Preface

The following article was originally published for subscribers of my exclusive marketplace, The Formula, last month when KALV was trading at $17.05/share.

| Timeline | Price Target | Relevant Events |

| 12-18 months | $30 |

|

Diabetic Macular Edema

Figure 1: Leaky blood vessels cause edema and subsequent loss of vision (Source: NIH)

Pathophysiology

Diabetic macular edema (DME) is one of the many terrible outcomes associated with diabetes. Over time, diabetes is known to wreak havoc on the blood vasculature and the eyes are not spared. The damaged blood vessels leak fluid within the eyes, causing inflammation and edema. The edema leads to progressive blindness.

Prevalence

It’s estimated that between 750,000 to 1,000,000 patients in the US suffer from DME. Because of the increasing prevalence of type two diabetes in our society, we can expect this number to grow, quite significantly, in the future.

Treatment

Treatment is directed towards the reduction of edema and inflammation in the affected eyes. Fortunately, there are a few treatment options that are effective and safe in the majority of DME patients. Let’s further assess the treatment landscape for DME:

- Anti-VEGF injections – Avastin (off-label use via Roche), Eylea (Regeneron), and Lucentis (Roche, Novartis)

Vascular endothelial growth factor (VEGF) is a protein that is produced in response to hypoxia (low oxygen levels). VEGF stimulates the growth of blood vessels and increases the permeability of existing blood vessels in an attempt to increase oxygen levels. Unfortunately, it is common for VEGF to be overproduced, leading to damage to the eye.

Anti-VEGF injections are delivered directly into the eye on a monthly basis for up to 2 years or until the macula is dry. Anti-VEGF, in responsive patients, is heralded as a “miracle” treatment because of the depth of its ability to restore vision. “Anti-VEGFs work well if used early in the course of disease, aggressively and possibly long term.” It is estimated as much as 50% of patients are not adequately-responsive to anti-VEGF therapy. For our purposes (to be conservative), we will use a figure of 33%.

Costs:

Eylea $1850/injection (FDA-approved for DME), Lucentis $1200/injection (FDA-approved for DME), Avastin $50/injection (prescribed off-label for DME). Costs are just for one injection in one eye. Here is an interesting piece discussing the differences in costs between these drugs and the reasons doctors still write prescriptions for the more expensive options.

Limitations of anti-VEGF therapy summed,

There are still patients that have suboptimal improvement, so better efficacy is still an unmet need. Durability is definitely an issue. Anti-VEGF therapy works very well on average, but it takes long-term treatment and frequent administration. We want a treatment that lasts longer and works better and faster. We want to prevent recurrences, too.

In Development:

Brolucizumab (Novartis) is an anti-VEGF therapy that, compared to standard anti-VEGFs, allows for more concentrated molar dosing. Brolucizumab is currently going head-to-head with Eylea in a phase 3 trial for DME. Data is expected in 2021.

Allergan’s Abicipar pegol proved non-inferior to Lucentis in a phase 3 trial in July of this year. This anti-VEGF therapy can be administered less often than standard anti-VEGFs (every two or three months).

Roche’s RG7716 is a bi-specific molecule that inhibits both Ang2 and VEGF. It showed promise in a phase 2 trial for DME earlier this year.

- Anti-inflammatory agents – corticosteroids (Ozurdex, a dexamethasone intravitreal implant by Allergan & Iluvien, afluocinolone acetonide intravitreal implant by Alimera Sciences) and NSAIDs

If a patient is minimally- or non-responsive to anti-VEGF therapy after six months, clinicians usually begin to seek other options.

Corticosteroids are, generally, regarded as the second-line of treatment after anti-VEGF failure. However, the number of diabetic patients appropriate for corticosteroids (given the many side effects associated with them) are limited. Additionally, there are concerns of efficacy and safety surrounding corticosteroids in DME.

Schwartz, Scott, Stewart, & Flynn, 2016 conclude:

Currently, surgeons have three intravitreal corticosteroid options for the treatment of DME: the dexamethasone delivery system, the fluocinolone acetonide insert, and off-label intravitreal triamcinolone acetonide. All three agents, as well as the larger fluocinolone acetonide surgical implant, are associated with risks of cataract progression and IOP elevation. There is no current consensus regarding the indications for intravitreal corticosteroids, but they are generally regarded as second-line agents for patients with center-involving DME who respond insufficiently to a series of anti-VEGF injections.

Interestingly, a study assessing anti-VEGF injections in combination with corticosteroid injections versus anti-VEGF injections alone revealed no added efficacy from corticosteroids.

- Surgery – appropriate for a very limited number of patients; focal laser (used increasingly less)

Unmet Need

While these treatments are effective for the majority, there is a significant subset of DME patients who do not respond and end up having progressive disease. Therefore, there is an unmet medical need for new therapeutics to address DME patients who are unresponsive and/or minimally responsive to standard-of-care treatments.

The problem as proposed by Diabetes, 2015:

An increasing number of patients with diabetes suffer from vision-threatening diabetic retinopathy, i.e., proliferative diabetic retinopathy (PDR) and diabetic macular edema (DME), worldwide. Vascular endothelial growth factor (VEGF) plays a key role in the angiogenic responses in PDR, and the development of anti-VEGF therapy has reduced the burdens of PDR patients. Retinal vascular permeability leads to morphological and functional damages in the neuroglial components in the retinas and concomitant visual disturbance in DME. Although anti-VEGF agents have been effective for many patients with DME, their effects are often slow and partial and the benefits are limited, suggesting that there are other cellular and molecular mechanisms in addition to VEGF.

There is a clear need for a safe and effective second-line treatment for patients who are minimally- or non-responsive to anti-VEGF therapy.

Proposed Solution

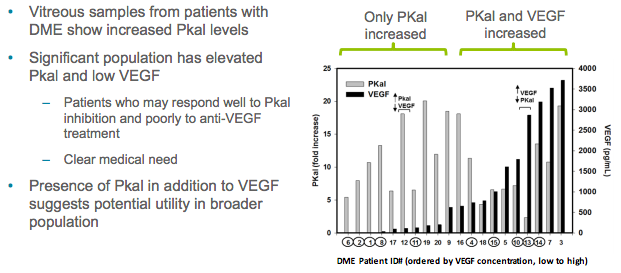

Plasma Kallikrein (PKal) is an enzyme that is emerging as a critical player involved with the pathophysiology of DME. PKal has been demonstrated to be 11.0-fold increased in vitreous from subjects with DME. Although a KalVista slide suggests that PKal and VEGF have an inverse relationship (possibly, in an attempt to provide an explanation as to why anti-VEGF non-responsive patients would be responsive to PKal inhibition),

Source: KalVista Corporate Deck

other evidence suggests there is no correlation between VEGF and PKal levels:

While the vascular endothelial growth factor (VEGF) level was also increased in DME vitreous, PKal and VEGF concentrations do not correlate (r = 0.266, P= 0.112).

I will choose to describe PKal simply as an enzyme that has broader implications in DME pathophysiology than does VEGF and is, additionally, independent of VEGF. Supporting evidence:

Using mass spectrometry–based proteomics, we identified 167 vitreous proteins, including 30 that were increased in DME (fourfold or more, P < 0.001 vs. MH). The majority of proteins associated with DME displayed a higher correlation with PPK than with VEGF concentrations. DME vitreous containing relatively high levels of PKal and low VEGF induced retinal vascular permeability when injected into the vitreous of diabetic rats, a response blocked by bradykinin receptor antagonism but not by bevacizumab. Bradykinin-induced retinal thickening in mice was not affected by blockade of VEGF receptor 2. Diabetes-induced retinal vascular permeability was decreased by up to 78% (P < 0.001) in Klkb1-deficient mice compared with wild-type controls. B2- and B1 receptor–induced RVP in diabetic mice was blocked by endothelial nitric oxide synthase (NOS) and inducible NOS deficiency, respectively. These findings implicate the PKal pathway as a VEGF-independent mediator of DME.

There is sufficient laboratory evidence suggesting PKal promotes vascular permeability in DME, independent of VEGF. Preclinical evidence also suggests targeting PKal proves beneficial in animal models of DME.

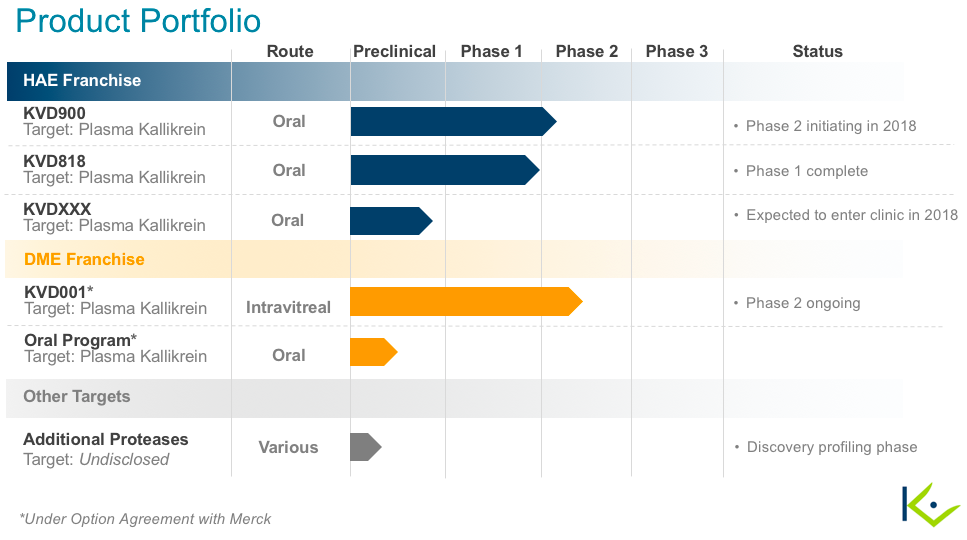

KVD001

KalVista Pharmaceuticals (KALV) is developing KVD001 for DME. KVD001 is a potent inhibitor of human plasma kallikrein delivered via intravitreal injection. I am choosing to focus on intravitreal injection as opposed to KalVista’s oral plasma kallikrein inhibitors because I believe delivery via intravitreal injection will prove far more beneficial than oral administration for the following reasons:

- Intravitreal injection delivers the medication directly to the site of edema and inflammation (increased efficacy), avoiding systemic exposure and the subsequent side effects possibly involved with systemic exposure (increased safety)

- Other DME medications are delivered via intravitreal injection (patients and primary care provider’s are already accustomed to this)

Patent Life

KVD001 is covered by U.S. patents and patent applications covering composition of matter, methods of treatment, solid form and clinical formulations. The anticipated expiration dates of these patents, or patents arising from applications, range from 2032 to 2038, absent any adjustments or extensions.

Source: KalVista’s most recent 10-K

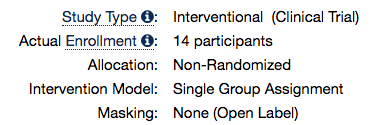

KVD001 Phase I Trial Design

Insight: Phase 1 trials serve to estimate tolerability and characterize pharmacokinetics and pharmacodynamics. They can also provide preliminary data into drug activity. Oftentimes, the goal is to estimate the largest tolerable dose that can be administered (coined, “maximally tolerated dose”). Researchers begin with a very small dose. If no significant toxicity occurs, they move onto a larger dose, and so on. When researchers do observe unacceptable toxicity, the dose escalation is terminated and the previous tolerated dose is selected. Source: Fundamentals of Clinical Trials, 5th Edition

Below, we will assess phase 1 trial design for KVD001.

Concept: The ideal clinical trial is randomized and double-blinded.

- Randomized: patients who meet trial inclusion criteria are assigned either to the placebo arm or the treatment arm.

- Double-blinded: patients in both arms are unaware of which arm they were assigned to.

This concept, generally, applies to later-stage trials. Let’s look at the brief summary of KalVista’s phase 1 trial:

This is a Phase 1 study to investigate the safety, tolerability of the novel plasma kallikrein inhibitor, KVD001 in subjects with diabetic macular edema. The study is the first step to investigate the hypothesis that plasma kallikrein plays an important role in the disease process behind diabetic macular edema in many patients.

Study Design:

Because the trial involved one arm (a treatment arm), it was not possible for it to be randomized nor blinded.

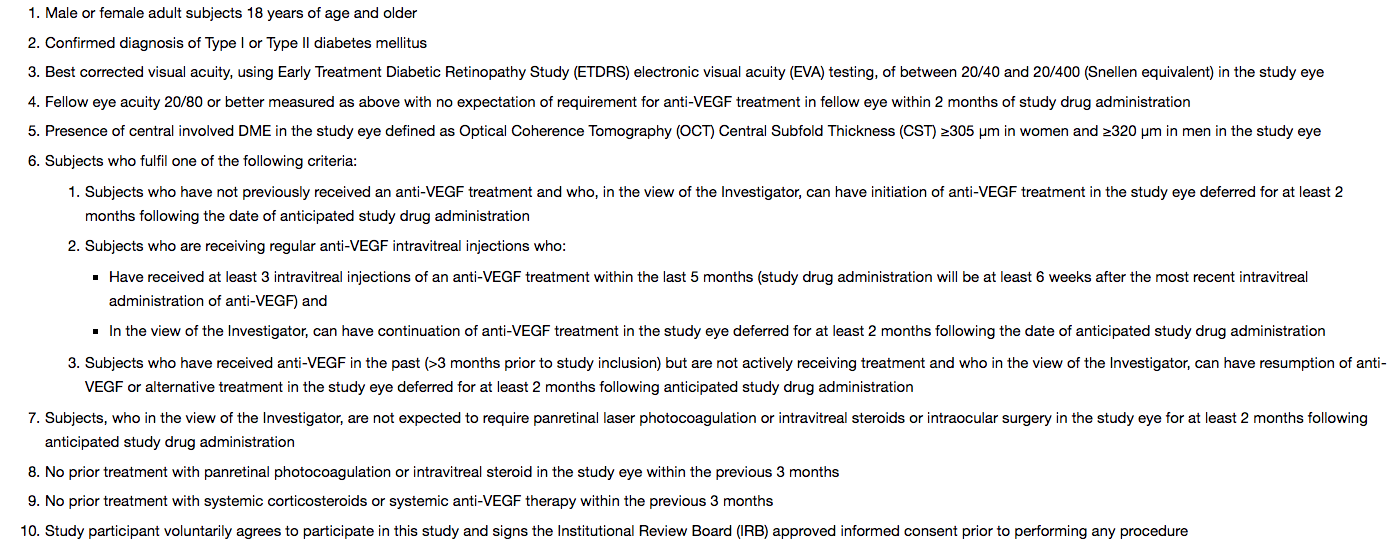

Inclusion Criteria:

According to KalVista, “All patients had previously received anti-VEGF treatment.” It is worth noting that there is no way to tell if these patients were actually minimally- or non-responsive towards anti-VEGF therapy, as many of them possibly hadn’t completed a full schedule of it. However, again, this is a phase 1 trial just exploring the safety, tolerability, and efficacy of a drug in an indication.

Other than that, there is not much to draw from the inclusion criteria.

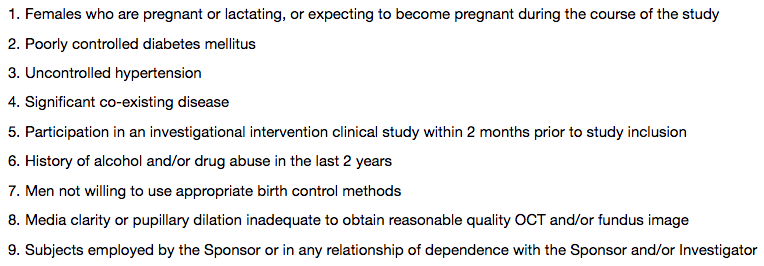

Exclusion Criteria:

It is normal for phase 1 studies to exclude pregnant or lactating patients because we still do not know much about the drug and this population of patients are at-risk.

Novartis’ DME trial also excludes patients with poorly-controlled DM.

Locations:

Locations in this trial are limited to the US, but include all regions (North, South, East, West). Such variability in treatment locations enhances trial credibility. Also noteworthy: US sites are, generally, reliable.

Primary Outcome:

- Number of participants with Adverse Events as a measure of safety and tolerability [ Time Frame: 56 days ]

Phase 1 trials are, primarily, concerned with the safety and tolerability of a new drug. Safety is, and always will be, #1.

Secondary Outcomes:

- Measurement of KVD001 plasma levels over time following intravitreal injection (with calculation of Tmax, Cmax, AUC and t1/2) [ Time Frame: 28 days ]

- Best Corrected Visual Acuity as measured by ETDRS EVA [ Time Frame: 56 days ]

Phase 1 trials are also very concerned with how the drug works and how it can be dosed.

Importantly, “Best Corrected Visual Acuity as measured by ETDRS EVA” is a relevant efficacy measure for this condition. Novartis is also utilizing the same outcome for their phase 3 trial.

Summary

Based on the above information, the phase 1 trial KalVista designed was an appropriate and reliable one. Additionally, the trial gave us a lot of insight into the efficacy of the drug within the disease process, which is not common of phase 1 trials, which generally utilize healthy volunteers to first assess for the safety of a drug.

KVD001 Phase I Trial Results

Unfortunately, a lot of specifics concerning the results are left out (perhaps, for competitive reasons).

Most importantly, KVD001 was “well tolerated”.

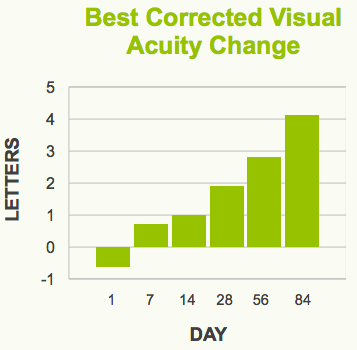

On the efficacy side, KVD001 demonstrated improvement in mean visual acuity change after just one dose in 14 patients:

Source: KalVista Corporate Deck

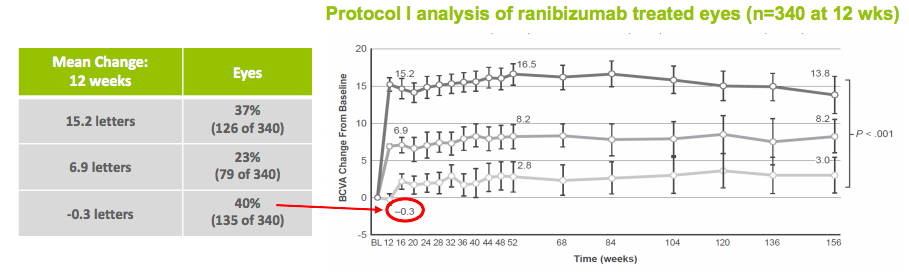

The 12-week results compare favorably to anti-VEGF therapy:

Bear in mind, KalVista’s results are in patients who had tried anti-VEGF therapy. So, these are, theoretically, non-responders to anti-VEGF therapy. Additionally, KVD001 was administered just one time in this trial. Contrarily, anti-VEGF therapy is administered every month.

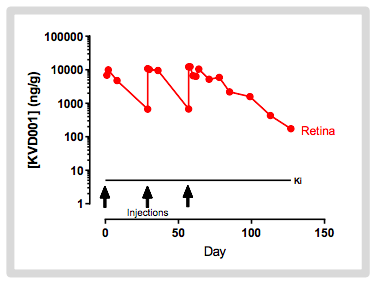

A preclinical profile of KVD001 demonstrates the drop-off in exposure that occurs after a few weeks:

Theoretically, more frequent dosing would result in better efficacy. In a phase 2 trial, KVD001 will be administered four times over the course of three months.

Merck Option Agreement

After phase 1 data, Merck entered into an option agreement with KalVista:

On October 6, 2017, the Company’s wholly-owned U.K. based subsidiary KalVista Pharmaceuticals Limited (“KalVista Limited) and Merck Sharp & Dohme Corp. (“Merck”) entered into an option agreement (the “Option Agreement”). The Company is the guarantor of KalVista Limited’s obligations under the Option Agreement. Under the terms of the Option Agreement, the Company, through KalVista Limited, has granted to Merck an option to acquire KVD001 through a period following completion of a Phase 2 clinical trial. The Company, through KalVista Limited, has also granted to Merck a similar option to acquire investigational orally delivered molecules for DME that the Company will continue to develop as part of its ongoing research and development activities, through a period following the completion of a Phase 2 clinical trial. The Company, through KalVista Limited, also granted to Merck a non-exclusive license to use the compounds solely for research purposes, and is required to use its diligent efforts to develop the two compounds through the completion of Phase 2 clinical trials. The Company will fund and retain control over the planned Phase 2 clinical trial of KVD001 as well as development of the investigational oral F-14 DME compounds through Phase 2 clinical trials unless Merck determines to exercise its options earlier, at which point Merck will take responsibility for all development and commercialization activities for the compounds. The Company’s development efforts under the Option Agreement are governed by a joint steering committee consisting of equal representatives from the Company and Merck. Under the terms of the Option Agreement, Merck paid a non-refundable upfront fee of $37 million to KalVista Limited in November 2017. If Merck exercises both options under the Option Agreement, KalVista Limited could receive up to an additional $715 million composed of option exercise payments and clinical, regulatory, and sales-based milestone payments. In addition, the Company is eligible for tiered royalties on global net sales ranging from midsingle digits to double digit percentages. Merck may terminate the Option Agreement at any time upon written notice to the Company. KalVista Limited may terminate the Option Agreement in the event of Merck’s material breach of the Option Agreement, subject to cure. Concurrent with the Option Agreement, the Company and Merck also entered into a stock purchase agreement (the “Stock Purchase Agreement”) pursuant to which Merck paid approximately $9.1 million to purchase 1,070,589 new shares of the Company’s common stock at a price of $8.50 per share.

Phase 2

KalVista plans to enroll 123 DME patients in a phase 2 trial that is currently enrolling. The trial will be a randomized, sham-controlled, double-masked study assessing the efficacy, safety, and tolerability of KVD001 in subjects with center-involving diabetic macular edema who have had prior anti-VEGF therapy. There will be three arms (high-dose and low-dose treatment arm; sham arm). Patients will receive 4 injections, either sham or treatment, within 3 months. The primary endpoint will be Best Corrected Visual Acuity at 16 weeks. Data is expected 2H 2019.

Market

Assuming a DME market of 800,000 patients with 33% of patients being non- or minimally-responsive to first-line treatment (anti-VEGF therapy), this nets an addressable market of ~ 267,000 patients.

Assuming a peak penetration of 15% (40,000 patients), $1500/injection ($3000/treatment)/month for an average of 1 year ($36,000), this nets ~ $1.4B in peak annual sales. Applying a 25% discount = ~ $1.1B. Applying a 3.5 multiple = $3.85B.

To assess for current value:

- 45% chance of Phase 2 success for ophthalmology drugs ($1.73B)

- 58% chance of Phase 3 success for ophthalmology drugs ($1B)

- 73% chance of ultimate NDA approval for Phase 3-completed ophthalmology drugs ($730M)

Coincidentally, this figure ($730M) is eerily similar to the amount of money Merck agreed to pay KalVista is they happen to exercise the option and drug development goes as planned.

What happens to the valuation if Phase 2 is successful in late 2019? We can then value KVD001 at $1.63B. In this event, it is very likely Merck would exercise the option and buy KVD001. Merck would then be responsible for all development costs associated with KVD001.

Furthermore, depending on KalVista’s enterprise value after phase 2 data, I believe there is a possibility of Merck acquiring KalVista in totality (which could, very well, be the cheaper option for Merck depending on their confidence in KVD001).

Valuation

In addition to the $48M KalVista reported as cash and cash equivalents for the quarter ending July 31, an additional $73M is expected after a September offering. With a cash burn of ~ $6M, we can anticipate KalVista having ~ $110M in cash and cash equivalents at writing. They have < $1M in debt.

KalVista’s market capitalization is ~ $250M. We can postulate that the market is valuing their entire pipeline to be ~ $150M. In light of KVD001 alone, I believe this is an undervaluation.

Recent insider buying, seemingly, agrees with my sentiment:

Source: OpenInsider

Summary

I believe, based on KVD001’s value, that KalVista should be valued in excess of $500M if phase 2 is successful. I believe, based upon preclinical evidence and phase 1 data, that it is probable KalVista will see success in phase 2. I believe, as a result, Merck will, at the least, purchase KVD001 per the option agreement.

Taking into account the likelihood of reasonable dilution between now and phase 2 data for KVD001, I will project a price target of $30/share to be reached within 12-18 months from now.

Peripherals

Pipeline

I may consider looking into KalVista’s HAE franchise if I am convicted it offers great value (like I believe their DME franchise does). In such event, I will write an article on HAE similar to this one. For now, my thesis and price target in KalVista rely solely on their intravitreal DME prospects.

Risks

Please read their annual filing to become familiar with all the risks associated with an investment in KalVista: 10K

Some of the specific risks to our investment thesis include:

- KVD001 may not be effective

- KVD001 may not be safe

- KVD001 may not be tolerable

- KVD001 may not be profitable in the unlikely event it hits the market due to a number of possibilities (competitive, tolerability issues, etc.)

- KalVista has a number of other programs that may fail or disappoint. This could cause share prices to suffer.

- Merck may terminate the option agreement completely. Investors may interpret this as bad and the share price may suffer.

Relevant News

Public offering – Sept., 2018

Option agreement with Merck – Oct., 2017

Competition

Improvements, in development, for anti-VEGF therapy (as mentioned earlier in the article) may serve as competition to KalVista (or Merck) simply because if anti-VEGFs become more effective for more patients, this would reduce the number of patients who would be eligible for second-line treatment.

Furthermore, Oxurion is also developing a PKal inhibitor for DME. They are a bit behind KalVista, as they expect phase 1 data in mid-2019. To my knowledge and according to KalVista’s annual filing, Oxurion is the only other company developing PKal inhibitor injections for DME.

Disclaimer: The intention of this article is to provide insight, not investment advice. While the information provided in this article is intended to be factual, there is no guarantee and prospect investors are encouraged to do their own fact-checking and research before investing in a company. One must also consider one’s own financial standings, risk tolerance, portfolio diversification, etc. before making a decision to buy shares in a company. Many of my articles detail biotechnology companies with little or no revenue. These stocks are, therefore, speculative and volatile. Even when prospects seem promising, there is no predicting the future. Losses incurred may be significant.

Disclaimer: The intention of this article is to provide insight, not investment advice. While the information provided in this article is intended to be factual, there is no guarantee and prospect investors are encouraged to do their own fact-checking and research before investing in a company. One must also consider one’s own financial standings, risk tolerance, portfolio diversification, etc. before making a decision to buy shares in a company. Many of my articles detail biotechnology companies with little or no revenue. These stocks are, therefore, speculative and volatile. Even when prospects seem promising, there is no predicting the future. Losses incurred may be significant.

Within The Formula, I present biotechnology companies that I believe have assets that are undervalued and provide therapeutic differentiation for diseases with limited treatment options. I typically look for stocks that present with at least 50% upside within 12-18 months. The above article is an example of the content that is readily available and accessible to marketplace subscribers.

Disclosure: I am/we are long KALV.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Be the first to comment