Quick Take

YETI Holdings (YETI) intends to raise gross proceeds of $400 million from a U.S. IPO, according to an S-1 registration statement.

The firm designs, manufactures and sells portable coolers and related gear to outdoor enthusiasts worldwide.

YETI has a recently uneven operating history, will receive very little of the IPO proceeds, and is facing an uncertain and potentially higher materials cost environment.

Company & Technology

Austin, Texas-based YETI was founded in 2006 to make the active lifestyle more enjoyable by designing and marketing innovative outdoor products.

Management is headed by President and CEO Matthew J. Reintjes, who has been with the firm since 2015 was previously Vice President of the Outdoor Products reporting segment at Vista Outdoor.

Below is a brief promotional video about YETI products:

(Source: YETI)

YETI manufactures durable coolers that are suitable for camping, boating, and many other outdoor activities.

The firm’s product lines are as follows:

- Coolers & Equipment

- Drinkware

- Other

Customer Acquisition

YETI markets their products through an omnichannel strategy, comprised of a select group of national and independent retail partners and a direct-to-consumer and corporate sales, or DTC, channel.

The company’s DTC channel is comprised of YETI.com, YETIcustomshop.com, YETI Authorized on the Amazon Marketplace, corporate sales, and its flagship store located in Austin, Texas.

Sales and marketing expenses as a percentage of revenue have been dropping, as the table below indicates:

|

Sales & Marketing Expenses vs. Revenue |

|

|

Period |

Percentage |

|

1H 2018 |

35.5% |

|

2017 |

36.1% |

|

2016 |

39.8% |

(Source: Company Prospectus and IPO Edge)

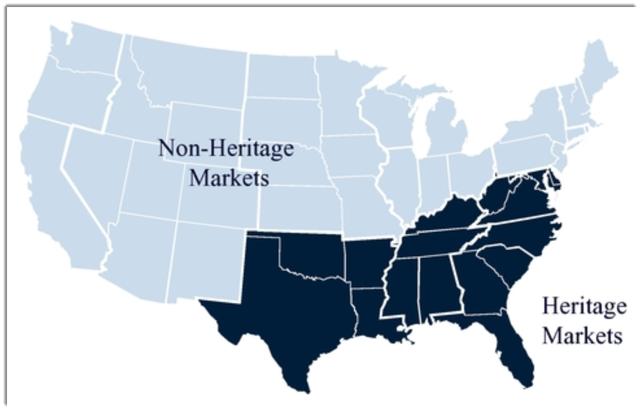

YETI management divides its current U.S. market penetration into ‘Heritage’ and ‘Non-Heritage’ markets, as shown below:

Going forward, the firm believes that much of its sales growth will be driven by growing its brand awareness in ‘Non-Heritage’ market areas in the US.

Market & Competition

According to a 2018 market research report by Technavio, the global portable coolers market is projected to grow at a CAGR of 13.4% during the period between 2018 and 2022.

The main factor driving market growth is the need to preserve food provisions and chilled food products from perishing.

Major competitors that provide coolers include:

- Bison Coolers

- Igloo Products

- Newell Brands (NWL)

- Grizzly Coolers

- ORCA Coolers

Financial Performance

YETI’s recent financial results can be summarized as follows:

- Uneven topline net sales growth

- Uneven gross profit

- Relatively stable gross margin

- Strong growth in cash flow from operations, but moderating in 1H 2018

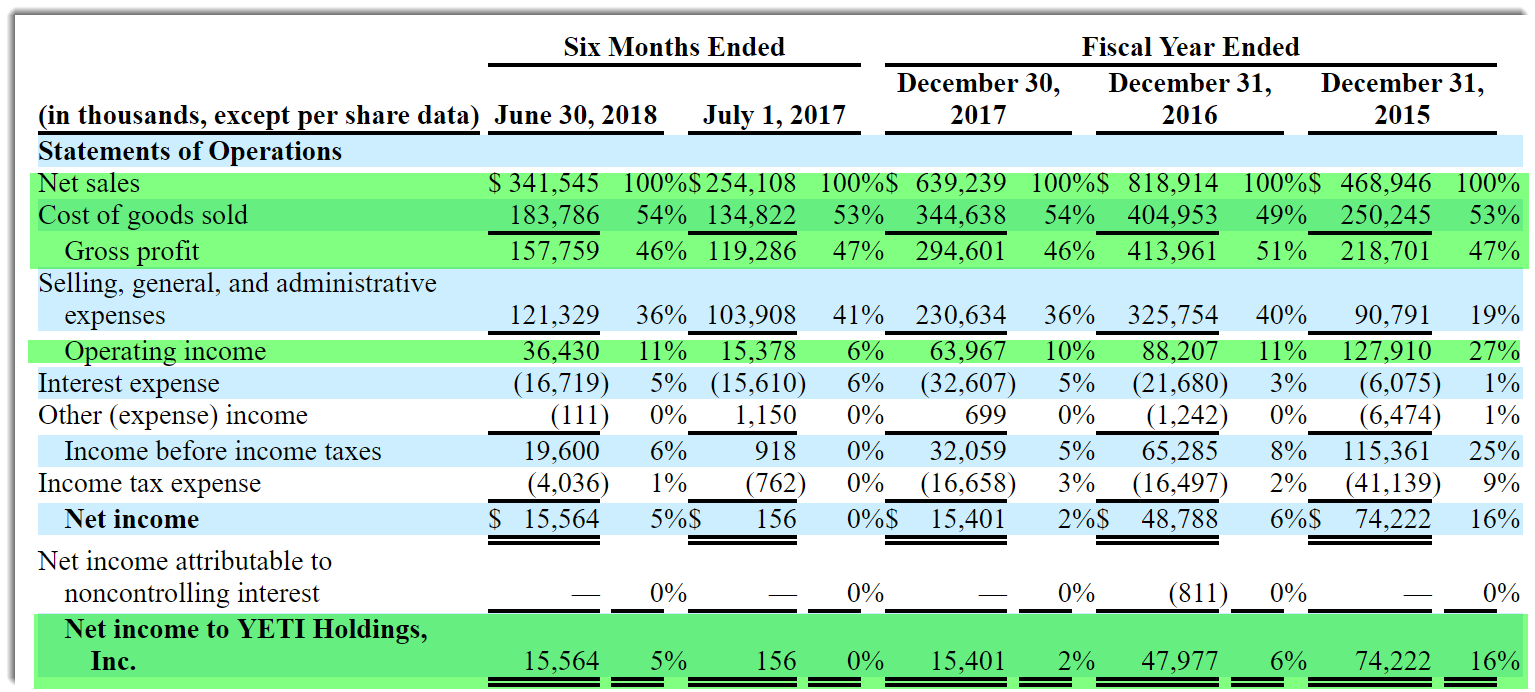

Below are the company’s financial results for the past three and ½ years (Audited PCAOB for full years):

(Source: YETI S-1/A)

(Source: YETI S-1/A)

Net Sales

- Through Q2 2018: $341.5 million, 34.4% increase vs. prior

- 2017: $639.2 million, 21.9% decrease vs. prior

- 2016: $818.9 million, 74.8% increase vs. prior

- 2015: $468.9 million

Gross Profit

- Through Q2 2018: $157.8 million

- 2017: $294.6 million

- 2016: $414.0 million

- 2015: $218.7 million

Gross Margin

- Through Q2 2018: 46%

- 2017: 46%

- 2016: 51%

- 2015: 47%

Cash Flow from Operations

- Through Q2 2018: $83.6 million

- 2017: $147.8 million

- 2016: $28.9 million

- 2015: $8.6 million

As of June 30, 2018, the company had $71.3 million in cash and $567.2 million in total liabilities. (Unaudited, interim)

Free cash flow during the six months ended June 30, 2018, was $76.6 million.

IPO Details

YETI intends to sell 2.5 million shares and selling shareholders will sell 17.5 million shares of common stock at a proposed midpoint price of $20.00 per share, for gross proceeds $400 million.

Assuming a successful IPO, the company’s enterprise value at IPO would approximate $2.0 billion.

Management says it will use the net proceeds from the IPO as follows:

We currently intend to use the net proceeds from this offering to repay $41.5 million of outstanding borrowings under the Credit Facility. We will not receive any proceeds from the sale of shares of our common stock by the selling stockholders.

Management’s presentation of the company roadshow is not currently available.

Listed underwriters of the IPO are BofA Merrill Lynch, Morgan Stanley, Jefferies, Baird, Piper Jaffray, Citigroup, Goldman Sachs, KeyBanc Capital Markets, William Blair, Raymond James, Stifel, and Academy Securities.

Valuation Metrics

Below is a table of relevant capitalization and valuation metrics for the firm:

|

Measure [TTM] |

Amount |

|

Market Capitalization at IPO |

$1,672,948,500 |

|

Enterprise Value |

$2,029,469,500 |

|

Price/Sales |

2.30 |

|

EV / Revenue |

2.79 |

|

EV / EBITDA |

23.87 |

|

Earnings Per Share |

$0.36 |

|

Total Debt To Equity |

-9.99 |

|

Float To Outstanding Shares Ratio |

23.91% |

|

Proposed IPO Midpoint Price per Share |

$20.00 |

|

Net Free Cash Flow |

$207,458,000 |

(Source: Company Prospectus and IPO Edge)

As a reference, YETI’s clearest public comparable would be Newell Brands (NWL); below is a comparison of their primary valuation metrics:

|

Metric |

Newell Brands (NWL) |

YETI Holdings (YETI) |

Variance |

|

Price/Sales |

0.59 |

2.30 |

290.2% |

|

EV / Revenue |

1.17 |

2.79 |

138.7% |

|

EV / EBITDA |

8.41 |

23.87 |

183.8% |

|

Earnings Per Share |

$4.25 |

$0.36 |

-91.6% |

(Source: Company Prospectus, Yahoo Finance, and IPO Edge)

Conclusions

YETI wants to go public again after filing in mid-2016 and then withdrawing its IPO.

Since that attempt, the firm’s financials have shown significant fluctuation, especially a 22% decrease in topline net sales in 2017 vs. 2016.

While management has turned the company around so far in 1H 2018, two quarters of positive results don’t make a significant trend.

Additionally, competitor Newell Brands (NWL) is facing a credit downgrade due to a rising cost environment, which I believe may also impact YETI.

YETI’s controlling shareholder is also selling the majority of IPO shares offered, so only 12.5% of the IPO proceeds will go to the company. This doesn’t provide management with significant resources with which to pursue growth initiatives.

The firm is positive free cash flow and is growing its topline net sales by a healthy amount over 2017’s figures, but those are easy comparables to jump over.

I see a more difficult comparable when the firm reports its 1Q 2019 results and I expect that to show a much less impressive growth trajectory than the first half of 2018.

YETI has an enviable brand name among outdoor enthusiasts, but I’m not as enthusiastic about the IPO.

Expected IPO Pricing Date: October 24, 2018.

An enhanced version of this article on my Seeking Alpha Marketplace research service IPO Edge includes:

- Commentary

- Underwriter data

- Opinion on the IPO

Members of IPO Edge get the latest IPO research, news, market trends and industry analysis. Get started with a free trial.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment