$6B till the end of 2019), but again we see that the financial position is not strong since they have to rely on construction facilities and opportunistic asset disposals to fund liquidity needs if credit markets did not allow for a smooth debt rollover.

After the GGP acquisition

I have tried to get a financial picture of the business after the GGP acquisition, but have not really succeeded. The balance sheet was reported, of course, but I don’t know how to get run rates for income, NOI, FFO or cash flows. The best what I could find is this remark from 3Q18 report (Note 3, page 10):

In the period from August 28, 2018 to September 30, 2018, the partnership recorded revenue and net income in connection with this acquisition of approximately $129 million and $77 million, respectively. If the acquisition had occurred on January 1, 2018, the partnership’s total revenue and net income would have been $6,142 million and $3,413 million, respectively, for the nine months ended September 30, 2018.

I like the net income figure; it suggests that 2018 will be a successful year. (The actual proportionate net income was $1.4B for the first 9 months.)

In September, during ID 2018, they mentioned pro-forma debt to capital of 58%; in 3Q18 report they mention 52% (consolidated, page 37), and add the following comment: “It is our view this level of indebtedness is conservative given the cash flow characteristics of our properties and the fair value of our assets.” In my opinion, they are running the show with the maximum amount of debt one can call conservative. Without BAM, when judged only on their financials, they are barely investment grade.

The portion of floating-rate debt is 42% and a 100 bps increase in interest rates will increase interest expenses by $231M (the effect is partially mitigated by some interest rate swaps).

Conclusion

The key question is whether the higher risk is compensated by higher expected returns. The problem, of course, is that risk is not a single number; it can only be viewed through the whole range of possible scenarios.

If you are interested in survival in dire scenarios, then BPY might interest you only if you fully believe BAM will not let it fall (and won’t acquire it on the cheap when the bottom is hit), and then it might be better to invest in BAM anyway since prospective returns in almost any scenario are higher.

On the other hand, if you are interested in having nice income during a majority of favorable scenarios, BPY offers juicy 7.5% yield coupled with significant growth of 5%+, something quite attractive compared to almost any other REIT (or most other investments). Again, the security of this growth in mediocre scenarios where it is hard to recycle assets profitably mostly consists in reliance on BAM’s interests, not on BPY’s own solid financial footing. Apart from the cash yield, BAM’s prospects again look better in such scenarios.

The advantage of BPY against other high-yielding vehicles is the possibility of meaningful distribution growth over a wide range of scenarios. Leveraged junk bond CEFs, MLPs distributing all available cash flow, overleveraged companies in capital-intensive industries etc. are not less risky than BPY, but typically offer little or no growth at all and yield only a couple of percentage points more if anything at all. They also do not protect against inflation as well as BPY’s high-quality properties.

Considering that the stock market tends to be much more volatile than income and cash flows from high-quality properties, BPY might be suitable as a position in a portfolio that should produce at least some current income. In particular, one can use it to boost his cushion between income and mortgage payments if he has other means of dealing with unfavorable economic conditions (I have written an article discussing this portfolio strategy).

Disclosure: I am/we are long BAM, BPY. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment