Overview of Investment Thesis

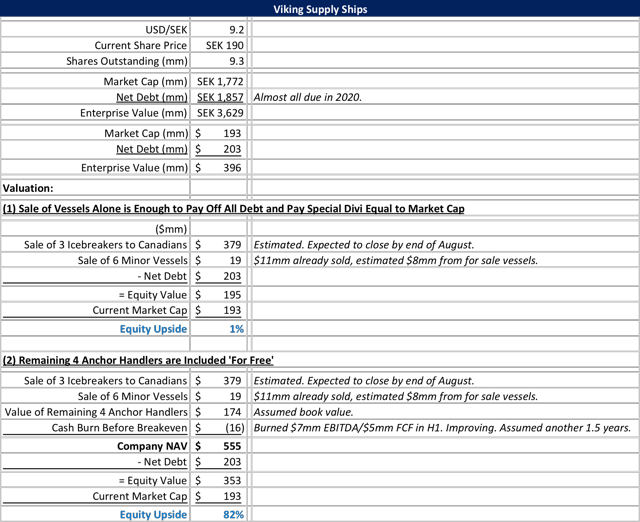

Viking Supply Ships AB, a company listed in Sweden (ticker: VSSAB-B), announced on Aug. 10 that they had sold 3 of their vessels. Our calculations suggest that the total sales price, which needs some estimation efforts, was likely ~$380mm. The company has net debt of $203mm and a recent market cap of $193mm, meaning that the cash from the sale is roughly equal to its Enterprise Value. If correct, Viking could repay all of the company’s outstanding debt and pay a special dividend equal to almost the entire market cap, if it chooses to be unlevered.

In addition, the Viking stub will still own 4 high quality vessels that are in total likely worth an estimated $175mm at replacement value, or 50% of that in the event of an immediate liquidation. On this basis, the stock has 45-80% potential upside, with limited downside risk in our view. Only 21% of the stock is floating, and retail investors appear to be cashing in on profits after a 715% rally, amid some confusion on Swedish retail investor forums as to what the sales price actually was. Viking’s market cap was just $27mm prior to the sale.

The remaining 79% of the company is owned by a Norwegian investment firm that reported, on Aug. 22, 2018, that they expect a special dividend when sale of the 3 vessels closes (at the end of Aug.). The announcement of a special dividend represents a hard catalyst that could drive 45-80% further upside for investors.

Company Background

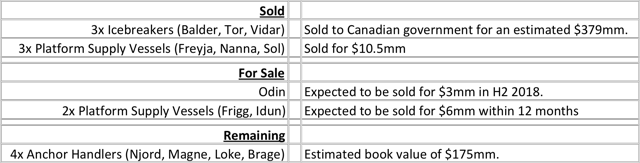

Viking owns a total of 13 vessels; 3 icebreaker vessels that it has just sold to the Canadian government, 4 high quality anchor handler vessels that will remain in its fleet, and 6 very minor vessels that are either sold or expected to be sold in the next 12 months.

For the sale or expected sale of the 6 minor vessels, we estimate the proceeds will be $19mm in total. Once all sales are completed, Viking will have just the 4 anchor handler vessels remaining.

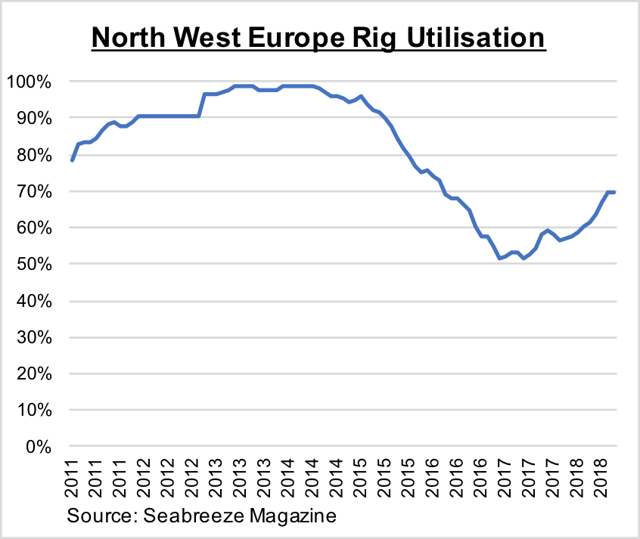

The 4 anchor handlers that will remain are vessels in the North Sea primarily used to tow offshore oil rigs. The North Sea market consists of ~75 anchor handlers, of which ~35 are in layup after arguably the worst downturn in its history (source: Westshore Shipbrokers – Home Page). The industry is highly cyclical and ultimately driven by confidence in future oil prices, which drive the capex of oil companies and the demand for rigs and vessels. The market is now clearly recovering (see Appendix: The North Sea PSV Market), with day-rates bottoming in early 2018.

The company is 79% owned by the Norwegian industrialist Christen Sveaas’s investment firm Kistefos, which invests across financial services, TMT, real estate, and venture capital and has a history of funding this through dividends and exits from their companies. Viking paid out a special dividend when it last sold a subsidiary in 2015.

The recent vessel sales mark a complete turnaround for the company that appeared to be at risk of bankruptcy. Viking had only $9mm of cash remaining, burned through $4mm of cash in H1, and had most of its vessels in layup (including the 3 sold).

The Vessel Sale Proceeds Cover Viking’s Current Enterprise Value

Viking announced on Aug. 10 that it had sold 3 of its vessels to the Canadian government for $274mm above book value. We estimate that book value for these 3 vessels stood at ~$105mm (see calculations below), implying a total price of ~$379mm, with Nordic brokers (Arctic, Carnegie, and Pareto) estimating a price range of $360-390mm. With Viking’s share price languishing below SEK 25.00 prior to the announcement (versus SEK ~190 today), the sales price at ~3.3x book value certainly caught the market by surprise. The scenario was likely only possible due to an urgent shortage of ice-breaking vessels for the Canadian coastguard, and the fact these vessels take several years to build.

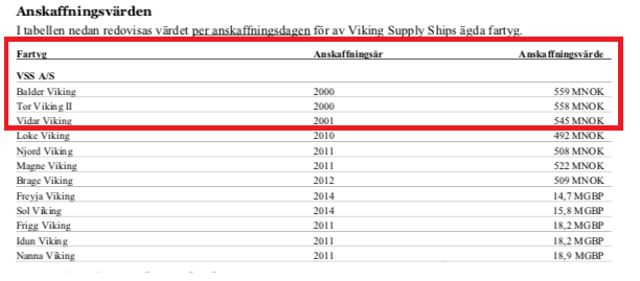

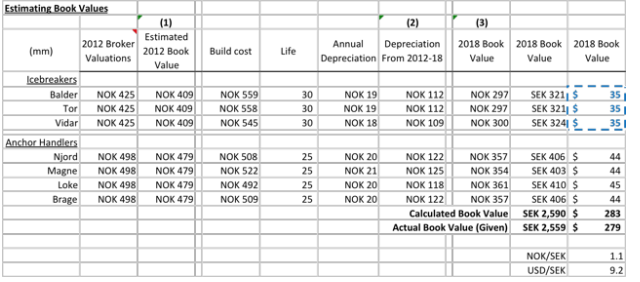

The 3 vessels sold (the Balder, Tor, and Vidar) were built in 2000-2001 for a cost of NOK 545-559mm (Source: Nov. 11, 2017 prospectus p.41).

We estimate their combined (Balder, Tor, Vidar) book value stood at $105mm.

The company’s policy is to depreciate the cost of vessels over 25-30 years (on a Straight-Line basis, per page 48 of the 2017 Annual Report), add the cost of additional repairs and modifications while allowing room to reclassify values upwards or impair downwards if management feel it is appropriate. The company’s book values have historically closely followed independent appraisal estimates. In Q2 of 2018, the company revealed that the book value of all vessels combined was only 4% below broker estimates (pg. 14), while in 2012 they stated that “the value of the Group’s vessels was determined with the help of external appraisers and internal impairment tests”.

Interestingly, in 2012 these appraisers also revealed their estimates for each vessel individually (Source: June 25, 2012, listing document p.23). These appraisals valued the 3 icebreakers at NOK 425mm each.

Reducing this value by 4% leads to a value of NOK 409mm each. Assuming a vessel life of 30 years, which the company has confirmed, and a straight-line depreciation policy, we estimate that the vessels incurred NOK 109-112mm of depreciation from 2012 to 2018. Subtracting this estimate depreciation from the estimated 2012 book value results in a 2018 book value estimate of NOK 297-300mm per vessel, or $35mm each for a total book value estimate of $105mm.

Note that this book value calculation does not include the added value of any repairs or reclassifications.

Based on our book value estimate of $105mm, a sales price $274mm above book value implies a total sale of $379mm.

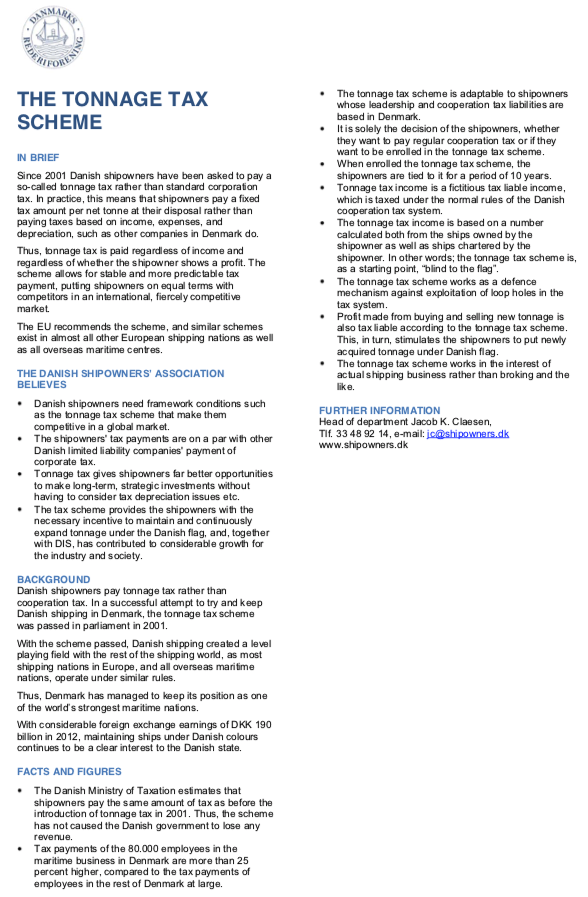

We spoke with Viking’s CFO twice in mid-August, and management have confirmed to us that Danish law means that Viking will not pay tax on the sales of these vessels because they are protected by the Danish tonnage tax scheme. This scheme taxes companies based on the net tonnage of the ships operated rather than by profits. The scheme specifically states that “Profit made from buying and selling new tonnage is also tax liable according to the tonnage tax scheme. This, in turn, stimulates the shipowners to put newly acquired tonnage under Danish flag.” (see Appendix: Danish Tonnage Tax Scheme). While it may seem strange that taxes for shipowners are low, shipping has a history of very low taxes since the assets are mobile. Countries like Denmark have introduced schemes to remain competitive with offshore tax havens.

Viking’s stock has rallied 715%, taking the market cap to $193mm and EV to $380mm. The cash from these sales alone is enough to pay off all the company’s debts and also issue a very large special dividend, potentially approaching an amount equal to the market cap.

The risk of the sale to Canada falling apart is very low, as the vessels are already on their way to Canada, with an expected arrival this week. The deal is expected to close by the end of Aug. (with Canada likely to make payment before the end of Q3), with no regulatory concerns.

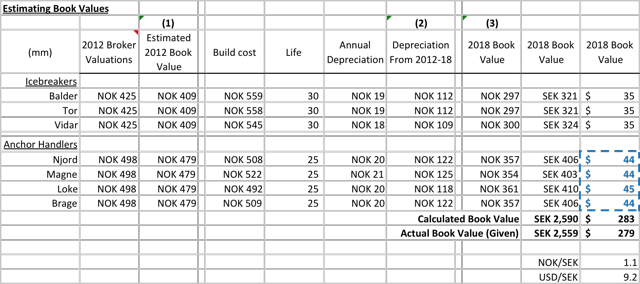

The Remaining Vessels

The 4 remaining vessels are good vessels: only 6-7 years old, have good engines, and are in the top 2 ice classes typically desired of anchor handlers. The standard valuation approach to these vessels is to estimate their replacement cost by taking the original build cost, add repair/upgrade costs and depreciate for age. That is exactly the approach that Viking has taken to calculate the book value of the 4 vessels on the balance sheet, which we estimate comes to ~$175mm for the 4 in total. This implies a value per vessel of $44mm, versus an estimated new build cost of ~$70m.

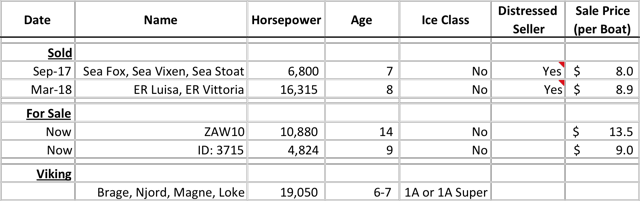

While replacement value reflects intrinsic value, the market is highly cyclical, with transaction prices significant below this at the trough and above it at peak. The North Sea market is currently coming out of the worst downturn since the 1980s, and the 2nd hand market remains illiquid. Our observations of second-hand transactions suggest that if Viking were to seek an immediate sale, they would likely only receive 50% of replacement value, or $88mm in total.

Basing estimates on second-hand market sales is difficult because most vessels sold tend to be low quality and from distressed sellers. However, the below table on comparable sales offers some support:

Sea Fox, Sea Vixen, and Sea Stoat were sold by Deep Sea Supply in September 2017, while the company was restructuring its debt. These vessels were sold for $8mm each when their book value was $7.5mm. In comparison, Viking’s vessels have 2.8x the horsepower and are Ice-class. Multiplying the sales price of $8mm by 2.8x difference in horsepower gets to a back of the envelope sales price for Viking of $22mm without taking into account the Ice-class and the fact that Viking is not a distressed seller (the ER vessels were sold in an even more distressed scenario as the company forced by creditors to liquidate the entire fleet). This supports the claim that Viking should be able to fetch half of book value (also $22mm) if they were to immediately liquidate these 4 anchor handlers.

It’s worth noting that the investment firm, Kistefos, lists in a May 2018 presentation that it internally values Viking on “vessel broker values relative to book values”, which suggests it estimates the value of the 4 vessels at the $175mm (plus 4%) rather than $88mm.

The Market Mispricing

Prior to the Canadian deal, Viking was just a $27mm market cap company with only 21% floating. The stock’s traded volume was only ~$10k a day and the free float was owned by retail investors or made up of tiny positions for institutions. The stock was/is so inefficient that it ‘only’ rose 13% in the remaining trading on the Friday afternoon of Aug. 10 after Viking issued a press release announcing the sale. The stock then opened up ‘only’ 42% on Monday, Aug. 13, before rising throughout the day to finish up 291%. Recent stock action suggests that many investors are choosing to take profits after a 715% gain.

One of the challenges likely confronting investors’ analysis is the fact that the company did not directly reveal the sales price or the book value of the vessels, but only the gain above book value of $274mm. When we look at Swedish retail investor forums, there appears to be confusion as to what the sales price actually was. It seems unlikely that this confusion will last for long.

In fact, the stock also did not react to reports in the Canadian media throughout June and July that the Canadian government had provisionally awarded a ~$470mm contract (CAD $610mm) to a shipyard to purchase and refurbish Viking’s 3 icebreakers, with purchase price of the vessels themselves likely to make up the bulk of the $470mm.

Catalyst for Additional Stock Upside: Special Dividend

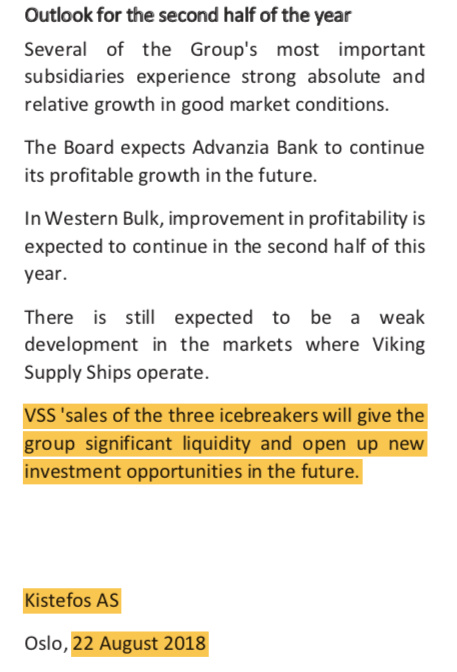

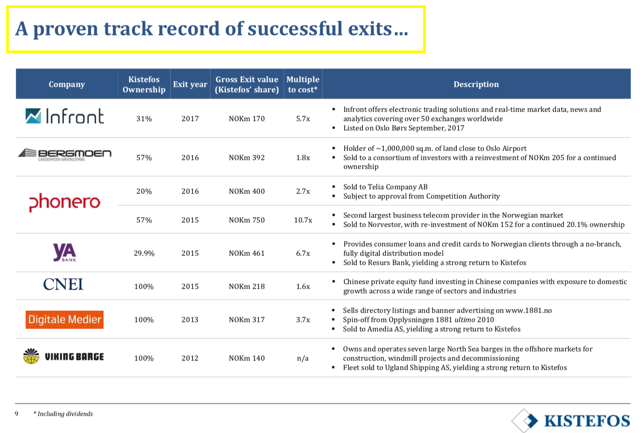

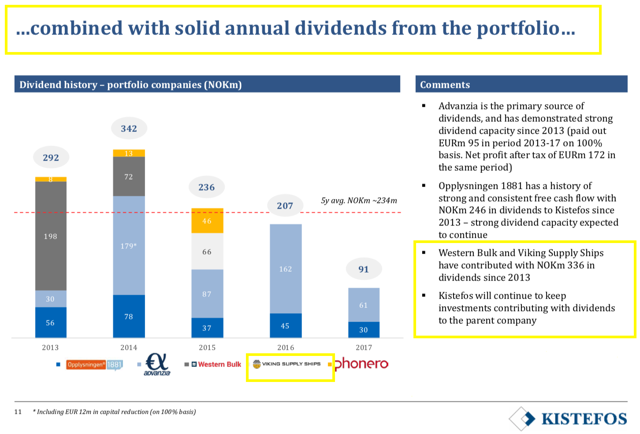

With the Canadian sale expected to be complete at the end of Aug., we expect Viking to announce a special dividend. The company is 79% owned by the investment firm Kistefos, which wrote in a May 2018 presentation that it has “a proven track record of successful exits… combined with solid annual dividends from the portfolio” (See Appendix: Ownership). It then wrote in its Aug. 22 report that “VSS ‘sales of the three icebreakers will give the group significant liquidity and open up new investment opportunities in the future.”

Source: See “Half Year Reports” at Financials | Kistefos

We spoke with Kistefos on Aug. 22nd, where they confirmed that this wording refers to new investment opportunities within Kistefos, not Viking. Kistefos has various businesses it could redeploy capital across, including financial services, TMT, real estate, and venture capital. Viking also issued a special dividend in 2015 after the sale of a subsidiary.

Debt Limit and Possible Special Dividend Value

Due to its existing agreements with banks following a restructuring earlier this year, Viking is obligated to reduce its debt following the sale. It currently has an LTV of 75% and creditors have historically allowed it to issue debt at 60%. Assuming that the Viking stub would be required to have an even lower LTV of 50% equates to an ability to carry $88mm of debt (the $175mm book value of the 4 anchor handlers x 50%). The company currently carries $211mm of debt, meaning that it would have to repay $123mm from the vessel sales proceeds. With a sales price to the Canadians of an estimated $379mm, this gives Viking the ability to pay out up to $256mm ($379mm – $123mm) in special dividends, or SEK 251/shr. That number represents 132% of the current share price. (See Appendix: Size of Potential Special Dividend)

Risks

-

Cash is not paid out in a dividend. The biggest risk is that Kistefos decided to keep the cash in Viking and spend it on something value-destructive, which is easy to do in the offshore energy industry. In our opinion, this risk is mitigated by Kistefos’ published commentary on Aug. 22 (From the H1 report) which ended with the phrase “VSS ‘sales of the three icebreakers will give the group significant liquidity and open up new investment opportunities in the future.” Christen Sveaas – who owns 100% of Kistefos, also has a net worth likely to be ~$700mm – so paying out a large dividend would be of significant interest to him.

-

The sales price of the Canadian deal is less than our estimate of $379mm. This is possible since the company did not reveal the sales price or the book value of the vessels sold. However, even the lowest broker estimate of $360mm implies an equity upside of 35-70%.

-

Fall in oil prices. This is usually the biggest risk for offshore energy companies, but the risk is low in this case, given an expected catalyst/time horizon of a few weeks.

-

Low liquidity. Viking Supply Ships’ stock is not listed in North America and suffers from weak trading liquidity in Sweden. The stock has historically traded only ~$10k a day, despite the fact that volume has jumped as high as $47mm on the Monday after the Canadian deal announcement and may be elevated for a while following the announcement of a special dividend. Liquidity will likely remain low for the stub.

Conclusion

Although Viking’s shares are up a massive 715%, a Sum-Of-The-Parts analysis, anchored by our estimated total sales price for the icebreaker vessels sale, suggests that the stock still offers up to ~80% potential upside and limited downside risk. The expected special dividend announcement is a hard catalyst in the near term, making the IRR appear very attractive here.

This opportunity largely exists because Viking’s retail investor base is still digesting the news of the sale, and are understandably happy to take profits after the price rise. As other analysts perform their research and calculations, Viking’s remaining undervaluation may not sustain itself for very long.

Appendix

Danish Tonnage Tax Scheme

Management have confirmed that they do not expect to pay tax on the sale due to the Danish tonnage tax scheme:

Ownership

79% of Viking’s shares are owned by the Norwegian Christen Sveaas’s investment firm Kistefos. Sveaas owns 100% of Kistefos and is likely to worth somewhere around $700mm. A Norwegian equivalent of Forbes magazine – Kapital – listed his net worth at NOK 5bn ($600mm) in 2017. (Source: KapitalIndeks | Kapital. Taking into account the ~$150mm increase in market cap by Viking since then and the fact that Sveaas owns 79% suggests his net worth is now ~$700mm.

Sveaas first acquired Viking in 1989 and initiated a major expansion in their platform supply vessel fleet. Through several acquisitions and mergers, by 2013, Viking was one of two subsidiaries. The other subsidiary was called TransAtlantic and was a persistently loss-making shipping and logistics company. Sveaas owned 63% of the company at the end of 2014.

Since 2014, Sveaas has been selling off or closing down the business:

-

In 2015, the majority of the TransAtlantic was sold and a dividend of SEK 98mm was paid out. The remaining operations were discontinued or sold off over the course of 2016-17.

-

The company had 5 offices, but shut down the UK one in 2015, Canada in 2016, and Denmark in 2018. Only the Norwegian headquarters and Russian office remains.

-

The company announced they intended to sell all 5 platform supply vessels in Q2 2018. 3 have had deals agreed and the other 2 are expected to be sold in H2 2018.

-

On Aug. 10, 2018, the company announced that its 3 icebreakers would be sold to the Canadian government.

-

Only the 4 anchor handler vessels remain.

The above moves suggest that Sveaas will not be keen to keep the $379mm proceeds from the Canada sale in the company. His investment firm, Kistefos writes in a May 2018 presentation that it has “a proven track record of successful exits” and “solid annual dividends from the portfolio”:

Sources: Kistefos – Company update

Kistefos also published its H1 2018 report on Aug. 22, which ended with:

Source: See “Half Year Reports” at Financials | Kistefos

Size of Potential Special Dividend

As mentioned, we estimate that Viking could pay out a special dividend of up to SEK 251/shr, or 132% of the current share price after the Canadian sale.

Viking’s creditors calculate its loan-to-value using the book value of its vessels. Today, the company has $211mm of debt and a vessel book value of $279mm, giving it an LTV of 75%. Historically, the company has been able to issue further debt up to an LTV of ~60%. Assuming that creditors would now demand a lower LTV – perhaps 50% – if the company was only to have 4 anchor handlers remaining suggests that the Viking stub will be able to carry $88mm of debt (the $175mm book value of the 4 vessels x 50%). The company currently carries $211mm of debt, meaning it would have to repay $123mm. With a sales price to the Canadians of an estimated $379mm, this give the company the ability to pay out up to $379mm – $123mm = $256mm in special dividends, or SEK 251/shr. That represents 132% of current share price.

It is also important to note that the company has confirmed that it does not expect to pay any tax on the Canadian sale. This is because the 3 icebreakers are held in a Danish subsidiary, which operates under Danish tonnage tax law. This law states that companies pay tax based on the net tonnage of the ships operated rather than by the profits earned from such operations. The company pointed out that it has also previously paid special dividends without any tax complications.

Share Price Reaction to the Announced Vessel Sale

The stock did not move in June or July despite several important announcements:

The Canadian government announced on June 22 that it had awarded the shipyard Chantier Davie an Advance Contract Award Notice (ACAN) to convert the 3 Viking vessels. (Source: ARCHIVED Class of three AHTS Icebreakers (F7013-180009/A) – Buyandsell.gc.ca).

“An ACAN is a public notice indicating to the supplier community that a department or agency intends to award a contract for goods, services or construction to a pre-identified supplier, thereby allowing other suppliers to signal their interest in bidding, by submitting a statement of capabilities. If no supplier submits a statement of capabilities that meets the requirements set out in the ACAN, on or before the closing date stated in the ACAN, the contracting officer may then proceed with the award to the pre-identified supplier.”

This was reported by Canadian media on the day with an estimated project cost of just under $500mm to both purchase and do work on the vessels. Example: Ottawa makes deal to buy three icebreakers for coast guard | CBC News

While the allocation of the $500mm to the purchase price vs repairs was not stated, the shipyard pitching for the project has written in their pitch that the “vessels only require minimal alteration or re-configuration to the topsides (not hull or propulsion) to fully meet the needs of the Canadian Coast Guard.” Canadian media further reported that 1 of the 3 vessels would be available almost immediately, while the other 2 would be available in 1 year’s time. This again suggested that the cost of purchasing the vessels themselves would make up the bulk of the estimated $500mm contract price.

(Shipyard presentation)

Viking confirmed the sale on a Friday afternoon (Aug. 10), but stock ‘only’ rose 13%:

The stock then opened up ‘only’ 42% on Monday, Aug. 13, before rising throughout the day to finish up 291%. The stock has since had significant up and down says, suggesting that investors are choosing to take profits after a 715% gain.

The North Sea PSV Market

The North Sea has been a market for offshore oil for nearly a century. Numerous oil companies operate in the region, most notably the majors like Statoil, BP (NYSE:BP), and Shell (NYSE:RDS.A), but also many others. The market for supply vessels is split into two: anchor handlers (AHTS) that primarily tow offshore rigs, and platform supply vessels (PSV) that carry cargo to rigs from the shore.

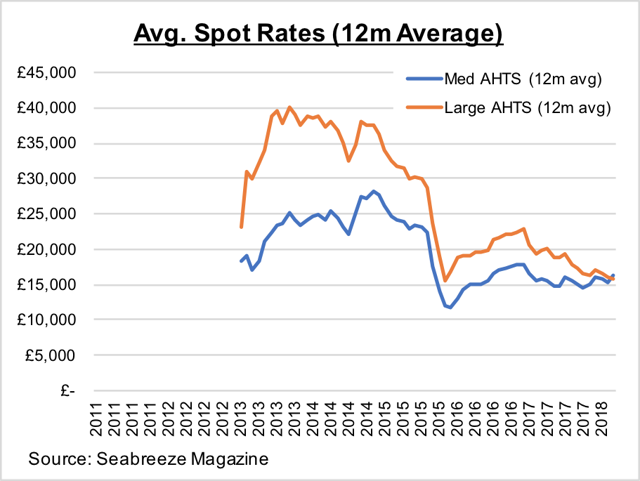

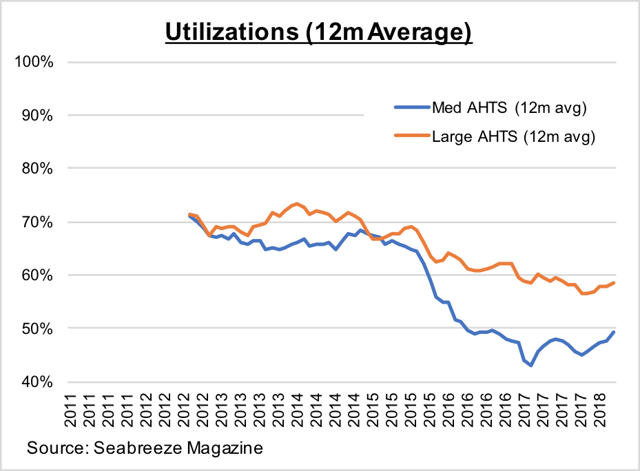

The unit economics are fairly simple: companies order vessels from ship builders typically years in advance of delivery and lease them to oil companies typically on contracts of 1-12 months. There is also a spot market that is used particularly often when demand for vessels for a long period is low (like now). While the opex of hiring a captain and crew tend to be relatively stable, the day rates paid by oil companies tends to vary greatly over the course of a cycle. Utilization of vessels is also very important. This can be as high as 90% for the industry at peak cycle, and 30% at trough cycle as ships get put into lay-up:

Ships usually last for 20-30 years. Replacement values are typically determined by the cost and depreciation as they age, but the cyclicality of the industry means that companies end up ordering vessels at the top of the cycle, and so vessels often earn lower than normal FCFs in their initial years which means that their PV ends up being below the cost of construction.

The market consists of many players and barriers to entry are extremely low: it is easy to rent a boat and hire and captain and crew. The biggest players tend to be Norwegian or US companies. On the Norwegian side, these include Solstad/Farstad/Deep Sea Supply (recently merged), DOF, Havila, Eidesvik and many others. On the US side these include Tidewater, Hornbeck, Gulfmark, and SEACOR Marine.

There are ~75 anchor handlers in the market, of which ~35 are in layup, and there are ~130 PSVs in the market, of which ~65 are currently in layup. More vessels could come from other markets as conditions improve. The live status of all vessels can be tracked at Westshore Shipbrokers – Home Page, with live locations here.

All our sources stated that the current downturn in the North Sea has been worse than 2008 and potentially the worst ever. This has been because (1) the oil price did not recover quickly, (2) companies made large vessel orders right at the top of the cycle, and (3) most/all companies entered the downturn highly levered. As a result, almost all companies have been through some form of bankruptcy or restructuring. As one source summarized, the North Sea had a “near death experience”.

As costs fall and oil rises from $30 to $75, it is clear that the cycle has turned. As several sources said, if oil remains at $60-90 then oil companies will have the confidence to invest in project, which translates into higher activity and demand for vessels. The upturn in rig utilization has already begun:

A key source of speculation is how many ships in layup will come back to the market. The supply vessel companies say that only 40-50% will, whereas the shipbrokers estimate that 70-80% will. The vessels that will struggle to come back are the older and smaller ones. There are two main reasons for this: First, given the oversupply of boats oil companies can be picky in the ones they choose. Second, as offshore drilling moves increasingly to deeper and harsher waters, higher quality boats are required. Boats over 10 years old are unlikely to come back.

As the market turns, so too does the value of the vessels. However, given the number of vessels in layup, it is unlikely that the increased theoretical value of the vessels can be realized immediately through asset sales. Instead, they will initially be realized through higher day rates that translate into higher cash flows.

Important Disclosures

Note: The author is a principal of Plural Investing LLC (“Plural”). As of the publication of this report (the “Report”), the author, Plural, its affiliates, and/or its principals (the “Plural Parties”) currently maintain an investment in Viking Supply Ships AB (the “Company”) and stand to realize gains in the event that the price of the Company’s stock rises. For this reason, the opinions expressed in this Report should not be considered independent. Following the publication of this Report, the Plural Parties expect to transact in the Company’s securities covered in the Report and may increase or decrease investment in such securities.

This material is for informational purposes only, does not constitute an offer or solicitation to buy or sell securities, and no specific recommendations are intended. The Plural Parties reserve the right to transact securities in a manner inconsistent with the views expressed herein and, furthermore, disclaim any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: ((i)) reliance on any information contained in the analysis; ((ii)) any error, omission or inaccuracy in any such information; or ((iii)) any action resulting therefrom.

Selective citations of, or quotations from, this document may be made under “fair use” laws, provided publication includes an appropriate reference to Plural and a link to Plural’s web site, at www.pluralinvesting.com. No reproduction of the whole report, or large sections of it, including graphics, is permitted without written permission from Plural.

Disclosure: I am/we are long VIKING SUPPLY SHIPS (VSSAB B).

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment