The term SWAN (Sleep Well At Night) has been used ad-nauseam on Seeking Alpha, particularly in regard to REITs. There have been so many REITs that have been called SWANs that the term might as well mean: Here is a REIT I think is decent.

There are few if any investors who made it through the week without seeing a lot of red in their portfolio. While they can be extremely painful in the near-term, bear markets often provide opportunities for long-term investors to buy very high-quality stocks at prices that are rarely seen.

To me, the idea of a SWAN stock is an investment where I do not have to worry how much or how long it is in the red because the underlying company is so solid that no matter how bad the damage is, it will rebound when the storm is over.

For REITs, these are the companies that are very likely to maintain, or even grow, their dividend through even the worst downturns. They are companies that will be able to access credit, even when lenders tighten up. They are companies that will not be forced to sell properties if property values decline. They have enough organic cash-flow that they do not need to expand and can hunker down until the time is right to start buying up properties at low prices.

In a recent article, I listed 5 REITs that I consider to have SWAN status. Essex Property Trust (ESS), Realty Income (O), American Tower Corporation (AMT), Public Storage (PSA) and Prologis (PLD). Regular readers of mine will notice that I rarely write about these tickers. That is because there is rarely anything interesting to say about them. All 5 of these companies just keep doing what made them great. They are the kind of investments that you can buy and forget because there is unlikely to be some huge surprise.

The very factors that make them boring to write about are the same ones that make them excellent investments to hold through and buy during bear markets. Looking at my article history, I realize I might have been remiss in ignoring these companies. It makes it look like my investing is far more aggressive than it actually is since I tend to write about the riskiest tickers I invest in.

ESS

ESS is a multi-family REIT that invests in apartment complexes in the West Coast.

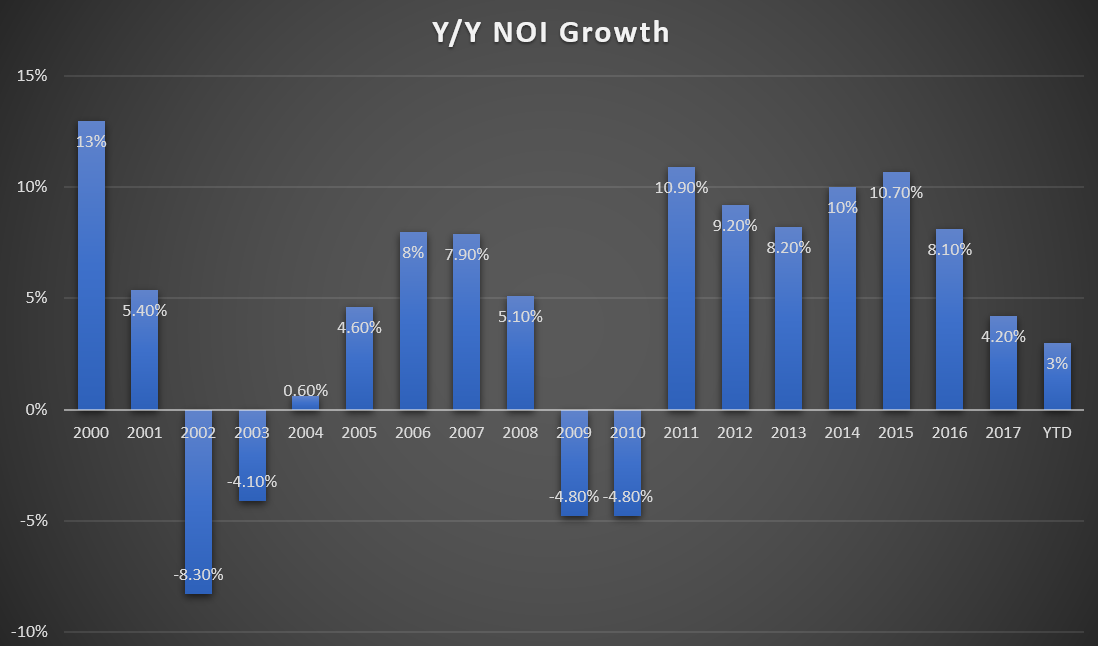

They focus on metro areas which have high barriers to new housing construction as well as inherently strong demand. These fundamentals have allowed ESS to experience strong same-property NOI growth.

Source: Q4 YoY NOI growth from quarterly supplementals

Source: Q4 YoY NOI growth from quarterly supplementals

While there is no escaping the real estate cycle, the strength of ESS is that they invest in areas where people want to live and there are significant physical as well as political barriers to new supply. Even through recessions, these areas have proven that they will bounce back.

Balance Sheet

REITs are designed to distribute the majority of their cash-flow to shareholders through dividends. The result is that issuing equity to raise capital for acquisitions is a frequent occurrence. Ideally, an equity issuance will raise enough capital that the new investments will not only cover the dividend for the new shares but will also increase per-share FFO for legacy shareholders.

When share prices fall, issuing new shares can become dilutive, meaning that the funds from shares issued cannot be invested to return enough cash-flow and legacy shareholders will see their FFO per share decline.

During a recession, one of the most common reasons that a REIT will issue shares even when it is dilutive to current shareholders is the need to deleverage or to pay off maturing debt. In a bull market, utilizing high levels of leverage can improve performance. When the market turns bearish, high leverage can spell disaster by forcing the REIT to issue equity when conditions are poor.

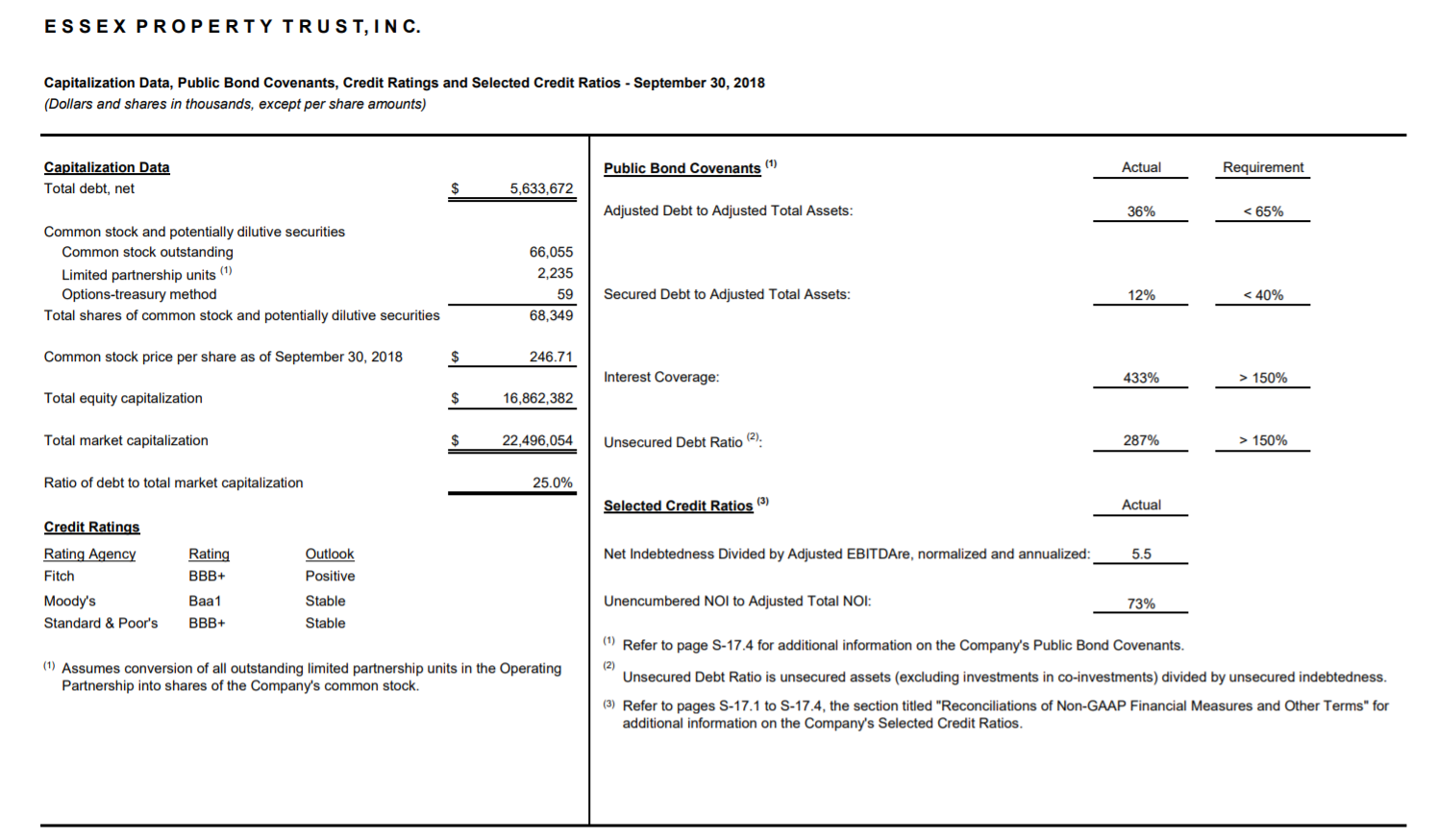

ESS maintains a modest leverage level of 5.5x Adjusted EBITDAre and as you can see, they have a healthy cushion on all of their covenants.

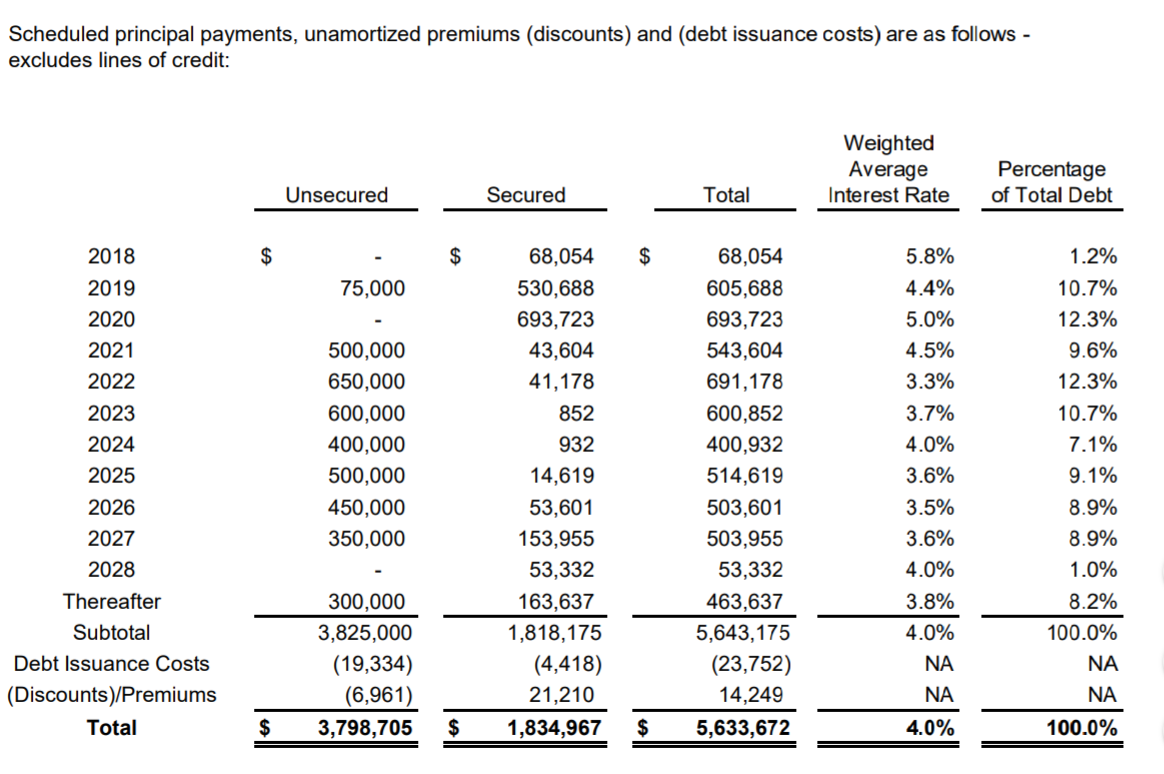

Looking at their maturity schedule, ESS does not have any significant lumps. They have a consistent $400-$700 million maturing per year and a $1.2 billion revolver that is currently undrawn.

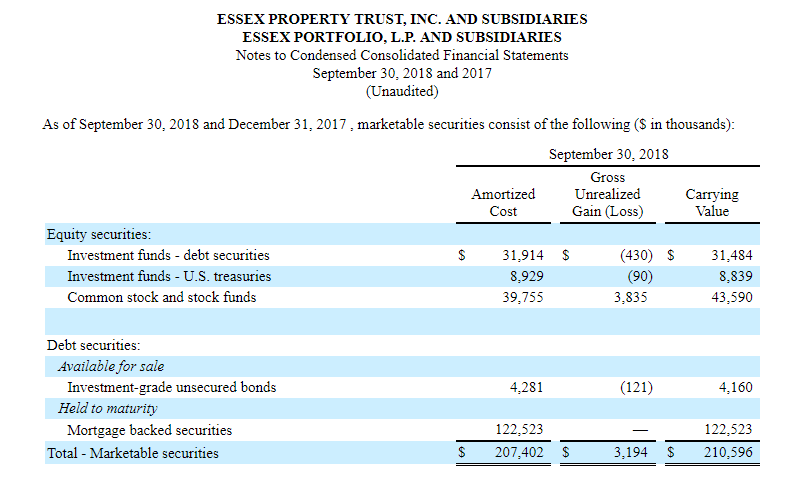

With a significant portion of their debt unsecured, ESS has significant flexibility to refinance even if the credit markets start to tighten up. Additionally, ESS maintains a series of more liquid investments which could be sold with no impact on their core operations.

ESS is well positioned to weather a downturn.

FFO/Dividend Growth

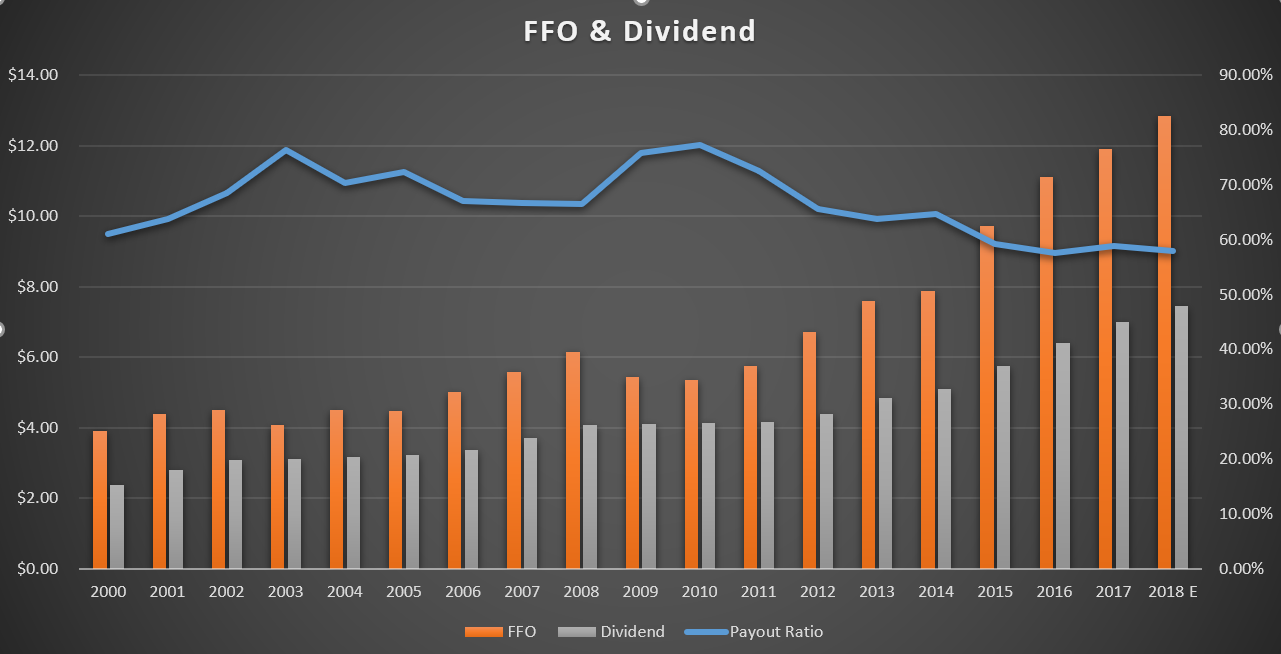

One of the big attractions of REITs for retail investors is their dividends. I would argue one of the most important aspects for SWAN status is the ability and willingness to continue paying the dividend. From 2008-2010, many REITs cut their dividends as their FFO dropped. ESS beat that trend, and actually raised their dividend through the recession.

One of the big attractions of REITs for retail investors is their dividends. I would argue one of the most important aspects for SWAN status is the ability and willingness to continue paying the dividend. From 2008-2010, many REITs cut their dividends as their FFO dropped. ESS beat that trend, and actually raised their dividend through the recession.

Like other REITs, ESS experienced a drop in FFO, per share FFO fell more than 20% from 2009 to 2010. Unlike most REITs, ESS was able to continue raising their dividend. While the 2010 increase was only a penny, even a very small raise provides reassurance in a recession.

Today, the payout ratio is lower than it has been in the last 18 years. If there is a recession in 2019, ESS has a very good chance of repeating what they have done in the last two recessions by raising the dividend a smaller amount with the payout ratio creeping higher but remaining manageable.

Share Price

ESS data by YCharts

ESS data by YCharts

While ESS managed to grow their dividend despite the recession, investors should realize that the share price was not so fortunate. Investors who were holding in 2008 saw their value drop 60% by early 2009. It took almost 3 years until mid-2011 for the share price to fully recover.

The recession in the early 2000s was less severe for ESS, with a drawdown of only 20%, and recovery in approximately 2 years.

It is important for investors to realize that a “SWAN” is not immune to the ups and downs of the economy or the market. Investors can still experience large unrealized capital losses, and if you have a personal situation where you have to sell, those losses could become realized.

What makes a SWAN is a company where the investor does not have to worry about daily price action, secure in the belief that the company will continue to pay the dividend, will continue to have strong fundamentals and that the share price will recover. For investors who have cash, investing during the depths of a recession, when many are fleeing, can lead to outstanding returns.

Conclusion

I consider ESS a SWAN because they invest in a sector and geographical locations which have very strong demand and limitations on supply. While those dynamics might be temporarily skewed out of favor, demand for residential housing on the West Coast is going to continue to grow long-term.

The area remains very attractive not only on an economic level but is also geographically attractive. Coastal California is going to remain on the short-list of places where people dream of living. While on the supply side, it is very likely that the barriers to new construction are going to remain and continue to strengthen. Over the long-term, ESS should continue to experience supply-demand dynamics that are very favorable to landlords.

In terms of their balance sheet, ESS has a conservative leverage level and a debt maturity schedule that provides them with a lot of flexibility. In the event of a recession, ESS can partially pay off debt, refinance, add collateral or sell off unencumbered properties for cash depending on what is best for the conditions.

Historically, ESS has raised their dividend every single year since IPO. Even during the 2008-2010 recession, which was a recession driven by real-estate, ESS continued raising their dividend. With the FFO payout ratio at multi-decade lows, ESS remains in a position where they should be able to maintain that track record.

Investors have to be prepared for the possibility that the share-price could experience a significant drawdown. However, there is a very good chance they can maintain their dividend and control the decline of their FFO.

Since ESS was in a strong position before the 2009 recession, they were able to take advantage of the situation by doing things like redeeming their Series G preferred at a nearly $50 million discount. They were also able to resume acquisitions in 2010, near the bottom of the market. Those moves provided significant long-term value to shareholders.

There is no safe harbor in a bear market, but there are those companies that manage their fundamentals and remain solid investments. When they become the baby being thrown out with the bathwater, investors can buy premium companies at heavily discounted prices.

Today, ESS is only about 10% off their high and I am not a buyer. If the bear market returns with a vengeance in 2019 and pushes prices down 20%-30%+, ESS is on my short list for flight to safety REITs.

Disclosure: I am/we are long O, PLD, AMT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment