Bayer just recently announced its third quarter earnings results, which may at first glance disappoint investors as the net income decreased, especially after the acquisition of Monsanto. However, a careful look at the company’s financial performance reveals that this is not really the case, and the company has favourable conditions to improve its earnings in the future. Overall, the company remains in a position to deliver solid growth going forward, especially with the growth of market for seeds and genetics just acquired from Monsanto.

Q3 2018 key results

In the third quarter this year, Bayer’s sales increased by 23.4% (Fx & portfolio adj.) to more than €9.9 billion, with main contribution from Pharmaceuticals and Crop Science. Pharmaceuticals remains to be the highest revenue-generating business with sales increased by 4.8% and accounted for more than 42% of total sales. However, the main driver for the growth in this quarter was Crop Science, with sales rose substantially by more than 83%. This reflects the incremental benefit from the acquisition of Monsanto. With this result, Crop Science significantly improved its relative importance, as sales from Crop Science now equals around 90% sales from Pharmaceuticals, compared to only 50% in previous periods.

One thing to note here is that Monsanto’s sales are always considerably higher for the 6-month period starting December than the other period starting June. Looking at past figures, we notice that revenue in the former period is around 3.5 times higher than that in the latter. For example, in 2017, this data was $9.2B vs $2.6B, respectively. Thus, we conclude that Bayer Q3 results do not fully reflect the potential growth it could have from the newly acquisition, as it was in the period of lower sales. Hence, we expect Monsanto to contribute roughly €8-9 billion in sales for Bayer for the first six months of 2019, representing a y-o-y growth of around 177%-200% in the Crop Science segment.

Even though EBIT increased by 218%, net income from continuing and discontinued operation showed a reduction of around one-fourth. However, this was not due to low performance. Instead, the decline in the bottom line was mainly due to higher expenses that Bayer incurred in this period: with the acquisition of Monsanto, Bayer has to pay related costs totaling more than €700M. Besides, it also has to increase the number of employees, causing personnel expenses to increase by 21%. The most important thing to note is that the company did not include the €3.9 billion gain from the divestments to BASF, while the contribution of Covestro was no longer included. This results in €0 from discontinued operations, compared to more than €3000M in prior year period, which was the primary reason we see such a decrease in net income. As a result, earnings per share were also down and stood at €2.94. Again, it was the financing costs that stood against the earnings contribution from the acquired business that was lower due to seasonal reasons.

(Source: Bayer Q3 report)

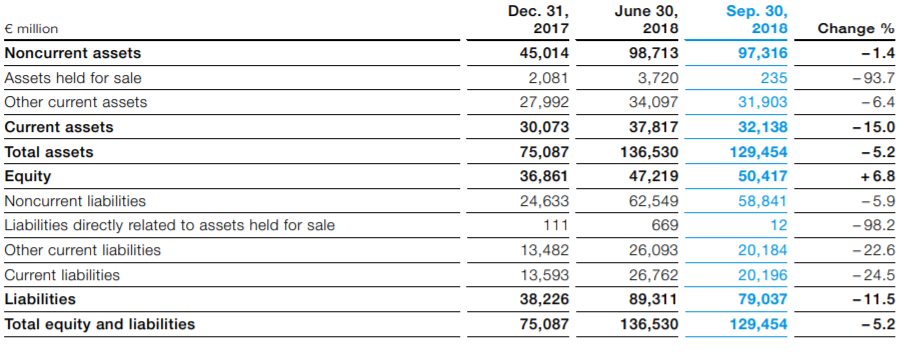

At this period, total assets fell by 5.2%, mainly due to the €3.5 billion decrease in assets held for sale regarding the divestment to BASF. Also from this divestment, Bayer received the proceed of €3.9 billion, which was used to repay the bridge financing for the Monsanto acquisition. As a result, liabilities were reduced by €10.3 billion, and net financial debt also declined by more than €8 billion (-18.3%).

(Source: Bayer Q3 report)

Seeds and genomics – the future value driver for Bayer

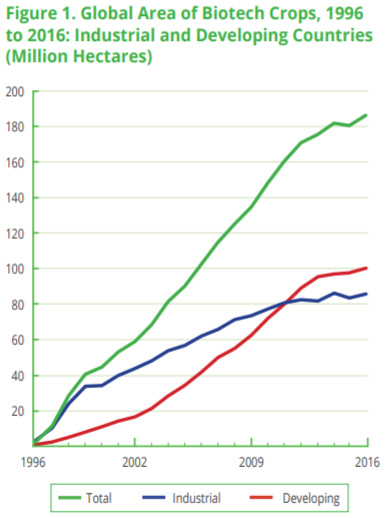

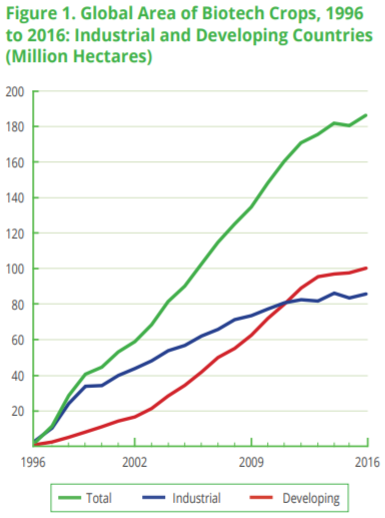

After acquiring Monsanto, Bayer has become the global biggest seed and genomics producer, opening up huge opportunities for the company. looking at past figures, we can see that genetic seed has becoming more and more important in the agriculture industry. According to ISAAA report, global area of biotech/genetic crops has been increasing steadily from 1996, with average growth rate of 5%. This rate is expected to be even larger in the future as production required for world food demand is expected to increase by 70% by 2050.

(Source: ISAAA report)

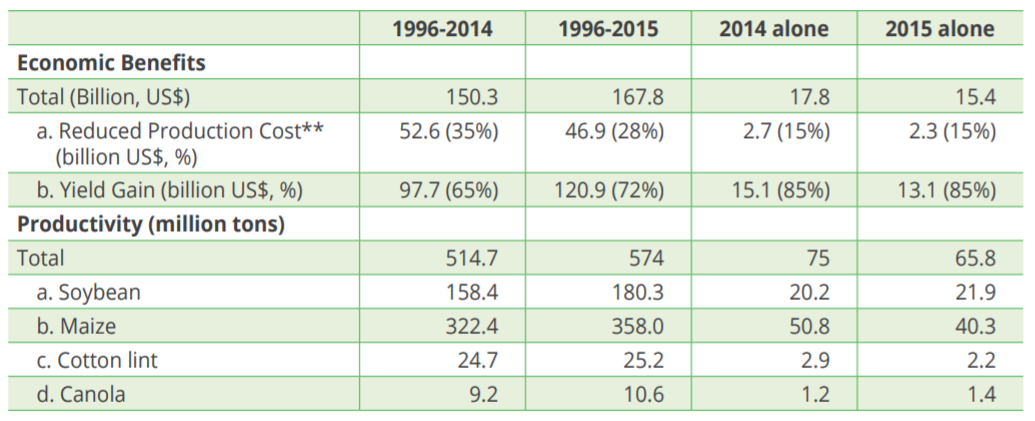

Also from the analysis of ISAAA, genetic crops have a lot of advantage over traditional farming. Firstly, it helps to reduce production cost by an average of 28% and increase yield gains by 72%. As a result, productivity increased by 574 million tons and economic gain of smallholder farmers rose by $167.8 billion. The following table would give a better look on the benefits from genetic crops:

(Source: ISAAA report)

Biotech crops are also more effective as they help plants to sustain harsh conditions caused by climate changes such as drought, submergence and high temperatures. Not only is genetic crop beneficial for farmers and plants but it is also friendly to the environment, which is a raising concern nowadays. Statistical analysis shows that biotech crops play an important role in mitigating climate change by reducing a significant amount of CO2. Moreover, it has also been proved to be safe for humans.

Thanks to all the favorable reasons above, genetic crop (or biotechnology) has been the fastest agricultural technology adopted by farmers in the last two decades. From only 6 countries adopting biotech crops in 1996, the number has increased to 30 countries in 2016. It is expected that biotech crops will be adopted by more countries in the future, which will expand the market size and strengthen the demand for seed and genomics – a condition that Bayer would take a lot of advantages from.

Looking at the financial performance of Monsanto, we see that more than 2/3 of total revenues come from seeds and genomics. Particularly, in 2017, the sales of this segment were $10.9 billion, accounting for around 75% of total sales. With the increased important of genetic crops, we expect this sales would be at least roughly the same for the next year. It means that the acquisition of Monsanto is likely to generate a comparable amount of around €9 billion (only for the seeds and genomics segment) for Bayer next years forward.

Risk

Perhaps Bayer’s biggest downside risk in this period is related to the case of glyphosate Roudup weed-killer. In our previous article, we have informed readers of a new trial court to reverse the $289M penalty verdict decided earlier. The result of the review trial was that the punitive damages were reduced from $250 million to approximately US$39 million, but the compensatory damages (around $39 million) remained unchanged. This was not the result that Bayer expected and it seeks another trials in February 2019. In the worst-case scenario, if Bayer was unable to prove the safety of glyphosate, it will have to face with more than 9300 other cases, which would cause billions in penalties or it may even be forced to discontinue the operation of this segment. This would of course be harmful to the company’s earnings, resulting in a decline of its stock price.

Conclusion

Even though Bayer is now facing a large downside risk, we would want to emphasize that the major source of revenue for Monsanto does not come from agriculture activity but from seeds and genomics. As this segment has a very potential outlook for the future, Bayer is very likely to gain benefits from the acquisition of Monsanto. Due to seasonal reasons, the increase in revenue for the third quarter could not offset the increase in expenses, causing net income to decline. However, for the next years onward, especially for the first six months, sales revenue of the Crop Science segment would increase significantly. Therefore, investors could be confident about the company’s future performance, even if glyphosate does not receive the most favourable result.

Disclosure: I am/we are long BAYZF, BAYRY.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment