The slow decline of Kraft Heinz’s (KHC) stock since mid-summer 2017 has crushed investors in the food conglomerate. The stock has been searching for direction, but continues to slowly drip lower. When the name first fell to $60, we cited it as a value watch name over at BAD BEAT Investing, especially if it were to fall well below this level. Here we are. The stock has now fallen well below this level and looking to breach the $50 level. This is a level we feel compelled to be buyers at, even in light of the issues facing many food conglomerates. The yield is high and the company is taking steps to raise some cash. While the name has still faced more pressure since we said the stock would be in our thoughts and prayers, we believe value investors should consider initiating a position here and get paid to wait for the turnaround. We will investigate Kraft Heinz’s performance and where we see the name heading in 2019. Let us discuss.

Revenues growth resumes, minimally

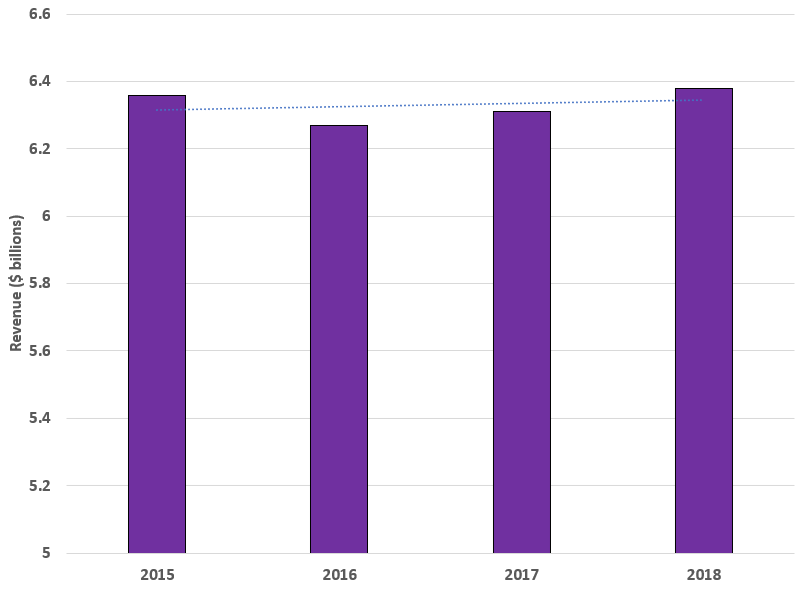

There is no doubt that sales have suffered in recent years. Sales do remain strong, but they had begun to flatten out and contract in some recent quarters. In the just reported quarter, there was demonstrated growth. Take a look at the last few Q3s:

Source: SEC filings, graphics by BAD BEAT Investing

Revenues have been pressured in recent years thanks to inflation, severe competition, and weakness in some key brands. There are still, however, some key positives to be aware of. First, we need to realize that Kraft Heinz’s sales have stabilized. Not only have they stabilized, they have also begun to rise again. This inflection is welcomed.

Keep in mind we have a stock that has fallen over 45 points since this immense sales pressure began. That is an incredible decline. We believe the negativity is more than priced in. The fact that revenues have stabilized and have begun inflecting higher is positive. Revenues grew 1.6% from last year, coming in at $6.38 billion.

Now, the one key item we like to look at is organic sales. Organic sales are natural sales growth of existing brands (as compared to inorganic growth, stemming from takeovers/mergers, etc.). Organic growth gives us a sense of the overall health of the company and its product portfolio. Organic growth has been severely pressured in recent quarters. Here in Q3, organic net sales jumped 2.6% versus the year-ago period. This is a strong result, especially when we consider what we have seen over the last 4 to 6 quarters.

How did the company achieve this organic growth? Here is where we see something very positive, and one reason we are starting to buy, with the thought that turnaround may be beginning. The organic growth was not a result of price increases. Pricing was actually down 0.9 percentage points as heavy promos in the United States dragged this figure down. Prices were higher internationally, primarily from highly inflationary environments. But the real strength was seen in volume/mix. Volume/mix increased 3.5 percentage points overall. This is a stellar figure. Further, there was growth in every segment.

Regionally, United States net sales were $4.4 billion, rising 1.8% versus the year-ago period. Pricing was down big. It fell 2.0 points, but volume/mix jumped 3.8 points driven by high consumption of most of the portfolio brands. Canada’s net sales were $525 million, 5.6% lower than last year, reflecting a 3.7-point impact from currency and a 1.4%-decline in organic net sales. Pricing was down 1.5 points, while volume/mix was flat. While flat volumes seem negative, it reversed a recent trend of declining volumes. Much of this was from promotional activity. Over in EMEA net sales were down 3.3% versus the year-ago period in part due to divestitures, but organic net sales increased 0.6% versus the year-ago period. Pricing declined 0.7 points while volume/mix increased 1.3 points. Finally, the ‘Rest of World’ segment net sales saw great growth. These sales came in at $793 million, increasing 9.9% versus the year-ago period. Organic net sales here were up 12.5% versus the year-ago period. Pricing was up 6.2 points while volume/mix increased 6.3 points.

We believe these results are mostly positive. However, we do have to caution that this came at a cost. In order to see these increases, promotional activity was heavy and this led to a hit in margins, as well as earnings. Still, we see the steps being taken to boost sales and fight for market share as positives.

Expenses take a bite out of margins

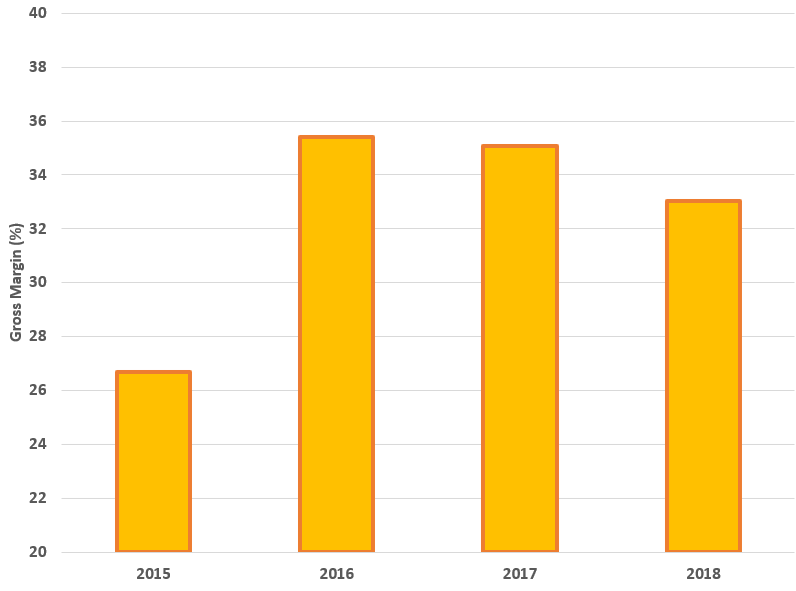

One notable weakness which has impacted earnings power with the relatively flat revenues is the rising cost of sales, which has led to compressed margins:

Source: SEC filings, graphics by BAD BEAT Investing

Source: SEC filings, graphics by BAD BEAT Investing

As you can see, margins narrowed to 33.0%, down from 36.6% last year. In the sequential Q2, margins were 35.3%, so we saw a major quarter-over-quarter decline as well. This trend is explained by the promotional activity that was necessary to jump-start organic sales. This was disappointing, as we want to see margins return to the high 30% range, and the decline was more than expected. However, the company took the long view of winning back customers rather than raising prices everywhere, which we believe could alienate its customers in this heavy competition environment. Moving forward, we encourage the company to focus more on its input costs, but we are cognizant of the fact that inflation is really having a negative impact on ingredients and other costs.

Earnings pressured thanks to margin compression

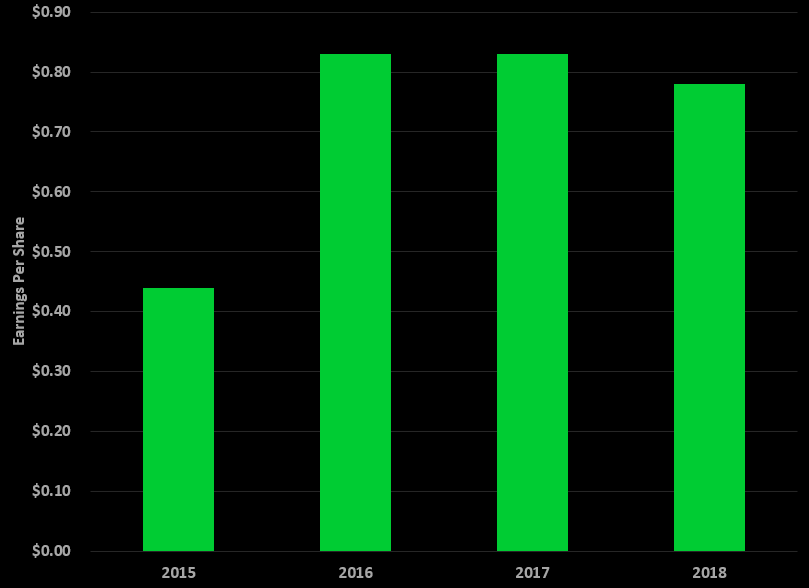

Earnings were below our expectation for $0.80, mostly on the back of higher-than-expected expenses which hit margins. Unfortunately, the trend for earnings in Q4 over the last three years is now negative:

Source: SEC filings, graphics by BAD BEAT Investing

We were expecting earnings per share to come in at $0.80 which would still have been slightly down from last year, given we expected slightly lower margins. However, the decline to 33.0% margins caught us by surprise and as such earnings per share fell to $0.78. While seeing this earnings decline is definitely painful, we caution would-be investors to realize shares are down almost 50% in just over a year. In other words, pain was more than priced in. We believe that even based on stagnant performance, with the current yield, shares are a buy for income while we wait for a turnaround in the company.

As we move into 2019

As 2018 comes to a close and we prepare to enter calendar 2019, we have some thoughts to keep in mind and some projections. As far as the stock goes, pick your spots to add. Wait for sizable dips. Do not buy all at once. Build a position. It should take time. Operationally, despite pressure on organic sales in 2018, we believe the company is ending the year on a high note by pumping promos to win back customers even at the temporary expense of margins. We continue to see value in the name. Patience is advised. The company this year is making significant improvements in many of its businesses, and accelerated needed investments internationally.

With one quarter to go, we have better clarity on earnings. Factoring in the reduced 2018 tax rate, roughly flat sales, and margins around 34-35%, we project adjusted earnings per share of $3.60 to $3.65. Thus, on a forward basis, shares are trading at 14.2 times 2018 earnings at the present $32 per share. This is most reduced the valuation has been in years. We also want to point out that we fully expect earnings per share growth in 2019, and preliminary are eyeing very low single-digit sales growth and average margins of 35%. This comes even with the name taking steps to raise some cash through a sale of its Canadian natural cheese business for $1.3 billion. While we will wait to see guidance on promotional spending, this is what we see as likely. Considering these metrics pan out, we are looking for earnings per share in 2019 of $3.70-3.90.

Overall, the entire sector has been under pressure. What we are seeing with KHC we have seen with many competitors. The name is also high-yield now, as it will serve well in a choppy and volatile market. We believe time is on your side and presently the dividend is safe. We like this name at a $50 handle. While currently paying you 4.7%, we encourage our readers and shareholders to add selectively to holdings.

Quad 7 Capital has been a leading contributor with Seeking Alpha since early 2012. If you like the material and want to see more, scroll to the top of the article and hit “Follow.” Quad 7 Capital also writes a lot of “breaking” articles, which are time-sensitive, actionable investing ideas. If you would like to be among the first to be updated, be sure to check the box for “Get email alerts “under “Follow.”

Just two spots left. Our half-off annual discount is back for a select few: Join a community of traders now

Our 53% annual discount period is back for the next two subs. Get our highest conviction rapid-return trade ideas for ~$1 a day.

What we do for you:

Find beaten-down stocks and profit from their reversals.

Defensive strategies in this turbulent market discussed in chat.

2-3 trade ideas a week, occasional deep value plays.

Guided entry and exits.

Open discussions of ideas with other day-traders and DEEP value investors.

Invest in your future by joining BAD BEAT Investing today.

Disclosure: I am/we are long KHC.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment