The iShares iBoxx $ Investment Grade Corp Bond ETF (LQD), which tracks US investment grade corporate bonds, is down by about 7.27% from its 52-week high. This has mainly been due to a hawkish Fed tightening credit conditions for the most part of this year. However, since Fed chairman Powell struck a more dovish tone on Nov. 28, the LQD ETF has rallied by about 1.26%. This article assesses why I believe investors should not buy into the rally at this point.

Source: Yahoo Finance

Prospectus Review:

The LQD ETF aims to track the investment results of the Markit iBoxx USD Liquid Investment Grade Index. The fund seeks to provide investors exposure to the highest- quality corporate bonds that are considered ‘investable’, allowing investors to earn higher yields in comparison to government bonds. It has an annual net expense ratio of 0.15%, which is lower than the 0.17% average net expense ratio of all the ETFs that offer exposure to corporate bonds, thereby making it comparatively cost-effective as an investment vehicle.

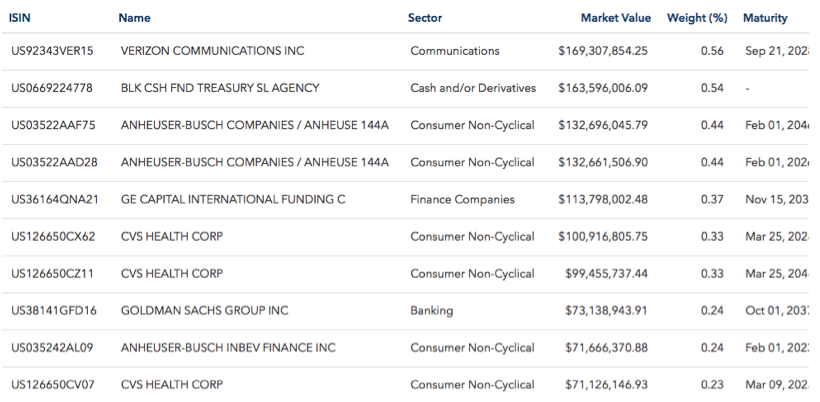

The top 10 holdings of the ETF includes:

Source: ishares.com

Source: ishares.com

Risk Note from LQD prospectus:

The Fund may be subject to tracking error, which is the divergence of the Fund’s performance from that of the Underlying Index. Tracking error may occur because of differences between the securities and other instruments held in the Fund’s portfolio and those included in the Underlying Index.

It is worth noting that the fund’s strategy involves only holding corporate bonds that have maturities of three years or more, its portfolio has an average maturity of 12.57 years. The fund’s preference for longer weighted bonds makes it more susceptible to interest rate risk.

The LQD ETF has the highest amount of Assets Under Management, at $30.48 billion, among its peers of corporate bond ETFs, according to data from ETFdb.com. This makes it one of the most highly traded and liquid ETFs, which is the main reason I have chosen this ETF, as liquidity is essential. Moreover, it has an average daily trading volume of 7.97 million, whereas the next two largest corporate bond ETFs, Vanguard Short-Term Corporate Bond ETF (VCSH) and Vanguard Intermediate-Term Corporate Bond ETF (VCIT), have an average volume of 1.47 million and 1.25 million respectively. The higher an ETF’s trading volume, the easier it is to buy and sell the ETF in the market. Thus, given my bearish thesis on this ETF, high liquidity is important for investors to be able to easily sell out of their positions.

Dovish Fed is highly anticipated

While the Fed is expected to raise rates on Dec. 19, markets are anticipating dovish statements from Fed chairman Powell in order to address the recent slowdown in the economy. Given that corporate yields are influenced by yields on government bonds, this dovish guidance is likely to lower yields on corporate bonds as well. Thereby easing pressures of tightening credit conditions, which would be a bullish factor for the LQD ETF.

However, I do not believe this rally will last in the face of persistently slowing economic growth, given that the 3 and 5-year section of the yield curve as inverted, and the spread between the 2-year and 10-year continues to narrow. While this latter section of the yield curve has not inverted yet, which would indicate an upcoming recession, I believe the extent of flattening at this section certainly indicates more economic weakness ahead at the very least. Markets perceive that economic growth had peaked in Q2 2018, and that the economy will remain on a downward trend. Moreover, the global economy is simultaneously also weakening as China, the second largest economy in the world, again reported weaker than expected economic data on Dec. 14. If US economic growth continues to move in tandem with the global economy, then corporate profitability will undoubtedly suffer.

In fact, the LQD ETF is currently more highly exposed to BBB-rated bonds, the poorest quality of investment grade bonds, than prior to the crisis. The current holding stands at 48.53%, whereas prior to this crisis it was only at 38%. If economic conditions worsen, rating agencies may downgrade corporate bonds, in which case yields could spike, and send the LQD ETF plunging.

Moreover, it is worthwhile noting that the LQD ETF currently has a 9.71% sector weighting towards the energy sector, making it the 4th largest sector weighting among all its holdings. Oil prices have already been plummeting this year, with WTI crude oil currently trading at $51.23 per barrel, putting stress on energy corporate bonds. If economies worldwide continue to slow, oil could decline even further, which would severely hurt the energy companies’ earnings potential, and certainly undermine their ability to repay loans. This would cause yields on their corporate bonds to spike, and given that the LQD ETF is nearly 10% exposed to this sector, it could put further downward pressure on the ETF.

Credit spreads widening

The current yield to maturity for the LQD ETF is at 3.89% Keep in mind that during times of uncertainty and recession worries, investors will move out of riskier corporate bonds and allocate capital towards safer US Treasuries. This higher demand for Treasuries would drive their yields much lower. On the other hand, the outflow of capital from corporate bonds would cause corporate bond yields to spike, thereby causing credit spreads to widen.

‘Credit spread’ is referred to as the spread between US government bonds and corporate bonds with similar maturities. When credit spreads widen, it is considered an indicator for a darker economic outlook ahead. My perspective is that as credit spreads continue to widen, at some point current market bulls will also be forced to reconsider their optimism on the US economy, which will aggravate the outflow from corporate bonds, resulting in the LQD ETF diving downwards.

Bottom Line

Even amid the Federal Reserve becoming more hawkish, the economic outlook continues to dampen. As the economy continues to weaken, corporate bond yields will move higher, inducing bond prices to drop lower. Widening credit spreads will definitely repel more and more investors from corporate bonds, which will drive the value of the LQD ETF lower. I do not recommend buying into the LQD ETF at present.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment