Investment Thesis

Many brick and mortar retailers no longer trade solely on traditional fundamental metrics. Instead, the market tends to price their equity on the e-commerce resistance of their business model. A retail company like Walmart (WMT) could miss analyst expectations on earnings, but if it reports strong digital sales growth, the stock could soar.

Pure-play grocers were traditionally exempt from this thinking because investors perceive grocery as an e-commerce resistant business. The market’s attitude changed in 2017 when Amazon (AMZN) announced it would acquire Whole Foods and the market punished grocers across the board. Now, grocers will have to show Wall Street that they are willing to compete in an increasingly digital retail landscape.

Kroger (KR) is the largest operator of grocery stores in the country and has the scale, capital, and willingness to compete in the digital world. The roll-out of curbside pickup and grocery delivery has been impressive, and the resulting growth in digital sales has lifted the stock price. But the announcement of the Kroger Ship beta is exciting and could be a potential driver of digital sales growth for years to come. I believe this, along with other e-commerce initiatives, gives investors an opportunity to buy Kroger on the weakness that arose from a soft earnings report in September.

A Recap on Kroger’s Year

Kroger has been a battleground stock for over a year since Amazon announced it would acquire Whole Foods last summer. Bears argued that traditional grocery shopping is on its way out the door and that Amazon will eat its competitors’ lunch, and earnings multiples should reflect that. Bulls claimed that the selling was overdone and Kroger would be able to compete in the new retail environment.

I fell in the bull camp. Headwinds aside, Kroger was dirt cheap on almost every conceivable metric. Its network of stores is massive, and I had seen their e-commerce investments starting to pay off first-hand, with my local Ralph’s (Kroger subsidiary) already rolling out curbside pickup and grocery delivery. Groceries are a defensive industry, and well-run grocers can grow sales and profits even during an economic downturn, evidenced below:

KR EPS Diluted (TTM) data by YCharts

Above all, Kroger has a strong portfolio of private-label brands that it can sell for materially higher gross margins than third-party branded goods. There is an argument that today’s shoppers care less about the brand name than previous generations, and if the case holds any water, Kroger is well-positioned to capitalize on this trend.

The Market Has Rewarded Tech-Savvy Retailers

There are several examples of the market assigning higher earnings multiples to retailers that can drive digital sales growth. This revaluation results in shareholder returns and a lower cost of capital for the retailers who can innovate in the eyes of the market.

1. Walmart (WMT)

In a push to grow its e-commerce operations, Walmart acquired Jet.com on August 8, 2016, for $3.3 billion in cash and stock. From then on out, Walmart began reporting digital sales growth consistently in the mid-to-high-double-digit numbers as it grew its online sales at a brisk pace. Additionally, Walmart has been aggressively rolling out grocery pickup at its locations.

Though earnings didn’t increase materially, the market eventually assigned a higher multiple to Walmart, presumably due to the resilience that a diversified revenue stream provides. As a result, the market rewarded WMT shareholders when the earnings multiple expanded from a market discount to a market premium:

WMT data by YCharts

WMT data by YCharts

2. Kohl’s (KSS)

In October 2017, Kohl’s announced it would partner with Amazon to allow customers to return Amazon-purchased items at certain Kohl’s department stores. Kohl’s would also debut Amazon smart home products at select stores.

This symbiotic relationship would presumably drive foot traffic to Kohl’s stores. If Amazon is the great white shark of retail, preying on the market share of other retailers, Kohl’s decided it would happily be Amazon’s remora (the fish that eats parasites from the shark’s skin):

Even though Kohl’s sales didn’t explode as a result of the partnership, the market rewarded Kohl’s shareholders handsomely, with shares appreciating about 100% in a matter of a year.

KSS data by YCharts

KSS data by YCharts

3. Macy’s (M)

Macy’s is a company that in 2016-2017 did not trade on fundamentals and instead traded on the fact that it was a department store. Peers like Sears (SHLD) and JC Penney (JCP) were suffering, and the market predicted Macy’s would be the next victim of the decline of the department store. Despite having a strong brand, consistent earnings, and a prime real estate portfolio, the company traded at dirt cheap multiples: low P/E, low EV/EBITDA, and high dividend yield.

Around November of 2017, the market woke up to the fact that Macy’s was a relatively savvy digital retailer. Its vast network of stores and the promotional nature of its sales translated into an above-average online user experience. Customers have many physical locations to return items to; they could try an item in-store and order it online, and they could get a good deal from one of the many promotions available to Macy’s shoppers.

These factors made Macys.com the number one trafficked website for retail apparel according to SimilarWeb‘s index:

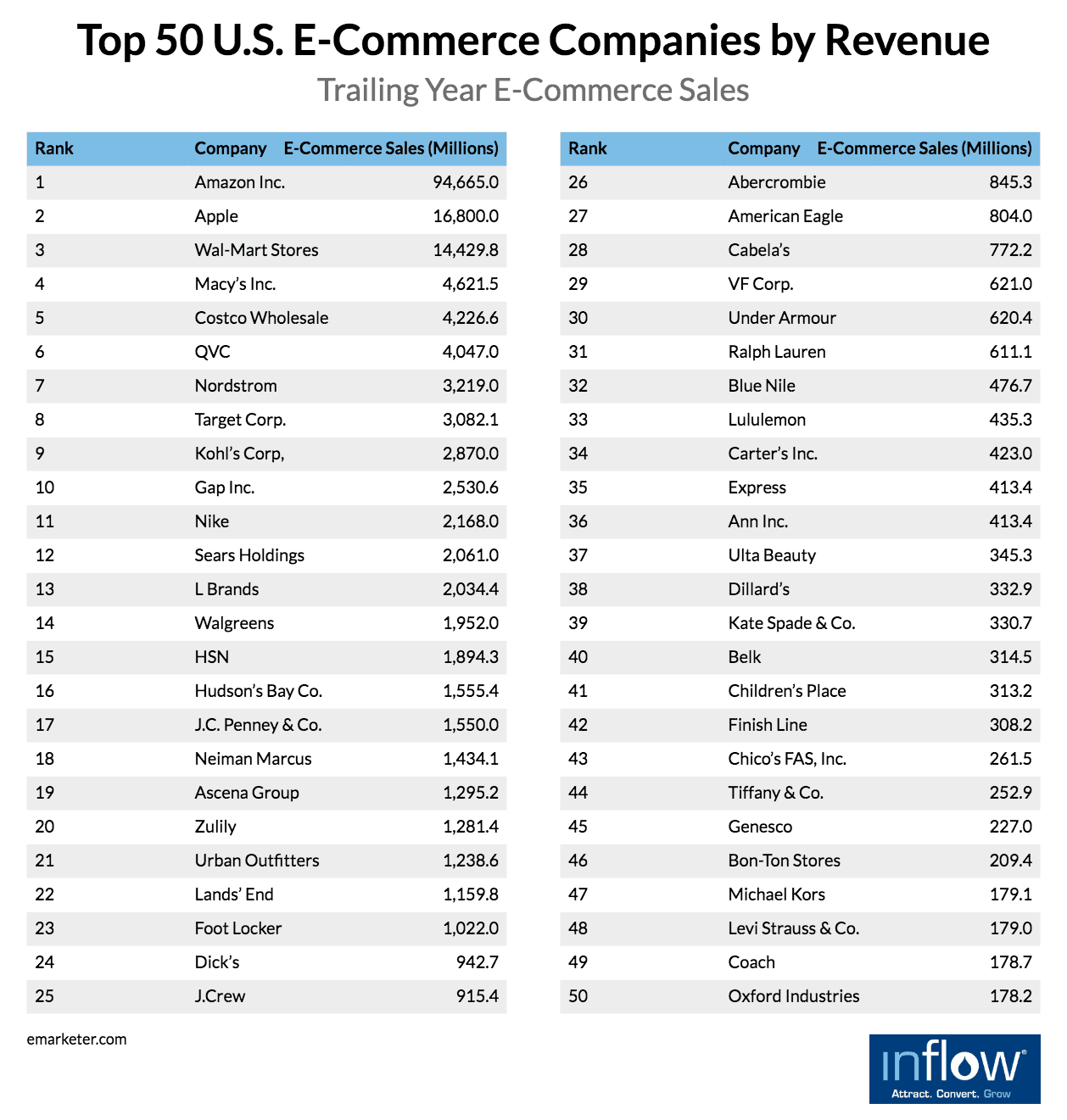

Additionally, Inflow ranked Macy’s the #4 retailer by e-commerce sales:

The market’s narrative about Macy’s changed from that of a dying department store to that of a business in transition to brick-and-click. The sales multiple expansion resulting from the new narrative has caused Macy’s shares to soar almost 100% from 52-week lows, and it still appears cheap at these levels:

The market’s narrative about Macy’s changed from that of a dying department store to that of a business in transition to brick-and-click. The sales multiple expansion resulting from the new narrative has caused Macy’s shares to soar almost 100% from 52-week lows, and it still appears cheap at these levels:

M data by YCharts

M data by YCharts

Kroger Could Easily Follow

Kroger has many irons in the e-commerce fire that will allow it to remain competitive as a grocer, but moreover, these initiatives will drive the market to revalue Kroger’s equity.

1. Kroger Ship

Kroger Ship is an exciting investment by Kroger that combines three of Kroger’s strongest assets into an e-commerce offering:

- its vast network of stores and distribution centers,

- its private label portfolio, “Our Brands,” which has materially higher margins than third-party products,

- and its data on its customers, which it has been collecting for years through rewards memberships

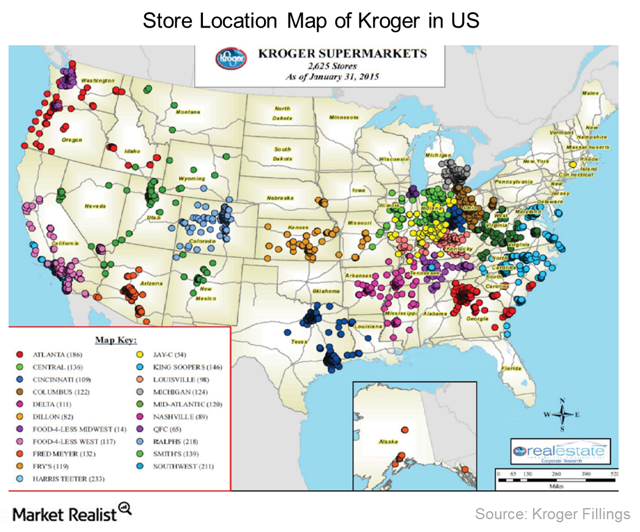

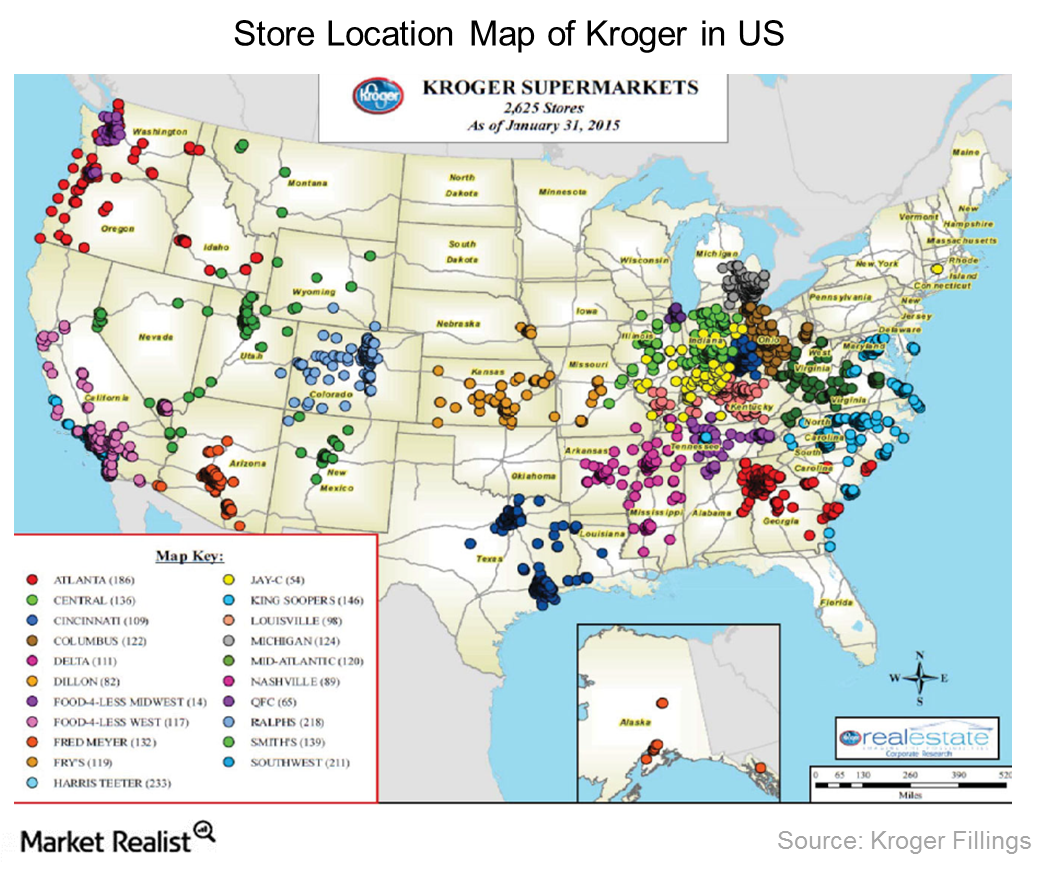

Kroger Ship is Kroger’s foray directly into e-commerce, and it has the potential to be a digital sales driver. Kroger’s existing network of stores serves as a robust distribution network:

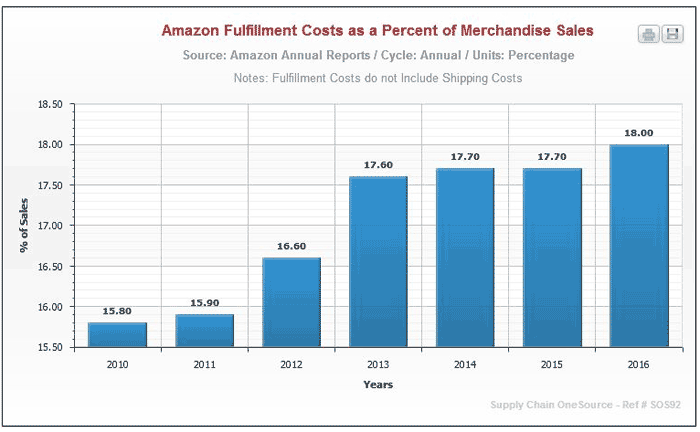

By only offering Ship to markets where Kroger has a strong foothold, it can keep fulfillment costs low by operating where it has a last-mile advantage without outlaying additional capital. Fulfillment costs are the bane of e-commerce operations, with e-commerce juggernaut Amazon facing increasing fulfillment costs as a portion of merchandise revenue year after year.

By only offering Ship to markets where Kroger has a strong foothold, it can keep fulfillment costs low by operating where it has a last-mile advantage without outlaying additional capital. Fulfillment costs are the bane of e-commerce operations, with e-commerce juggernaut Amazon facing increasing fulfillment costs as a portion of merchandise revenue year after year.

Source: Supply Chain Digest

By keeping fulfillment costs low, selling private label goods with high margins, and using customer data to advertise its offerings effectively, Kroger Ship seems like a recipe to drive digital sales growth and eventually add to the bottom line.

2. Grocery Pickup

From an investor’s perspective, investing in grocery pickup is an attractive strategy. It saves customers time and does not require much in the way of additional expenses. Kroger offers Grocery Pickup at more than 1,000 locations.

Fulfilling grocery pickup orders presents its own set of challenges. Kroger, ever a forward-looking business, made an investment in Ocado (OTCPK:OCDGF) which employs armies of robots to fulfill orders. Much like Amazon’s purchase of Kiva to optimize its warehouses with robotics, Kroger’s partnership with Ocado could result in cost savings on its grocery pickup and other e-commerce operations.

3. Instacart & Grocery Delivery

Grocery delivery is a dubious proposition from a profitability standpoint, but Kroger is diving headfirst into grocery delivery organically through its subsidiary Grocery Pickup (formerly Clicklist) and third-party provider Instacart.

Due to perishability issues, grocery delivery is time sensitive, which adds an element of logistical complexity that translates into high costs to providers. If wealthier customers are willing to accept these added costs, then grocers would not need to subsidize their grocery delivery offerings to grow them.

Grocery Pickup’s name change could be a result of Kroger’s pivot from delivery to invest in curbside pickup, instead preferring to outsource transportation and its related expenses to Instacart or other third-party operators while still growing digital sales.

4. Smart Stores

Kroger is experimenting with smart stores which have automatically-changing price tags with time-sensitive deals. Eventually, Kroger may work with a partner such as Alibaba (BABA) to develop an Amazon Go-like cashier-less offering.

Adding technology to stores, while not necessarily driving digital sales growth, will cut out operational labor costs and drive efficiencies at the store level, which will improve margins and the bottom line.

Low Valuation Creates Opportunity

Fundamentally, Kroger is a stable company. It is currently rated investment grade by all three agencies who cover the company. Kroger’s net debt/TTM adjusted EBITDA is low at 2.59, with management targeting a range between 2.3x and 2.5x.

This range appears to be a reasonably low level of leverage, especially given that Kroger has high capital expenditure requirements. Kroger spent $2.9 billion in TTM capital expenditures, which consumed a large portion of operating cash. Still, the company was able to generate ample free cash flow to pay dividends and retire shares.

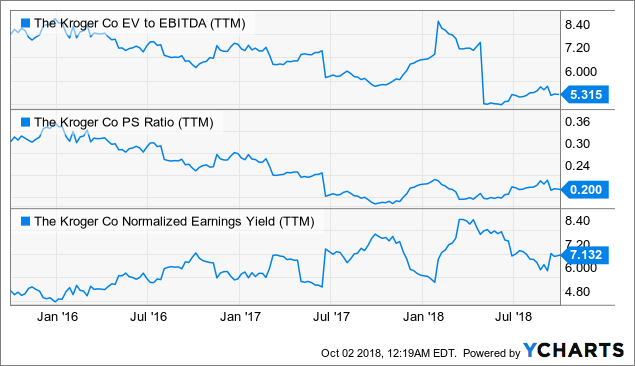

Despite its robust earnings, Kroger is currently trading at depressed multiples across the board, relative to its history.

KR EV to EBITDA (TTM) data by YCharts

KR EV to EBITDA (TTM) data by YCharts

A revaluation of Kroger to an earnings yield of 5% (or a price to earnings ratio of 20) from a base of $2.00 per share (the low-end of management’s guidance) would result in a price per share of $40, which is over 33% upside from today’s close. If management can deliver toward the high-end of its guidance while simultaneously growing its digital revenue, this revaluation could easily occur within the next twelve months. In the meantime, Kroger will continue to retire shares at this relatively depressed valuation as part of the stock buyback program.

Although Kroger has already experienced substantial share price appreciation over the last twelve months, it is still just as cheap as it was pre-Amazon/Whole Foods tie-up. Since then, it has made a severe dent in its outstanding share count. Investors who are looking to build a long position should see the weakness that arose from the latest earnings report as an opportunity to acquire stock.

Disclosure: I am/we are long KR, WMT, AMZN.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment