Apple (AAPL) beat expectations for the top and bottom line but Wall Street was unhappy with the low Holiday forecast so the valuation fell below a trillion dollars. The disappointment is understandable but unrealistic. Every additional dollar of revenue produces 30 cents of net income. Apple has to be very conservative on revenue. Even the lower bound of revenue guidance produces a 50% net income gain. If Apple just meets guidance, it will be because of supply chain problems or unanticipated demand shortfalls. It is a buy.

The Holiday Revenue

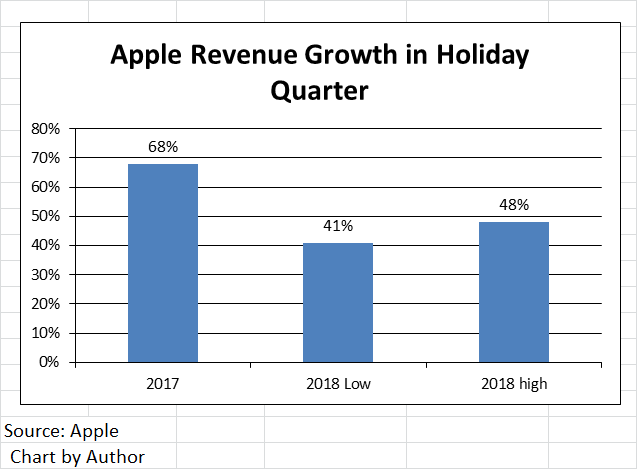

The key issue is the quarterly growth for the fourth quarter of fiscal 2018 to the first quarter of 2019 ending on December 31. As the chart below indicates, last year the holiday quarter’s sales grew 68% over the prior quarter. Apple is projecting growth of 41% to 48% -lower by 27 to 20 percentage points. Wall Street is right to be disappointed.

The iPhone is bigger than ever at 66% of sales. It grew 24% in revenue this quarter on a 14% increase in units, based on the success of the premium XS. The XR, which is $250 less, was only on sale for 5 days in the quarter. The reviews are excellent. They say the product performs very much like the XS and that it is a great value. The new iPad and Mac Air were also newly introduced with good reviews. It is likely that sales of these products will do well in the holiday season.

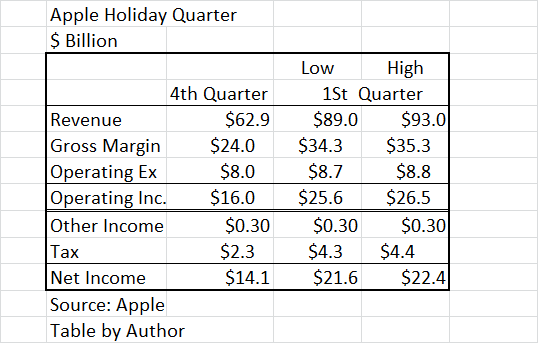

What is Apple’s rational for a lower forecast? Foreign exchange is unfavorable which will reduce the revenue from sales outside the U.S. A more serious problem is what Apple euphemistically calls the “supply demand balance”, in other words, a shortage of product for the holidays. It is better to have more demand than can be delivered, but in the holidays, some deferred demand will be lost. With newly introduced products, production schedules are subject to delays. It is likely that Apple can exceed the upper bound of $93 billion with some shortages.

Income Projection

The real reason for conservatism on revenue is that if last year’s 68% growth were used, the Net Income guidance would be way off if the revenue were missed. Every extra dollar of revenue in the quarter produces 30 cents of Net Income. No CFO will stick his neck out on that kind of projection, particularly one that depends on sales between Thanksgiving and Christmas. The disappointing revenue growth produces 50% net income growth at the lowest level. This is illustrated on the following chart.

Product Strategy

It is inevitable that competitors will add more expensive features to their premium phones. Apple is promoting the advantages of its own design of the biometric 7mm chip with AI capabilities to set it apart from competitors. Competitors now have more cameras and other features. To further set it apart, Apple links it to an expanding network of services like Apple Pay, Apple Music and the Aps from the Aps store. Revenue from Apple Services exceeded $10 billion in the quarter. Apple’s determination to keep customer data private has helped it expand in both hardware and services like Apple home and Apple TV.

Apple is increasingly tied to the iPhone despite an extensive expansion of other products. The latest Apple watch received good reviews. It is not clear if the new iPad, Macs, Apple home and Apple TV will take more share of revenue from the iPhone. However, they are premium highly profitable products.

Reporting Data

Apple further irritated the analysts by announcing that they will no longer report unit sales. They state the units are no longer a good indicator and they will now provide revenue and cost of sales for both hardware and software. The analysts pointed out that without the unit data, investors would suspect that Apple would be making deals that discount the products. The analysts are correct. Apple will discount the products. It is good to do that without it becoming an issue with the investors. Transparency can be overrated.

Conclusions

Apple is spending $14 billion per year on Research and Development. It is more productive because of the web of connected services that build product uniqueness. The phone operating system is a valuable asset to develop new mobile products. The analyst consensus forecast calls for slower growth as the iPhone becomes more mature. The link with services means that more opportunities are created. The emergence of fifth generation makes this even more relevant. That is why it is a buy.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment