Parsley Energy (PE) has been one of the fastest-growing oil producers from the Permian Basin and it looks all set to continue growing in the future. The company has a large inventory of drilling locations and sufficient financial resources to fund its future growth. The improvement in oil prices in the Permian Basin will likely give a boost to the company’s earnings. Parsley Energy stock has underperformed this year, and I believe investors should consider buying on weakness.

Image courtesy of Pixabay

Parsley Energy is a Permian Basin-focused oil producer which mainly operates in the Midland and Delaware regions of the shale oil play located in Texas and New Mexico. The company owns an interest in 164,000 acres in the Midland Basin and 46,000 acres in the Delaware Basin that hold 416.4 million barrels of proven reserves which are mostly crude oil (59.7%) and natural gas liquids (22.2%).

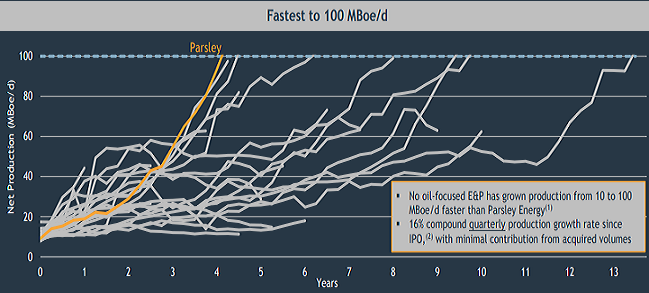

The Permian Basin is the premier U.S. shale oil play where a number of oil producers operate ranging from the oil major Exxon Mobil (XOM) to small independent exploration and production company Jagged Peak Energy (JAG). But what sets Parsley Energy apart is that it is the quickest among oil-weighted independent exploration and production companies to reach the 100,000 barrels of oil equivalents per day milestone from 10,000 boepd. The company IPO’d in 2014 and four years later, its production crossed averaged 107,813 boepd in Q2-2018. Its production growth clocked in at 77.5% for FY-2017, 70.6% for Q1-2018, and 66.6% for Q2-2018 on a year-over-year basis.

Source: Investor Presentation, Parsley Energy, August 2018.

Parsley gets most of its production from the Midland Basin and its output is mainly crude oil. Its second-quarter production mix was 63% crude oil, 21% natural gas liquids, and 16% natural gas. The above-mentioned production growth has come as the company increased drilling activity and brought dozens of wells online. In the second quarter, it placed 45 gross operated horizontal wells to production. By comparison, in the same quarter last year, it completed 27 gross horizontal wells. The company also operated 16 rigs in the second quarter of 2018, which was substantially higher than 11 rigs in Q2-2017.

Note that Parsley has managed to grow its production by 15.4% on a sequential basis from Q1-2018 without deploying any additional rigs. Instead, the company has been trying to optimize its operations by pumping more oil without increasing the number of drilling rigs. In the second quarter, Parsley reduced its cycle time and gradually increased its working interest by consolidating oil production blocks, which had a positive impact on production. Moving forward, Parsley will further optimize its operations by gradually shifting to larger wells per pad. Currently, it is running two to three wells per pad program, but it will increase this to three to four well pads in the future. The management has said that they may even go as high as six wells per pad. The focus optimization may have a negative impact on production growth but it will likely substantially improve capital efficiency, allowing the company to deliver more by spending less in the long run. The company will likely continue operating 16 rigs this year and may deploy one to two additional rigs in 2019. (Parsley hasn’t laid out its 2019 financial and operational plans.)

What I also like about Parsley is that it has ample firepower to continue growing in the future. The company has tapped into just a fraction of its reserve base. It has identified more than 6,000 gross operated development drilling locations in its proven reserves, with enough wells to power the company’s production for more than a decade at the current drilling pace. In the Glasscock, Reagan and Upton counties of the Midland Basin, for instance, the company has identified more than four decades of drilling inventory. This will continue to fuel the company’s production growth for years. Furthermore, the company has identified 4,000 delineation inventory locations in multiple zones (such as Middle Spraberry and Second Bone Spring) which may hold substantial oil and gas reserves. The size of its inventory with proven reserves may meaningfully climb in the future.

Furthermore, Parsley also has sufficient funds available to finance its exploration and production operations. The company has budgeted $1.7 billion of capital expenditure for this year. So far, it has financed more than half of its capital spending from internally generated cash flows. Parsley spent $901 million as capital expenditure in the first half of the year, of which 64% was backed by $572.9 million of cash flow from operations (ex. working cap. changes).

Although Parsley is facing a cash flow shortfall (since CapEx is much higher than op. cash flows), that’s not a major problem because the company is in great financial health. It benefits from having low levels of debt and high levels of liquidity which can be used to bridge any funding gap.

At the end of the second quarter, Parsley carried $1.98 billion of net debt (total debt minus cash) which translated into a net debt ratio of 27%. The leverage metric is one of the lowest among all mid-cap oil producers, most of which, including Laredo Petroleum (LPI), Newfield Exploration (NFX), and PDC Energy (PDCE), carry a net debt ratio of more than 30%. Additionally, Parsley has no significant near-term debt maturities. The earliest maturity on its long-term debt is the $400 million of senior notes due 2024 followed by a total of $1.1 billion of notes due in 2025. The company also has $1.3 billion of liquidity, which includes $301 million of cash reserves and $991 million available under the revolving credit facility.

Moving forward, Parsley’s profits and operating cash flows will likely climb substantially as the company continues to grow its production and benefits from improvement in oil prices. The price of the U.S. benchmark WTI crude has stayed north of $70 a barrel since mid-September, up from $65 a barrel in mid-August. The recent strength has been driven by the drop in oil exports from Iran ahead of the US sanctions which will take effect from November. As per data from Refinitiv Eikon, the country’s exports have tumbled to 1.33 million bpd from 2.5 million bpd in April when President Trump withdrew from the nuclear deal.

Meanwhile, the oil prices at the Permian Basin have also recovered. The fears related to supply bottlenecks pushed the region’s Midland benchmark to as low as $17 a barrel below the US benchmark in August but the difference has narrowed to just $6 a barrel. Plains All American (PAA) is slated to bring the expanded Sunrise Pipeline to service by early next month which will lift the region’s takeaway capacity by 500,000 bpd. A number of new pipelines, such as Plains All American’s Cactus II and Phillips 66 Partners (PSXP)’s Gray Oak Pipeline, representing a total takeaway capacity of two to three million bpd, will start coming online from the second half of 2019. That will push Permian Basin prices even higher.

The improvement in region’s prices, combined with strong production growth, will lift Parsley’s profits and cash flows.

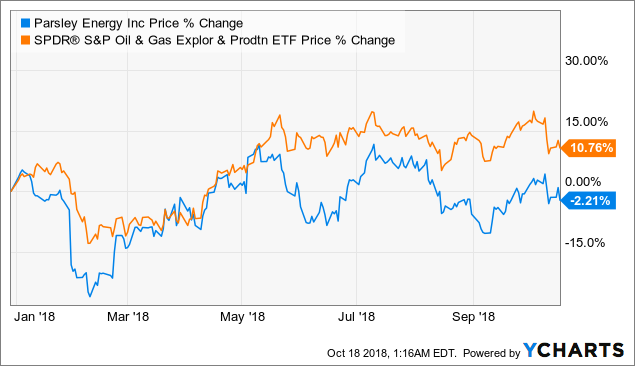

Shares of Parsley Energy have underperformed this year, falling by 2.2% while its peers, as measured by SPDR S&P Oil & Gas Exploration & Production ETF (XOP), have climbed ~11%. This has made Parsley a relatively cheaper stock as compared to its Permian Basin peers. The company’s shares are priced 12.9-times next year’s Thomson Reuters consensus earnings estimate while its rivals, including Centennial Resource Development (CDEV), Concho Resources (CXO), Pioneer Natural Resources (PXD), Energen (EGN), and Jagged Peak Energy (JAG), are all trading at more than 15-times future earnings. I think the weakness in Parsley Energy stock could be a buying opportunity. The company’s shares will likely bounce back as its production continues to grow, earnings and cash flows climb, and oil prices in the Permian Basin recover.

Note from author: Thank you for reading. Please share your comments below. If you like this article, then please follow me by clicking “ Follow” at the top of this page.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment