Editor’s note: Seeking Alpha is proud to welcome Tigron Park Energy as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to the SA PRO archive. Click here to find out more »

Situation Overview

Whiting USA Trust II (OTC:WHZT) is a classic cigar-butt investment with a potential catalyst for material upside. WHZT is a Net Profits Interest trust expected to terminate on December 31, 2021, after which no value will be received by the unitholders. The trust makes quarterly cash distributions and has a conventional asset base that produces ~3,000 boe/day (~80% oil) with relatively high operating costs per barrel, resulting in a significant leverage to oil prices for a ~$50m market cap trust with no debt.

WHZT data by YCharts

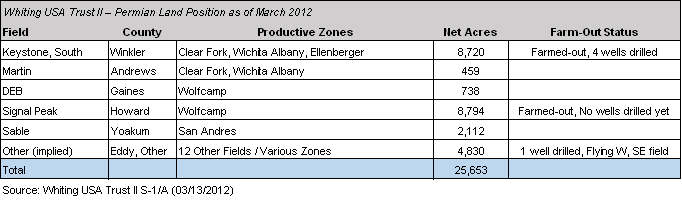

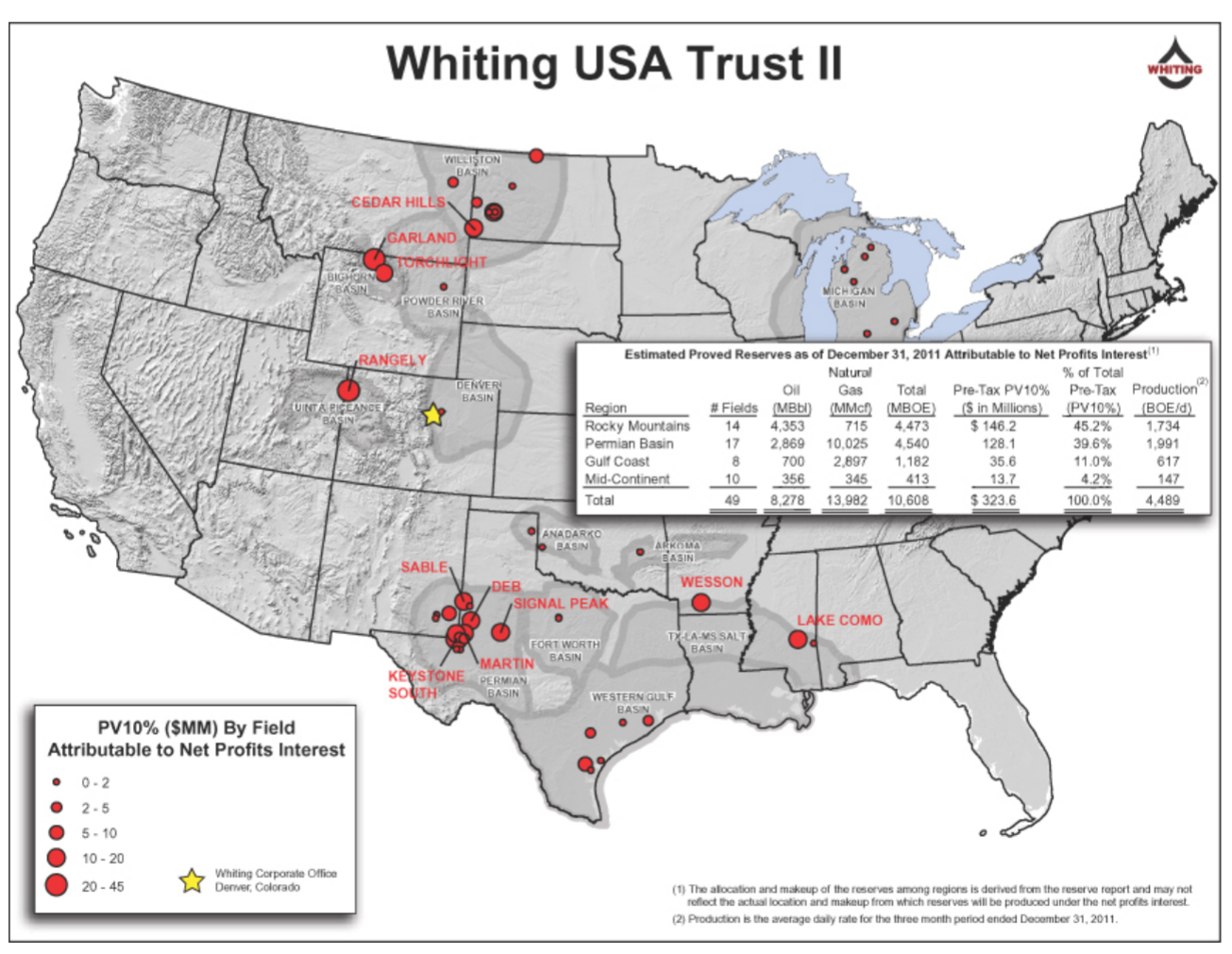

The purpose of this article is to discuss the possible hidden value in the trust’s land position. WHZT has an asset base that includes 22,692 net acres located in the Permian Basin. Much of this relates to the acreage around producing conventional oilfields conveyed to the trust. However, as time went by, some of this acreage has become prospects for popular horizontal shale plays. Whiting Petroleum (WLL) has the exclusive right to enter into farm-out agreements for trust acreage without the consent of the trustee or unitholders. Below is a breakdown of the company’s largest producing conventional fields and associated acreage at the time of the trust’s IPO:

Source: Whiting USA Trust II S-1/A (03/13/2012)

Current Farm-Out Agreements

In 2016, WLL entered into two farm-out agreements covering acreage in the trust. The first covering ~5,000 net acres in Winkler County, TX (Keystone South field) in the Central Basin Platform, and the second covering ~9,000 net acres in southeastern Howard County, TX (Signal Peak field) in the Midland Basin. Based on county records, it appears that that Basin Oil & Gas (“Basin”) is the farm-out partner in Winkler County, but has syndicated its investment out to several private equity investors. The terms of the farm-out seem to be industry standard in that the partner would cover 100% of well costs to retain a 75% working interest. One well would have to be drilled in each ~640 acre section of land in order for the partner to earn their working interest. WHZT would be free carried on this first group of wells. The trust would only receive a 10% carry on any additional wells drilled in the farm-out (meaning the trust would have to cover the remaining ~15% of costs to earn its 25% interest). To date, ~5 wells have been drilled across the farm-out acreage, resulting in $1.0-1.5m of incremental proceeds per quarter for unitholders.

In the Howard County, Basin appears to also be the farm-out partner. This farm-out has identical terms to the Winkler County farm-out, except it covers a larger tract of land and is situated in the Midland Basin where acreage costs and well costs are significantly higher than in the Central Basin Platform. To date, no wells have been drilled or permitted and the expiration date of the farm-out has been extended multiple times with seemingly no modification of terms. This acreage sits in the southeastern portion of the Howard County where drilling activity has started to heat up as operators like SM Energy (SM) have started to test the eastern boundaries of the Spraberry and Wolfcamp plays. If this farm-out were to move forward, it would require a significant capital outlay (Encana (NYSE:ECA) pegs its costs per well at $5.6m, though costs would likely be substantially higher for a smaller operator in the delineation phase).

Why Has There Been No Drilling Activity In The Howard County Farm-Out To Date?

One possibility is that Basin doesn’t believe in the quality of the acreage enough to make an investment. This is possible, but the continued extensions of the farm-out agreement seem to indicate continued interest. Also, why would WLL continue to offer additional optionality to Basin for nothing in return? Another possibility is that Basin and WLL both see that the acreage would be most valuable in a sale scenario, where it could be developed more rapidly and without restriction.

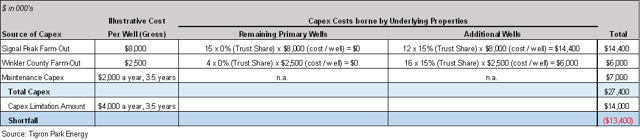

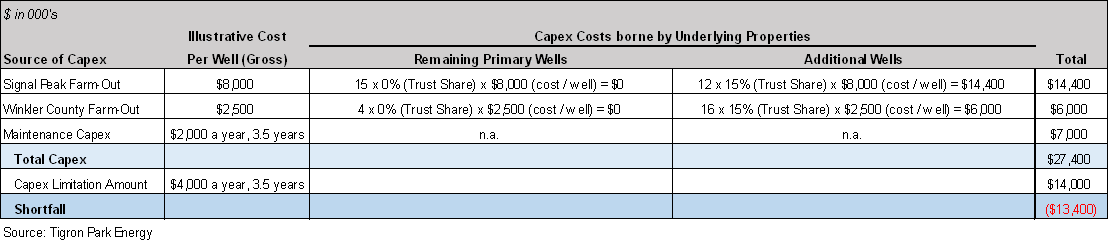

A possible piece of the puzzle is the Capital Expenditure Limitation Amount embedded in the WHZT trust agreement. The trust is restricted from incurring more than ~$4m per year of capex until expiration. Assuming $2m per year of conventional field maintenance capex, full participation under the Winkler County farm-out and Howard County well costs in the $8m area, there would be insufficient capital available for the trust to fund the additional wells. If the trust was unable to fund its share of costs, Basin could be hamstrung into waiting for the trust to expire to continue development.

Possible Sale Structure And Precedents

What if WLL could carve out and sell the land, providing some proceeds to unitholders today? Land in Howard County has routinely transacted in the range of $20,000-40,000 per acre. Assuming the low end of that range in a sale, the Howard County acreage would yield ~$200m of gross proceeds. If WLL were to try to execute a sale, unitholders would be entitled to a portion of the sale proceeds and would have to vote in favor of any proposed transaction. Given that there are about 3.25 years left in the trust and using a 15% discount rate, unitholders would be entitled to ~35% of the sale proceeds, or ~$4.00 per unit. In addition, the trust appears to hold other acreage in attractive areas that could also be monetized. A similar, carve-out and sale transaction was implemented just last year by Enduro Royalty Trust (NDRO).

One Possible Acquirer

Basin appears to be a relatively small private equity firm, evidenced by its choice to syndicate its interest in the Winkler County farm-out. Another possible piece of the puzzle is that Basin has recently engaged in a number of lease transactions in the Howard County with affiliates of HighPeak Energy (“HighPeak”).

The HighPeak and Basin management teams have worked together consistently in the past. In addition, HighPeak successfully launched a special purpose acquisition company, Pure Acquisition Corp. (PACQ), just a few months ago and is presumably looking to put capital to work. HighPeak has the knowledge of the area and has already permitted its first well in the Howard County. Given these facts, there is a reasonably good chance that PACQ will buy WHZT’s Howard County acreage in the near term.

Why Whiting Petroleum Might Be Supportive Of A Transaction

In this illustrative structure, WLL would receive 65% of the gross sale proceeds today – proceeds it could use to make accretive Bakken land acquisitions or to pay down debt and hit the leverage targets. Cash flow post-2021 or the opportunity to develop this relatively small block of Permian acreage internally would not be immensely beneficial to WLL, given its short-term leverage targets and scale in the Williston Basin.

Closing Thoughts

I believe that WHZT is an attractive cigar-butt investment opportunity with a possible asset-sale catalyst. While it is unclear if an asset sale will happen, a position in WHZT provides free exposure.

Disclosure: I am/we are long WHZT.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I am long WHZT and actively trade in it.

Be the first to comment