Taseko Mines (TGB) should be reporting its Q3 2018 results soon. Its share price has performed very poorly during 2018 so far, due to a variety of factors. The share price was affected during the first part of 2018 by weak production results in Q4 2017 and Q1 2018 due to wildfire-related disruptions.

During the second half of 2018, sagging copper prices have weighed on Taseko as a relatively modest change in copper prices has a much more significant effect on margins at Gibraltar. For example, a 10% change in copper prices (at around US$3 per pound) may change margins by around 33%. While Taseko can’t control copper prices, it can exert some effect on operating costs at Gibraltar, which is important in times with lower copper prices.

Copper Prices

Copper prices (in Canadian dollars) have stabilised at near CAD3.70 per pound after a precipitous mid-year fall. This is around US$2.85 per pound, with the exchange rate hovering near CAD1.30 to US$1.00.

Taseko is partly hedged (with put options covering 5 million pounds of copper per month at a US$2.80 strike price until the end of the year) should prices fall further.

Source: InfoMine

Concerns about slowing global growth (including some relatively weak economic results from China) have weighed on copper prices recently. There is a belief that China’s demand for copper will be supported in 2019 by initiatives it takes to boost its economy and counter the threat from the trade wars though.

Notes On Q3 2018

My expectation for Q3 2018 is that copper production at Gibraltar will be similar to Q2 2018. With the extra day in the quarter, copper production should be close to 34 million pounds (100% basis).

I am not expecting production related surprises, but am quite interested in what the operating costs are at Gibraltar are for this quarter. I noted before that the combined site operating and capitalised stripping costs at Gibraltar (denominated in CAD per ton milled) had increased during the first half of 2018.

The per pound margins at Gibraltar aren’t huge at current copper prices, so it will be quite beneficial to Taseko if the combined site operating and capitalised stripping costs end up back in the CAD10 to CAD11 per ton milled range. A CAD1 per ton milled change in those costs affects Taseko’s total operating costs by around US$0.17 per pound, potentially making around a 20% difference to Gibraltar’s margins (such as around US$0.85 per pound with CAD10.50 per ton costs versus US$0.68 per pound with CAD11.50 per ton costs) at current copper prices.

Florence Copper

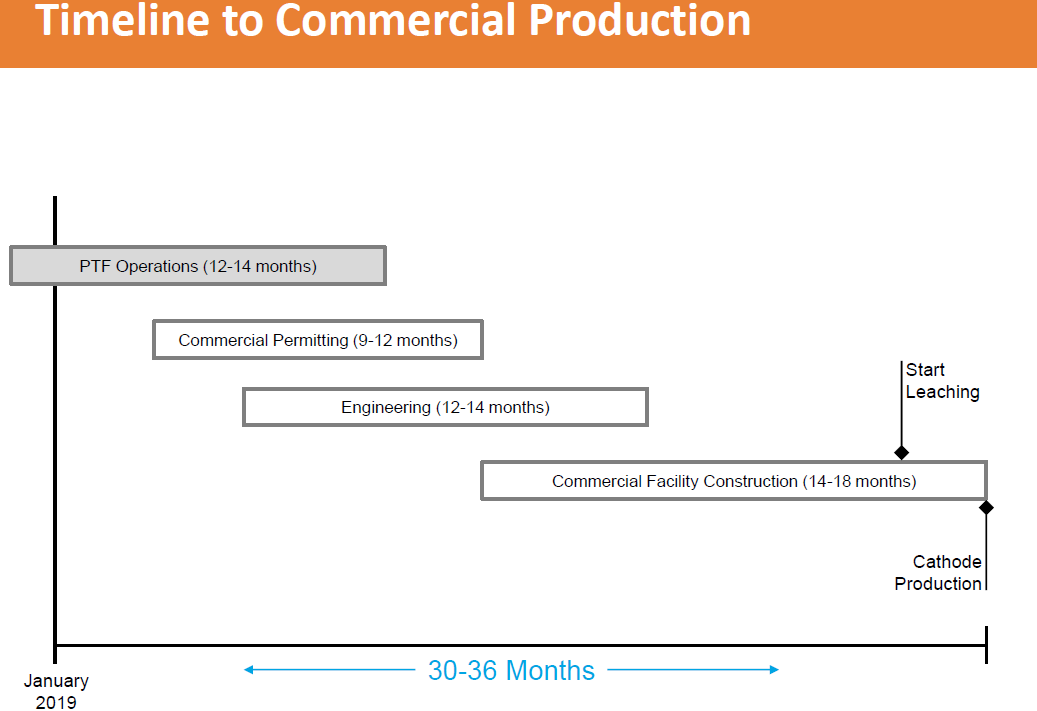

Florence Copper also appears to be progressing, with Taseko adding an October presentation about the project. Assuming that everything keeps progressing as planned, it appears that commercial production at Florence Copper could start in late 2021.

Source: Taseko Mines

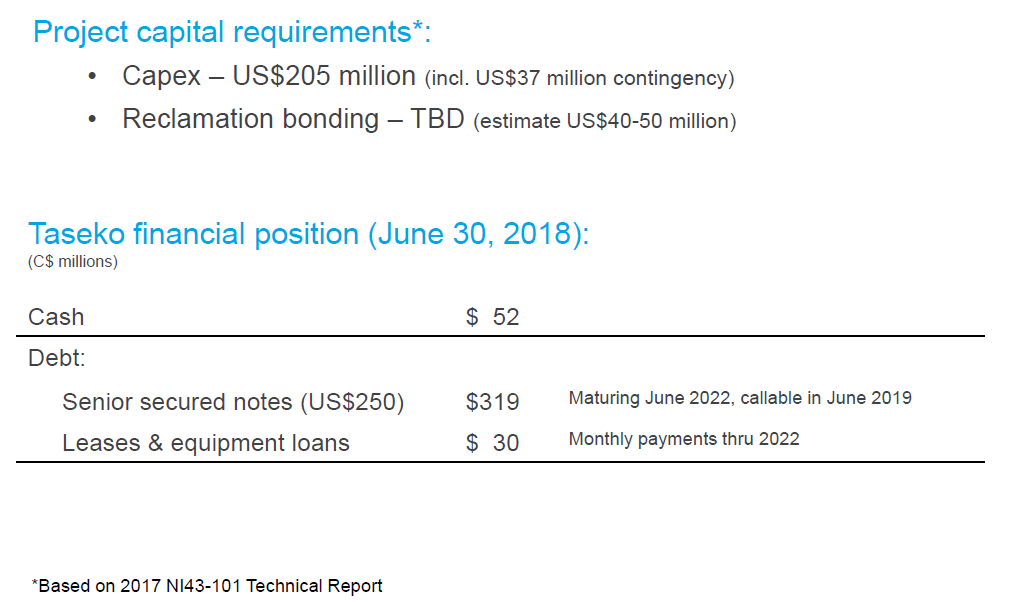

The financing issue will be interesting though, as Taseko will only be able to fund a small portion of the cost through cash on hand (based on its current cash position and expected cash flow at current copper prices).

Source: Taseko Mines

Taseko mentioned that it is targeting to have committed financing in place by the end of 2019. It does have a variety of options available to it, but needs to be careful with its decision. Its current US$250 million in senior secured notes are due in June 2022, and Florence Copper isn’t expected to start commercial production until late 2021. Thus Taseko will have a high amount of net debt by mid-2022 as Florence Copper will have only contributed a modest amount to Taseko’s cash flow by that point.

Conclusion

Taseko’s share price has been hampered by wildfire-related production issues in the first half of the year, and lower copper prices more recently. Being able to reduce costs at Gibraltar would significantly improve its margins at current copper prices, and if Taseko is able to show reduced costs, it could boost its stock.

Florence Copper offers a lot of potential for Taseko going forward, but it has some challenging decisions to make around financing the project and not getting itself into debt and interest cost trouble before Florence can start generating significant positive cash flow.

Free Trial Offer

We are currently offering a free two-week trial to Distressed Value Investing. Join our community to receive exclusive research about various energy and mining companies and other opportunities along with full access to my portfolio of historic research that now includes over 1,000 reports on over 100 companies.

Disclosure: I am/we are long TGB.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Be the first to comment