Hardware companies like Hewlett Packard Enterprise (HPE) are out of favor on Wall Street. Software is king and hardware is viewed as commodity-like. The resulting low valuation is interesting but not a sufficient reason to invest in HPE. You also need a catalyst to unlock the value. Dell’s upcoming IPO can be that catalyst.

Hardware out of favor

Hewlett Packard Enterprise was spun off from Hewlett Packard (HPQ) in 2015. HPE still has a weight of 7.5% in Invesco S&P Spin-Off ETF (CSD).

Hewlett Packard Enterprise’s enterprise-level servers, storage, and networking gear faces increasing pressure from Cisco Systems (CSCO) and Dell Technologies (DVMT). At the same time, HPE’s cloud-computing business competes with Amazon.com (AMZN), Microsoft (MSFT), and Salesforce.com (CRM).

IT Hardware is considered one of the sectors Amazon is/might be disrupting. Amazon represents an “existential threat” to the traditional enterprise IT hardware industry, according to Bernstein’s Toni Sacconaghi, as “IT organizations have begun to fundamentally change their thinking about tech spending, as companies increasingly eschew running their own datacenter hardware in favor of outsourcing most of this infrastructure to Amazon Web Services, Microsoft Azure, and Google Cloud Platform.”

In a Bernstein survey from June, CIOs reported that on average 20% of their organizations’ workloads were running in the cloud, a share that is only increasing. Amazon and other cloud providers have the scale and expertise to cut out traditional hardware players such as Dell, Oracle (ORCL), or Hewlett Packard Enterprise through the use of whitebox hardware and in-house support teams. According to Sacconaghi, at its current penetration, the cloud already represents at least a 4% headwind to traditional IT infrastructure spending growth, and will lead to negative growth as more organizations migrate functions to the cloud.

On the other hand, Michael Dell made the interesting comment that Dell has seen some customers that initially went to the cloud start repatriating back as they come to realize that the costs are “twice as much”. So, while cloud is having an impact on traditional infrastructure, it is not ideal for every workload.

Hewlett Packard Enterprise CEO Antonio Nero sees a future for a hybrid model: a combination of servers and cloud. HPE is well positioned for such a future. Dell is also betting on both horses: through its backdoor IPO it will own 81% in cloud specialist VMware (VMW).

When we look at the performance of hardware versus software and semiconductors, it’s clear that hardware isn’t outperforming.

Exhibit 1: Hardware underperformance

Source: Koyfin

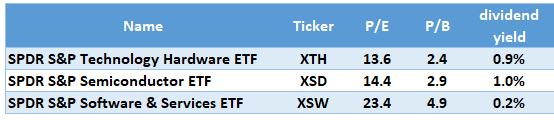

The fact that hardware companies are out of favor is also reflected in the valuation levels.

Exhibit 2: Hardware undervaluation

HPE isn’t Wall Street’s darling

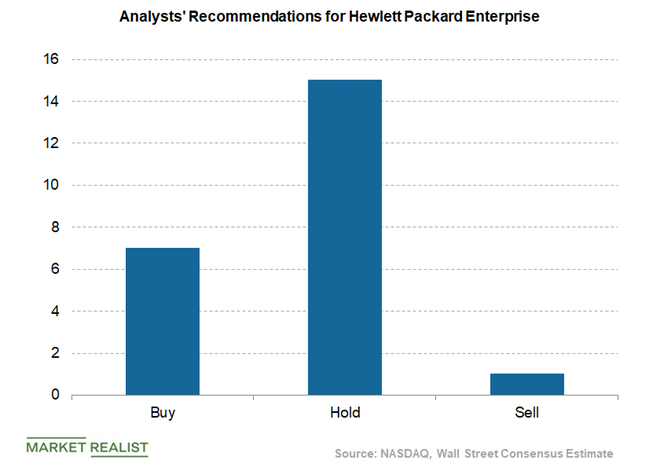

Of the 23 analysts covering Hewlett Packard Enterprise, only seven recommend “buy,” 15 recommend “hold,” and one has a “sell” rating.

Exhibit 3: Analyst Recommendations

Shareholder value

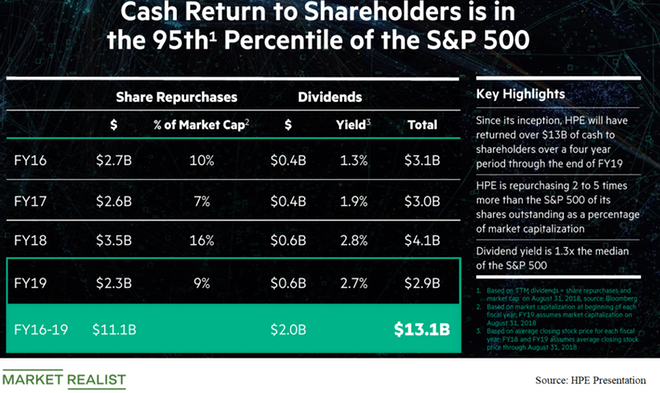

Hewlett Packard Enterprise has been consistently rewarding shareholders with cash dividends and share buyback programs. In fiscal 2018, the company returned $4.1 billion through repurchases and dividends to shareholders. It returned around $3 billion in fiscal 2017 and $3.1 billion in fiscal 2016 to shareholders.

In fiscal 2019, Hewlett Packard Enterprise expects to reward shareholders with $2.9 billion in dividends and share repurchases, bringing its total payout to $13 billion over four years.

In fiscal 2018, HPE’s dividend per share almost doubled to $0.4875 from $0.26 per share. HPE’s dividend yield is 3% and its annualized payout was $0.45, indicating a payout ratio of almost 30%.

Its capital return program puts Hewlett Packard Enterprise in the top 5% of companies in the S&P 500 in terms of cash returned to shareholders.

Exhibit 4: Shareholder value

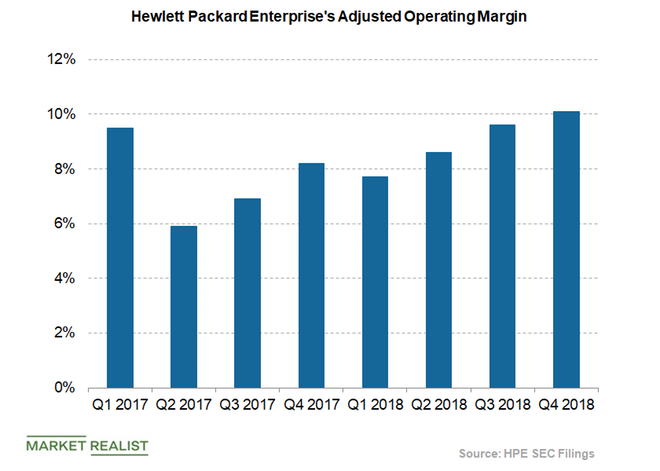

Earnings are up

Hewlett Packard Enterprise’s full year earnings were driven by growing demand for its storage and data center networking products, and its operating margin improved due to its cost saving measures.

Hewlett Packard Enterprise’s HPE Next initiative, launched during the third quarter of fiscal 2017, could help the company save approximately $1.5 billion over the next three years. HPE Next aims to simplify the company’s organizational structure and redesign business processes to improve margins.

The company is also making efforts to acquire and diversify into wider-margin businesses. For instance, HPE’s recent purchase of AI and analytics software maker BlueData Software could expand HPE’s margins further.

Exhibit 5: Operating margins

Besides cost savings through the HPE Next program, share repurchases will give a boost to HPE’s earnings in the future. HPE’s operating margin is expected to rise from 8.9% in fiscal 2018 to 9.4% in fiscal 2019 and 9.8% in fiscal 2020.

Dell IPO

As we said before, the hardware sector in general and HPE in particular are out of favor. HPE’s low valuation is tempting but not a sufficient reason to invest in HPE. You also need a catalyst to unlock the value. Dell’s coming IPO will put the spotlight on the hardware sector and this can be that catalyst. At the same time, Dell can act as a valuation anchor.

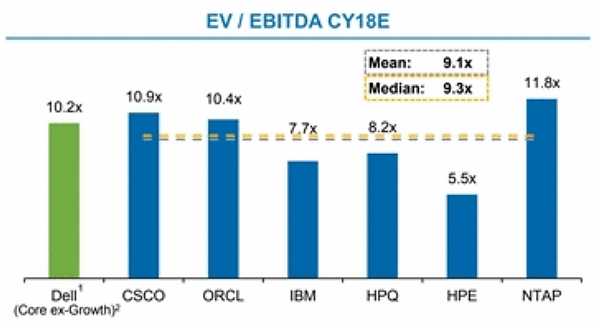

In a presentation Michael Dell put forward a very high valuation for Dell’s core activities (that are a peer for HPE’s activities).

Exhibit 6: Dell peer valuation

Michael Dell doesn’t of course take the Dell-discount into account. We see three reasons why Dell Technologies should carry a discount to its peers: conglomerate structure, heavy debt relative to peers, and poor corporate governance.

Those factors don’t apply to HPE and hence it would only be fair if HPE gets a higher valuation than Dell Technologies.

HPE’s operating margin is expected to rise from 8.9% in fiscal 2018 to 9.4% in fiscal 2019 and 9.8% in fiscal 2020. Peers like Cisco and IBM (IBM) have higher operating margins (at 31.7% and 18% respectively) and this warrants their higher valuation.

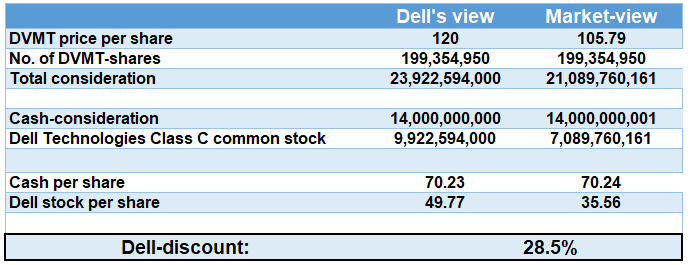

Of course, Michael Dell can come up with whatever valuation he wants, in the end, the market will decide. Based on Dell’s offer for DVMT shareholders, one can deduct an implied value for Dell Technologies shares. We show three examples: one based on the current DVMT share price, one based on Michael Dell’s view of the value of his offer, and one in-between.

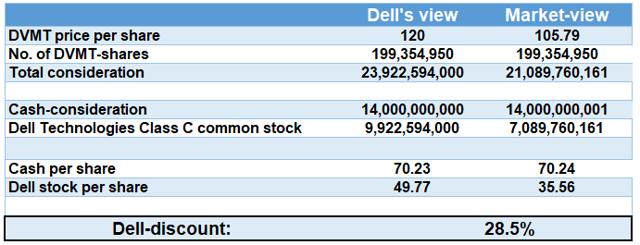

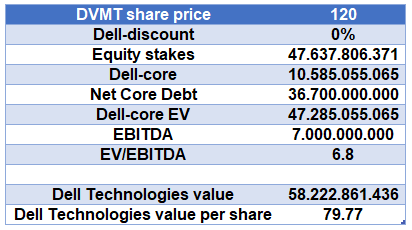

In his first offer to buyout DVMT shareholders, Dell put a value of $79.77 per share on Dell Technologies. In the final offer, DVMT holders are guaranteed an exchange ratio of 1.5043, which works out to the headline value of $120 per share if you believe Dell’s $79.77 valuation for its business. But DVMT share price has never reached $120. The market is applying a discount. Based on DVMT’s current market price, we calculate a Dell-discount of 28.5%! Instead of receiving a value of $49.77 in Dell shares, DVMT shareholders only receive only $35.56 (which equals a discount of 28.5%).

Exhibit 7: Dell-discount

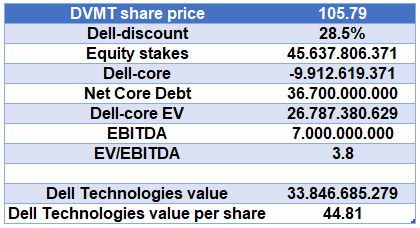

This leads to an equity value of $33.8 billion for Dell Technologies. This means the market attaches a negative equity value to Dell core and an enterprise value of 3.8 times EBITDA.

Exhibit 8: Dell valuation (in $)

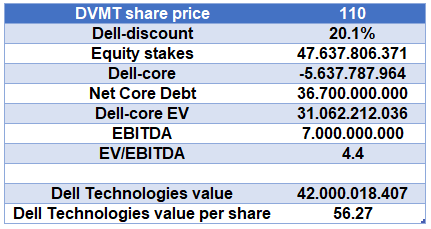

At a share price of $110 for DVMT, we get an equity value of $42.0 billion for Dell Technologies. This means the market attaches still a negative equity value to Dell core and an enterprise value of 4.4 times EBITDA, which is already more reasonable for a company with high debt and poor governance.

Exhibit 9: Dell valuation (in $)

We have put our fair value for Dell Technologies at $56.3 per share. This implies a conglomerate/governance discount of around 20% and an EV/EBITDA of 4.4 for Dell core, what is reasonable for a highly indebted company as (the core part of) Dell Technologies.

At a share price of $120 for DVMT (which implies no discount), we get an equity value of $58.2 billion for Dell Technologies. This means the market attaches an equity value to Dell core of $10.6 billion and an enterprise value of 6.8 times EBITDA, which is quite high for a company with high debt and poor governance.

Exhibit 10: Dell valuation (in $)

We can use this exercise as a basis for our HPE fair value calculation. There is no need to apply a discount to HPE for poor governance, conglomerate-structure or high indebtedness. On the other hand, a valuation as high as high-margin competitors like Cisco is also not reasonable. An EV/EBITDA around 7 seems fair.

We calculate a DCF fair value of $19.4 for HPE. This corresponds to a P/E of 12 (which is below the hardware-sector average P/E of 13.6) and to an EV/EBITDA of 6.5. This price target gives an upside potential of more than 35%.

The rosy scenario

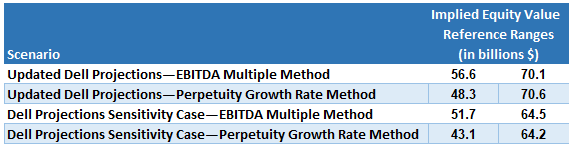

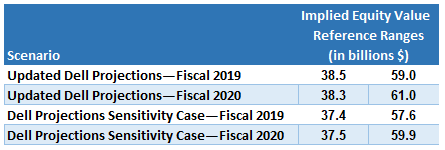

Things can of course always be crazier. Dell’s regulatory filings contain some very interesting peer valuations by Evercore (EVR) and Goldman Sachs (GS).

As a reminder, Dell’s view of a share price of $79.77 corresponds to an equity value of $58.2 billion for Dell Technologies.

Exhibit 11: Evercore Discounted Cash Flow Analysis

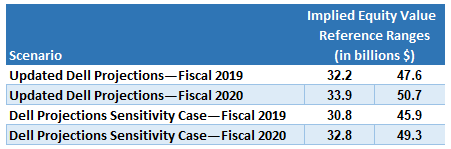

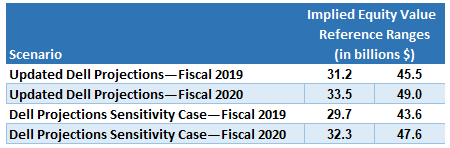

In performing a selected peer trading analysis of Dell Technologies, Evercore performed three different analyses:

- a sum-of-the-parts analysis,

- an analysis of Dell Technologies (excluding VMware) plus VMware, and

- an analysis of Dell Technologies on a consolidated basis.

Exhibit 12: sum-of-the-parts analysis

Exhibit 13: analysis of Dell Techn. (excluding VMware) plus VMware

Exhibit 14: analysis of Dell Technologies on a consolidated basis

The averages of all those valuations are ranging from $38.0 to $55.4 billion. This corresponds to an EV/EBITDA between 4 and 6.5 and remains below Dell’s valuation of $58.2 billion.

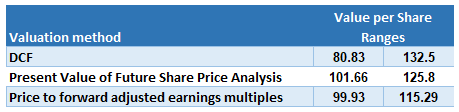

For the rosy view, we need Goldman Sachs. They performed an analysis based on different valuation methods. The results are displayed in exhibit 16.

Exhibit 15: Valuation by Goldman Sachs

This results in an average range of $94.1 to $124.5 per share for Dell Technologies. This corresponds to an EV/EBITDA between 8.1 and … 11.3!

If we apply this last multiple to Hewlett Packard Enterprise, we get a value of $38.4 per share for HPE.

Conclusion

Some people believe Amazon’s cloud services will annihilate the hardware-sector and take companies like HPE down. This pessimism is reflected in the current share prices of hardware companies. We follow Hewlett Packard Enterprise’s CEO Neri’s view that the future will be hybrid: both servers and the cloud will have their place under the sun. HPE is well-placed for such a future.

Hewlett Packard Enterprise ticks many boxes: margin expansion, earnings growth, creation of shareholder value and a low valuation to name a few.

Dell’s upcoming IPO and the fuss it will create can be the catalyst to unlock Hewlett Packard Enterprise’s value. BUY!

Disclaimer: This article provides opinions and information, but does not contain recommendations or personal investment advice to any specific person for any particular purpose. The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment