NCS Multistage has limited headroom in short run

NCS Multistage Holdings (NCSM) provides engineered products and support services that optimize energy well completions and field development strategies. The Western Canada-WTI crude price differentials, lower spot prices, and competition from peers are keeping NCSM’s pricing down. Recent large contract awards are NCSM’s growth catalysts. With incremental advances in technology, the company’s products look to edge NCSM’s competitors when the energy environment becomes more favorable. In 2018 so far, the stock price has decreased by 65% and underperformed the VanEck Vectors Oil Services ETF (OIH), which declined by 46% during this period. OIH represents the oilfield equipment & services (OFS) industry.

NCSM’s Canada operations and outlook

In NCS Multistage’s Canadian operations, its revenue of $29.1 million for Q3 2018 was lower by 28% compared to the year ago. The decline resulted from adverse weather conditions, widening commodity price differentials between Western Canada crude oil and WTI, pricing pressure on NCSM’s offerings from its customers, and competition in some operating regions. In this context, let us discuss the crude price differentials in detail. The crude oil price spread has led to lower future cash flow expectations for its upstream customers, which caused contract renegotiation at lower prices or lower spot prices, causing NCSM’s margin to deteriorate. Competitions from NCSM’s peers were high in Saskatchewan and in the Cardium in Western Canada, which have light crude oil resources.

In Q3 2018, the prices for providing fracturing pumping services in Canada declined. Not only did the spot market pricing, which indicates the demand for short-run, decreased, but rates for some of the longer-term work in the Canadian basin also went down. Lack of infrastructure in comparison to the supply boost in many parts of North America, including Canada and the Permian Basin in Texas, caused the price to fall. Investors may note that Western Canada Select (WCS), which tracks heavy oil from Canada, typically trades at a discount relative to WTI. The lower price reflects quality issues, as well as the cost of transport from Alberta to refineries in the U.S. In November, Canadian producers were fetching above $30 per barrel less than their counterparts in the United States. Since early 2018, when the Canadian pipelines began to saturate, the discount started to grow significantly. The inability of the Canadian oil industry to build a major pipeline from Alberta to either the U.S. or the Pacific Ocean is increasingly dragging down WCS. Keystone XL, Northern Gateway, Energy East, Trans Mountain Expansion – all of these pipeline projects have run into long delays.

Over the long-term, however, NCSM’s management expects the completion of a Keystone XL or the TMS Expansion to resolve the crude oil takeaway capacity constraints. Plus, not all of the company’s customers are exposed to the current spot prices as many have been able to hedge their exposure or price their crude at hubs where differentials are not as extreme.

Seasonally, the first quarter is NCSM’s most active quarter for the year. This leads to anticipating higher activity from NCSM’s business from the upstream segment in Q1 2019. However, the upstream companies’ budget for FY2019 is likely to be set keeping in mind the crude oil differential trend and their profit potential. Given the increasing gap between the prices, the short-term outlook appears to be dimmer.

NCSM’s U.S. operations and outlook

In NCS Multistage’s U.S. operations, its revenue of $26.3 million for Q3 2018 was nearly double compared to a year ago. The drilling and exploration activities in the U.S. unconventional shales increased significantly in the past year. NCSM achieved its fourth consecutive quarter of sequential unit sales growth in sliding sleeves and composites frac plugs sales in Q3. In the past years, NCSM has increasingly sourced its revenues from the U.S. However, compared to Q2 2018, the U.S. revenues decreased by 5%. The sequential decline was primarily attributable to services provided during pinpoint completions and tracer diagnostics.

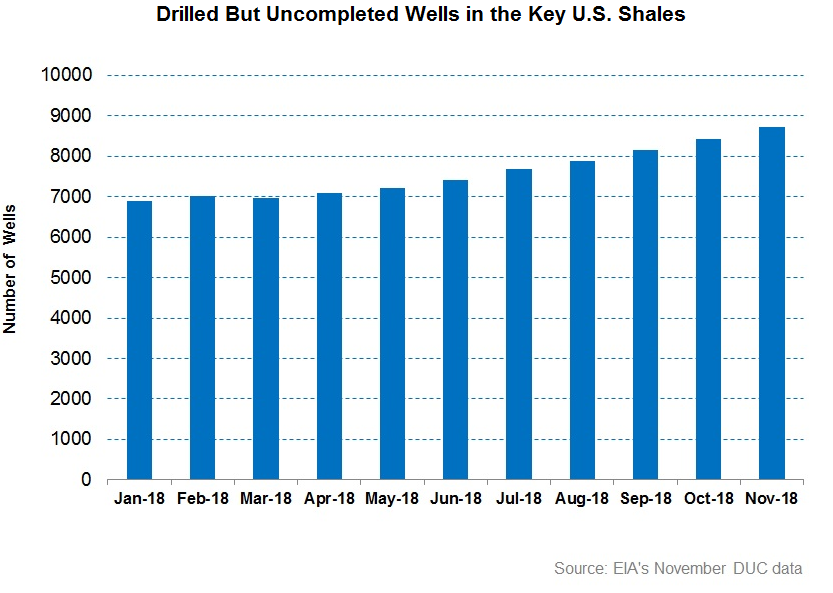

In the past couple of months, some of the key U.S. shales including the Permian in Texas were hit by capacity infrastructure constraints and a slowdown in well completions activity. Investors may note that drilled but uncompleted wells, or DUCs, represent wells that will likely be completed at some point in the future. Since the beginning of 2018, DUCs in the U.S. has increased by 26%, according to EIA’s estimates. This indicates a slowdown in well completions activity, which was fueled by a 33% fall in WTI crude oil price in the past year. NCSM’s premier solution pinpoint stimulation optimizes completion designs and increases well productivity. The completions activity headwind, if continued for a more extended period, can affect PFIE negatively. The revival of the DUCs is closely linked to the crude oil price’s recovery from the current depression. If the fall in price is short-lived, as expected by analysts, NCSM’s products will see higher demand in the medium-term.

How are NCSM’s premier product technologies advancing?

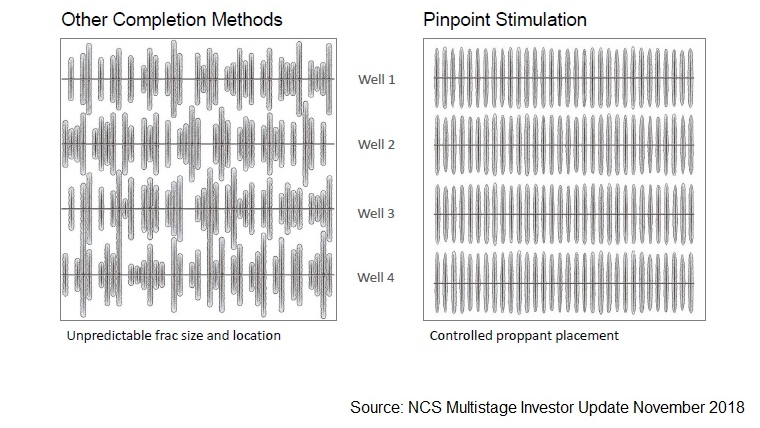

In this context, it is pertinent to discuss NCSM’s primary offerings including the pinpoint stimulation and tracer diagnostics. This trend towards more complex well completions has also resulted in increased use of tracer diagnostics services, which can be utilized to assess the effectiveness of various well completion techniques. Some of the wells where pinpoint stimulation techniques have been used involve a high number of stages in drilling. Typically, with rising lateral lengths in horizontal wells, more stages are required to ensure effective stimulation occurs. This widens the scope of pinpoint stimulation. In tracer diagnostics, NCSM commercialized its water-soluble tracer product offering in Q3. Also during the quarter, NCSM achieved the first commercial sales of the Purple Seal Express frac-plug deployment system.

However, upstream companies have the options of using NCSM’s pinpoint versus other OFS companies’ traditional plug-and-perf technology. NCSM’s biggest competitors offer plug-and-perf, which can be less costly in a certain situation and drilling methods. As hydraulic fracturing prices began to increase in the U.S., the total cost for NCSM’s pinpoint job has increased in some cases. As a result, the trend towards longer and more complex wells has resulted in selling more sliding sleeves or composite frac plugs per well on average.

As the headwinds in completions job continue, NCSM is looking increasingly towards its well construction tools. The management commented in the Q3 earnings call:

“So, we’ve had well construction products for a number of years. We developed the AirLock product line, we developed a liner hanger product line, we have the toe sleeves, but it hasn’t been a really big focus for us. So, over the last few months what we’ve done is, we have put together a well construction group in the company and we put additional focus on it, we’ve got dedicated sales support now and we are looking beyond just the U.S. markets.”

NCSM’s international market: In Q3 2018, NCSM generated 12% of its revenues from the global markets, which was significantly higher than the 4% share in Q2. The company delivered NCS products for an upcoming trial in the Middle East. This marks its first work in the Middle East. However, NCSM’s management estimates 4Q 2018 international revenue to be between $3 million and $4 million, which would be a 50% decline compared to Q3.

In August, NCSM signed a contract agreement with Aker BP – one of the largest oil and gas companies in Europe by revenues. The five-year deal pertains to well-stimulation services. Work under the contract is subject to individual purchase orders. Read more on the acquisition as well as a detailed analysis of NCSM here.

NCSM’s debt and cash flow

NCSM’s long-term debt increased on September 30, 2018, compared to what was at the beginning of the year. Earlier, in May 2017, NCSM issued a public offering and raised $149 million. It repaid a significant part of its long-term debt from the IPO proceeds. Its net debt was negative as of September 30 as a result of cash & equivalents exceeding total debt. NCSM’s negative net debt implies it has more cash than it owes, which is typically a sign of financial strength and stability.

NCSM has $20.4 million of long-term debt repayment scheduled in 2019-21. Free cash flow was negative in the past four quarters until Q3 2018. The company plans to incur ~$13 million-$16 million in capex in FY2018. It had cash and cash equivalents of $27.4 million. Plus, it has $55 million available as of September 30 under the revolving credit facility. With sufficient liquidity, meeting contractual obligations and the capex should not be difficult for NCSM in the short-term.

What does NCSM’s relative valuation say?

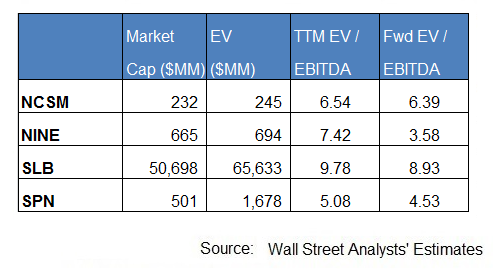

NCS Multistage Holdings is currently trading at an EV-to-adjusted EBITDA multiple of 6.5x. Based on sell-side analysts’ EBITDA estimates in the next four quarters, NCSM’s forward EV/EBITDA multiple is 6.4x. Between Q2 2017 and Q3 2018, the average EV/EBITDA multiple was 30.1x. So, NCSM is currently trading at a steep discount to its past seven-quarter average.

NCSM’s forward EV-to-EBITDA multiple contraction versus its adjusted trailing twelve-month EV/EBITDA is less steep than the industry peers’ average multiple compression. This is because I expect NCSM’s EBITDA to improve less steeply compared to the rise in the peers’ average in the next four quarters. This would typically reflect in a lower current EV/EBITDA multiple compared to the peers’ average. NCSM’s TTM EV/EBITDA multiple is lower than its peers’ (NINE, SLB, and SPN) average of 7.4x. For the table above, I have used sell-side analysts’ estimates provided by Thomson Reuters.

Analysts’ rating on NCSM

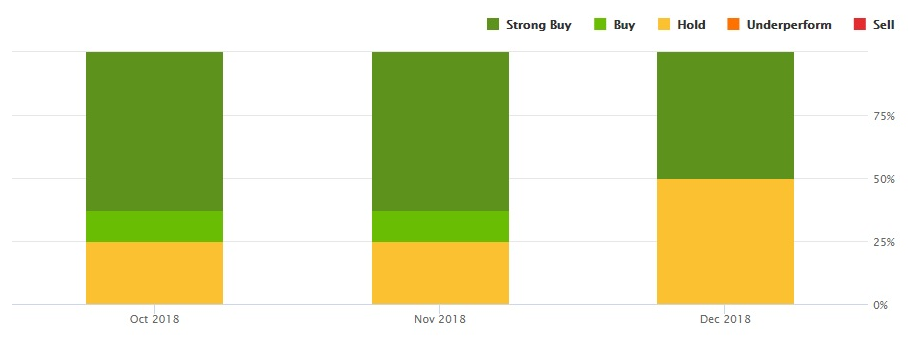

According to data provided by Seeking Alpha, four sell-side analysts rated NCSM a “buy” in December, while four recommended a “hold”. The analysts’ consensus target price for NCSM is $9.1, which at NCSM’s current price yields ~79% returns.

What’s the take on NCSM?

Canada, which continues to be a significant part of its portfolio, faces industry headwinds. The Western Canada-WTI crude price differentials continue to cause a lower profit margin for the Canadian oil producers, which adversely affects OFS companies’ growth potential. Plus, lower spot prices and stiff competition from peers offering alternative techniques are keeping NCSM’s pricing low. New and improved drilling techniques in the U.S. unconventional resource shales now drive NCSM. The Aker BP contract reached in August is also likely to boost NCSM. I don’t expect NCSM’s performance to swing upwards in the short-term. But its innovative product churn will gather higher price realization once the current negative drivers recede. That should drive NCSM higher in the medium- to long-term.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment