Gilead (GILD) reported better than expected Q2 results and has been making progress with its pipeline over the last couple of months. It looks like 2018 could be the bottom, and revenues might increase again next year. This, coupled with a promising outlook for some of Gilead’s pipeline candidates, could lead to improved market sentiment over the next couple of months. I believe that Gilead’s shares are not unattractive at the current level, at least for long-term focused investors.

The HIV Franchise Continues To Grow

Before the Q2 earnings report, I forecasted that Gilead would likely beat estimates again. This has come true, to an even bigger extent than I had estimated.

The much better than expected results were driven by strength in Gilead’s HIV franchise, which continues to grow at a compelling pace:

Source: Gilead presentation

Source: Gilead presentation

Gilead’s HIV franchise was established in the early 2000s, but despite the history of roughly one and a half decades, and an already quite large size, the franchise continues to grow at a double-digit pace.

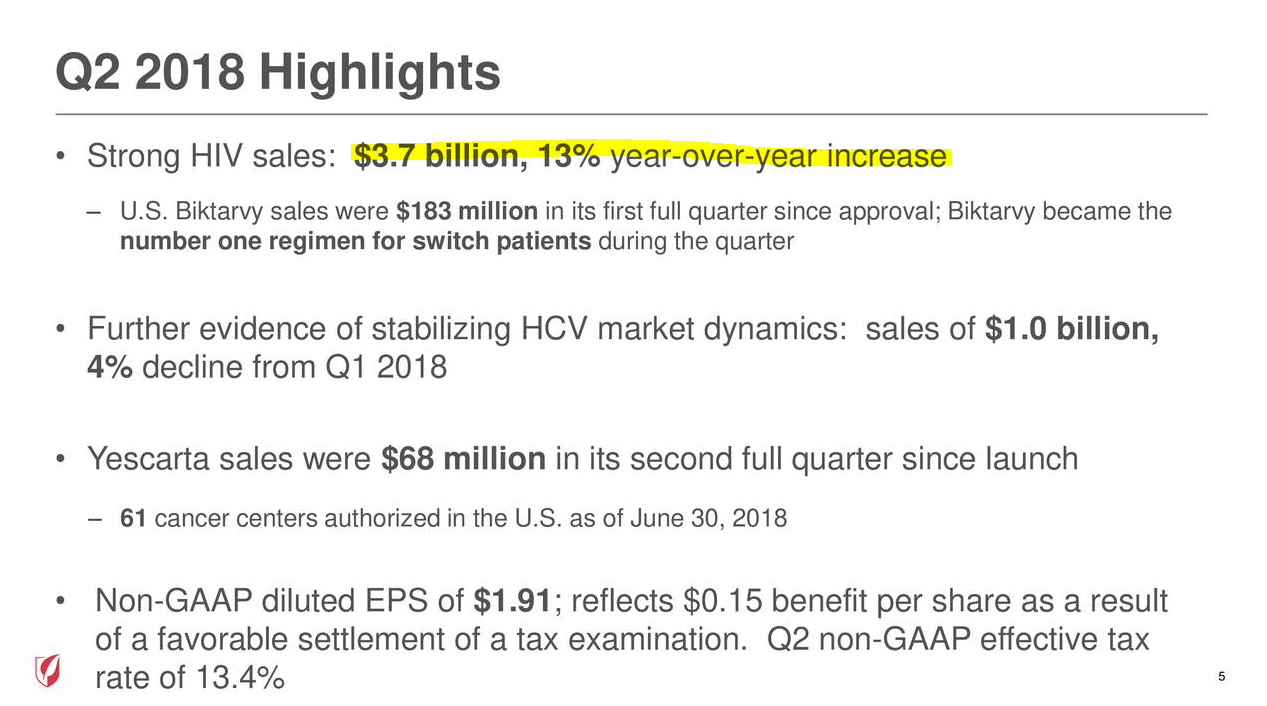

During Q2 Gilead managed to grow its HIV sales by 13% year over year, driven, at least partially, by the launch of Biktarvy in the US.

Source: Gilead presentation

Source: Gilead presentation

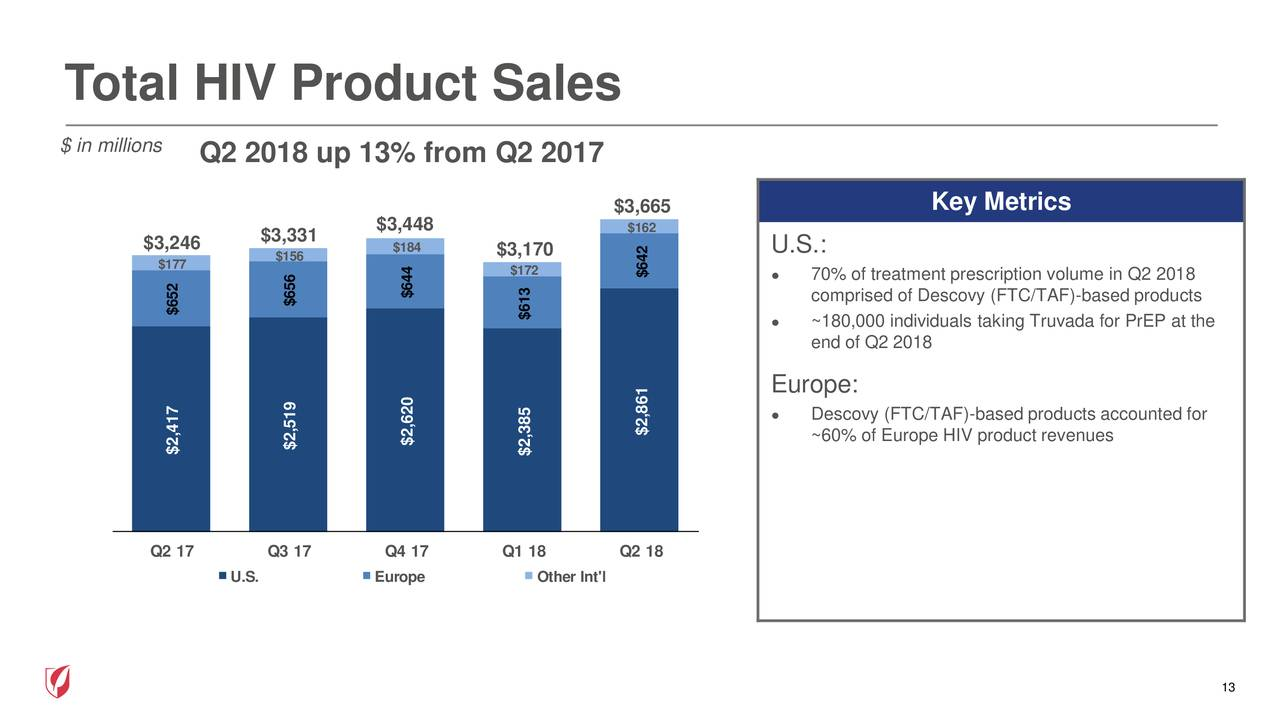

Q2 has been the best quarter for Gilead’s HIV franchise so far, sales surpassed the previous record quarter (Q4 2017) widely. Surprisingly sales for Gilead’s HIV franchise did only increase in the US, sales in Europe and in other International markets actually declined year over year. The decline in Europe was not severe (3% year over year), and from a much smaller basis compared to the market in the US, but nevertheless, it would have been better to see broad-based growth.

It is likely that HIV sales in Europe will improve going forward, though, as Biktarvy had not been rolled out during Q2 in the continent. Biktarvy received its marketing authorization in Europe at the end of June, so too late to influence Q2 results. Q3 and Q4 results should be positively impacted by the launch of Biktarvy in Europe, though.

It is likely that Biktarvy will generate meaningful sales in Europe going forward, as the single tablet regimen combines many positives:

Source: Gilead website

Source: Gilead website

It is possible that Q2 sales in Europe were lower due to patients & medical professionals waiting for the approval of Biktarvy, and therefore not renewing prescriptions of other HIV products, which led to lower sales for Gilead’s established drugs. Since the amount of people diagnosed with HIV continues to grow at a high pace in Europe, the overall market for HIV medications continues to grow as well. There thus are good reasons to assume that the small dent in Gilead’s European HIV sales was only temporary and that sales in the continent will rise going forward.

Declines In the HCV Market Are Getting Less Severe, Other Drugs Are Ramping Up

The primary cause for Gilead’s sales declines over the last couple of years was the decline in the company’s HCV sales. As Gilead’s HCV medication cures patients, sales for the drug were heavily front-loaded. The most severe cases are treated, and there is less need for HCV medication right now, which is why sales for Sovaldi, Harvoni & Co. have been declining.

Source: Gilead presentation

Source: Gilead presentation

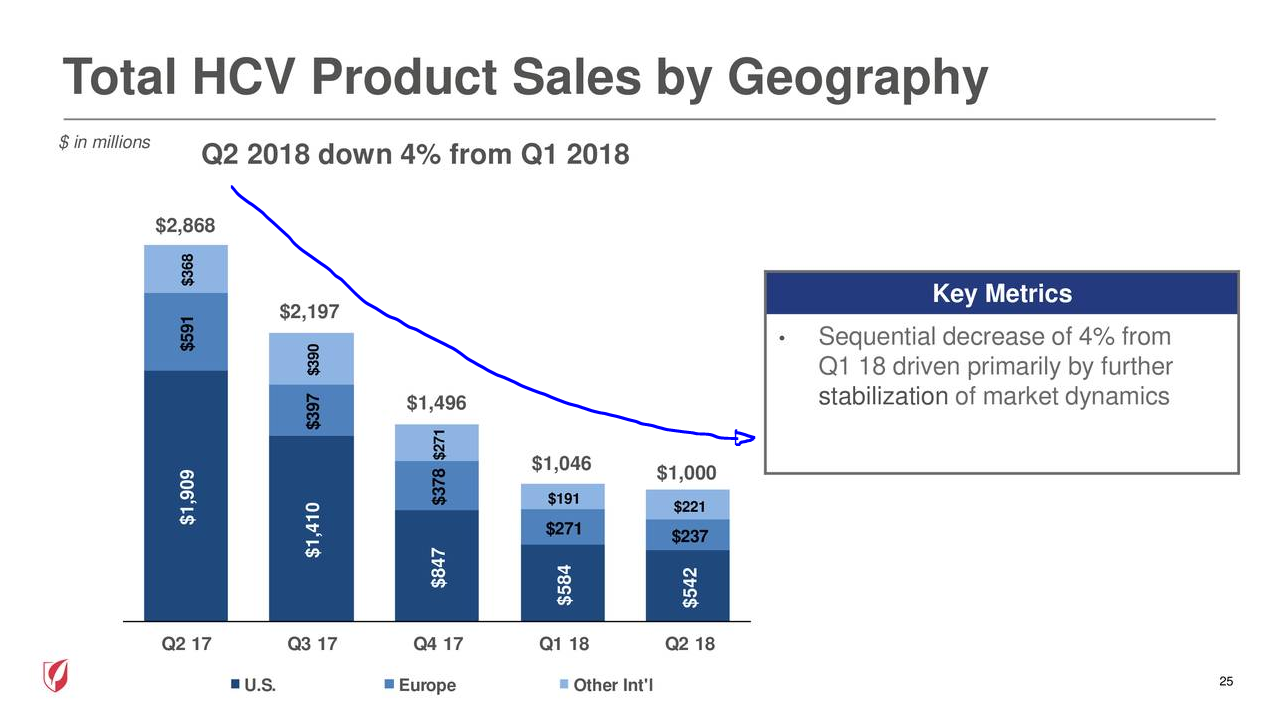

We see that Gilead’s HCV sales have been declining for each of the last quarters, but the declines have gotten less severe. From Q2 17 to Q3 17 the decline was $670 million, in the following quarters the declines were $700 million and $450 million. During the most recent quarter, however, sales declined by only $50 million — a big improvement from the decline rates in previous quarters.

If this trend persists, Gilead’s HCV sales would have more or less stabilized. Declining HCV sales would be a much less severe drag on Gilead’s top line compared to prior years and quarters, and Gilead would be much closer towards generating positive revenue growth on a year-over-year basis. The company has already achieved positive revenue growth on a quarter-to-quarter basis (Q1 to Q2).

Gilead will also profit from the ramp-up of Yescarta. This cell therapy has grossed $68 million in sales during Q2, an increase of ~70% quarter-to-quarter. The drug has received its marketing authorization in Europe in August, which means that sales of the drug can now ramp-up in this region as well. With the drug now being available in the two most relevant regions for drug sales, investors can expect that Yescarta’s sales will continue to increase at a substantial pace going forward. Analysts see Yescarta becoming a multi-billion dollar drug eventually, so we still are in the early innings regarding the growth trajectory of Gilead’s cell therapy.

Gilead should also be able to generate attractive sales numbers with some of its pipeline candidates, Filgoinib most likely being the most relevant one in the near term. A couple of days ago Gilead announced that the drug, which is developed with Galapagos NV (GLPG), has shown strong results in a phase III trial for the treatment of rheumatoid arthritis. Due to positive results, it is likely that the drug will receive approval for RA in the foreseeable future, approval in other indications is relatively likely as well. Since the RA market alone is worth $30 billion, even a relatively small market share can result in billions in annual sales in this indication alone. Other indications the drug is targeting, such as ulcerative colitis and Crohn’s, are possibly worth billions as well, so it is highly possible that Gilead will be able to generate several billions of dollars in annual revenues from Filgotinib a couple of years down the road.

Gilead’s Shares Are Inexpensive, And 2018 Could Be The Bottom

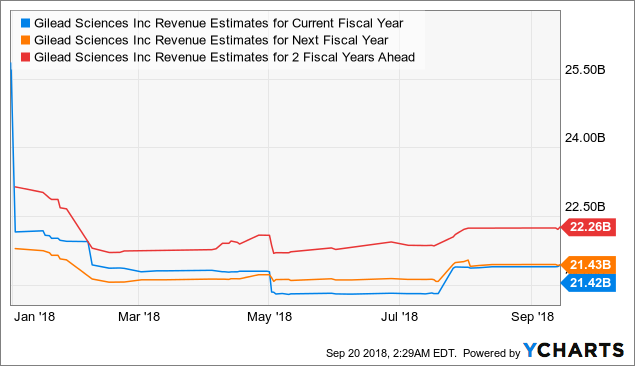

Over the last couple of years, Gilead’s sales and earnings kept declining due to the declines in the HCV franchise. Since those declines have gotten less severe, and since growth in HIV and the ramp-up of Yescarta influence Gilead’s sales positively, it is opportune to assume that 2019’s sales will be on par or higher than Gilead’s revenues during 2018.

GILD Revenue Estimates for Current Fiscal Year data by YCharts

GILD Revenue Estimates for Current Fiscal Year data by YCharts

The analyst community sees 2019’s revenues on par with revenues during the current year. This seems possible but could be too conservative if current trends (HCV sales stabilizing, HIV growing at a double-digit pace, and Yescarta ramping up successfully) persist going forward.

Gilead has earned $1.91 during Q2, which is equal to about $7.60 on an annual basis. Gilead, therefore, trades at slightly less than 10 times earnings right now. Such a valuation would be fair if Gilead stagnated forever, neither seeing growth nor declines. But since it is relatively foreseeable that Gilead will get back to growth in the foreseeable future the current valuation looks quite low.

It would not be surprising to see Gilead’s PE ratio expand to 12 or more once the market realizes that the nadir has passed and that things will improve going forward. There thus is substantial valuation expansion potential over the coming years.

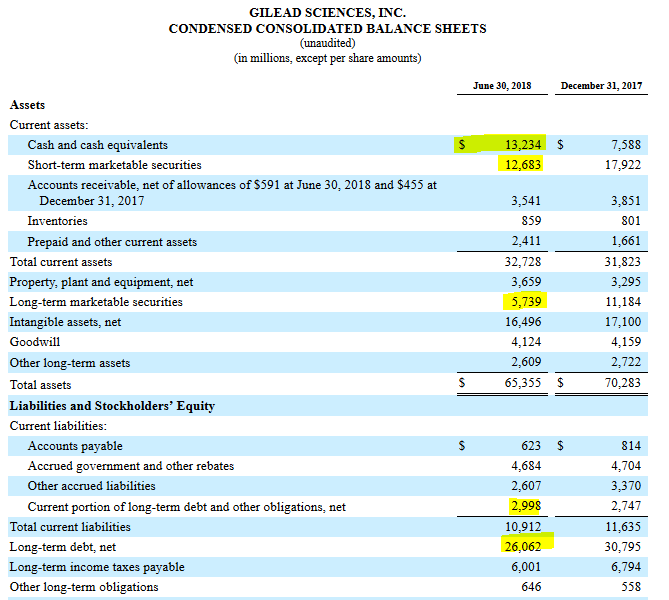

Gilead still has a strong balance sheet that allows the company to make more acquisitions as soon as management finds a valuable takeover target.

Source: Gilead’s 10-Q filing

Source: Gilead’s 10-Q filing

Gilead holds cash and equivalents of $31.6 billion, whereas debt totals $29.1 billion. Gilead, therefore, has a net cash position of $2.5 billion, which gives Gilead one of the strongest balance sheets in its industry.

Thanks to its strong cash flows ($3.3 billion in free cash flows during H1 2018) Gilead is easily able to finance its dividend payments ($3 billion a year) while having enough surplus cash flows to make acquisitions. Acquisitions such as Gilead’s takeover of Kita Pharma (Yescarta) could drive Gilead’s revenues up further over the coming years.

Risks To Consider

Biotech and pharma companies are under heavy scrutiny by regulators, governments, etc., and they repeatedly face the impact of losses of exclusivity. These risks are not specific to Gilead, though, but rather something investors should keep in mind regarding all investments into this industry.

Gilead is heavily reliant on its HIV business. Should a competitor come up with a superior product, or should someone find a cure for HIV, a majority of Gilead’s revenues would be on the line. Right now this risk seems quite low, as Gilead holds the majority of the HIV market due to the superiority of its products. It nevertheless is possible that Gilead’s HIV franchise does not maintain its cash cow in the long run.

Gilead repeatedly makes acquisitions in the multi-billion dollar range, such as the takeovers of Kita Pharma and Pharmasset. So far these acquisitions worked out well, as the drugs that were under development when Gilead bought these companies were successfully brought to the market later on (Sovaldi/Harvoni and Yescarta). It is, however, possible that Gilead makes an acquisition that does not play out so well in the future, which would weaken Gilead’s balance sheet and which would likely result in a negative share price reaction.

Final Thoughts

Sales trends for Gilead are improving on several fronts. HCV sales keep declining, but only at a relatively low pace, the franchise seemingly is stabilizing. On top of that Gilead’s HIV franchise is setting new sales records, while the ramp-up of Yescarta continues.

There are near-term positives, such as the approval of Yescarta and Biktarvy in Europe, and there are positives over the next couple of years as well, such as the likely approval of Filgotinib.

It is opportune to expect that sales will start growing again over the next two years, which could result in a rising valuation. Investors get paid a 3.1% dividend yield while waiting for things to improve. I believe that Gilead remains attractive for long-term focused investors.

Author’s note: If you enjoyed this article and would like to read more from me, you can hit the “Follow” button to get informed about new articles. I am always glad to see new followers!

Disclosure: I am/we are long GILD.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment