Kohl’s (KSS) has got to be a strong contender for the title of best-performing and most unjustly penalized retailer in 3Q18.

Riding the undesired wave of pessimism that has been plaguing the retail sector (XRT) in November, the Wisconsin-based company delivered a classic “beat-and-raise” this Tuesday that should have thrilled investors ahead of the holiday season. Instead, shares took a 9% post-earnings plunge, although they had recovered about a fourth of this week’s losses by the end of Wednesday’s trading session.

(Image Credit: Supermarket News)

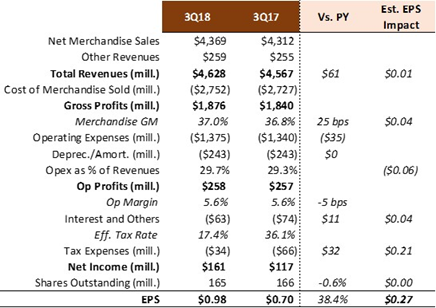

Calendar-adjusted comps reached an encouraging +2.5%, decisively leaving behind the early 2017 period of declining same-store sales and accelerating the YTD growth pace. Last quarter, I indicated that broad-based strength across the product line was a good indication that its house had been put in order. Kohl’s once again reported growth in the entire apparel business, with accessories staying flat. All accounted for, net merchandise revenues of $4.37 billion grew 1.3% YOY, topping consensus by one of the widest margins since 2014 at least: $260 million.

I believe the best thing about Kohl’s results came further down the P&L. Retailers have been experiencing a mixed bag of margin variance this earnings season. Macy’s (M), for example, saw gross margin rise 37 bps earlier in November as it continued to improve its merchandise inventory position; while Target (TGT) reported this week a discouraging 93 bp GM decline, driven by increased freight- and inventory-related expenses.

Kohl’s sided with the winners this quarter, delivering a quarter-point improvement in gross margin of 37%. This is not surprising to me, as I have been observing what seem to be superior asset management practices reflected in leaner merchandise inventories (see the generally improving five-year trend below). Within the peer group, Kohl’s had one of the best revenue-to-inventory per square foot ratios in the industry in the most recent year, second only to Nordstrom (JWN).

KSS Inventories (Quarterly) data by YCharts

KSS Inventories (Quarterly) data by YCharts

Very unusual in the retail space nowadays, the retailer managed to keep op margin largely flat YOY at 5.6%. With wages under pressure and revenues rising but only slowly, it is understandable that opex would increase on a percentage of sales basis: up 37 bps to 29.7%. Still, should Kohl’s manage to carry forward October’s comp momentum (the best month in 3Q18, according to management), we may start to see some operating leverage play out in the company’s favor in the holiday season.

See the summarized P&L below:

(Source: D.M. Martins Research, using data from company reports)

On the stock

Kohl’s fundamentals are not necessarily perfect, maybe not even best-in-sector. Top line growth has recovered, but remains timid at low-single digits levels. The company’s balance sheet has been improving, but still carries a net debt load of nearly 10% of total assets (trending positively).

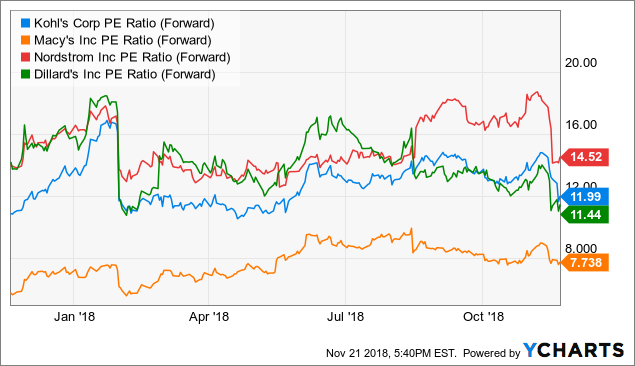

Yet, I believe the retailer is at least “good enough” to deserve a bit more love from investors. The stock is down 12% in November, and is now priced at early March 2018 levels. On a P/E basis (see below), a multiple of 12.0x is about as low as it has been in the past 12 months.

Potential investors looking for a combination of decent price for decent quality (a.k.a. “good value”) might want to spend some time looking closer into this name.

KSS PE Ratio (Forward) data by YCharts

KSS PE Ratio (Forward) data by YCharts

Note from the author: If you have enjoyed this article, follow me by clicking the orange “Follow” button next to the header, making sure that the “Get email alerts” box remains checked. And to dig deeper into how I have built a risk-diversified portfolio designed and back-tested to generate market-like returns with lower risk, join my Storm-Resistant Growth group. Take advantage of the 14-day free trial, read all the content written to date and get immediate access to the community.

Disclosure: I am/we are long M.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment