Unilever (UL, UN) shares are falling today after a disappointing Nielsen report indicating that the company has continued to lose market share:

The company is currently looking to move its global headquarters to the Netherlands – opting for Rotterdam over London – which could cause more selling pressure than today’s update on market share, however. Part of its decision revolved around a plan by the Dutch to scrap the withholding tax on dividends – something that simply doesn’t exist in Britain currently. The move has many implications, and some don’t want it to happen at all.

Backlash and a “plan B”

The ninth-largest holder of Unilever, the asset management arm of insurer Aviva (OTCPK:AVVIY) doesn’t want the company to move at all, apparently planning to vote against it. Unilever also has to convince 75% of UK shareholders and 50% of Dutch shareholders for the proposal to pass, so it’s not 100% guaranteed that it ends up being a Dutch company.

As a US investor, I like the fact that my UL shares are British, because I don’t pay any foreign taxes on my dividends due to a tax treaty between the US and the UK. Moving to the Netherlands changes that, especially if the country doesn’t scrap the dividend tax.

That’s not too big of a deal for me, since I hold shares in a taxable account (so I can hopefully reclaim any money lost from the Dutch dividend tax), but I can see how people holding it in a retirement account (where taxes can’t be reclaimed) would be angry with the move. Many people might sell their shares if the company does successfully move and the Dutch decide to retain the dividend tax, in my opinion, putting selling pressure on shares without valuations being taken into account.

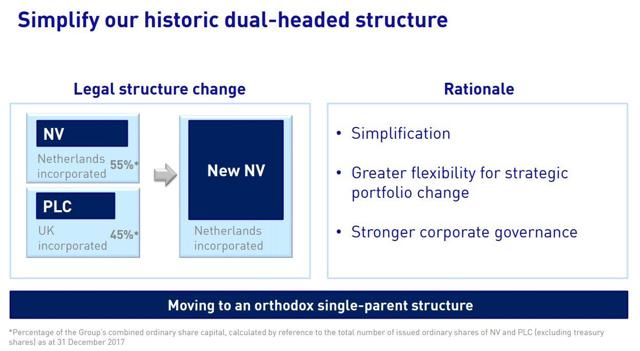

If the move is successful, the new share structure will look as shown in the below graphic:

Source: Unilever FH2018 presentation

If the company does manage to convince shareholders to approve the move and the Dutch keep the dividend tax, Unilever has a “plan B” as well. The backup plan was likely introduced in an effort to appease British shareholders who wouldn’t welcome a new 15% withholding tax warmly. Unilever plans to utilize a “substitution payment mechanism” in which it distributes capital in a way that doesn’t trigger the new tax.

According to Reuters, a recent poll showed that only 11% of voters support scrapping the tax, indicating that getting rid of it could be an uphill battle, so it makes sense that Unilever is exploring different options. Either way, looking at everything from the difficulty of scrapping the dividend tax to what appears to be major backlash from British investors, it appears that the company’s headquarters relocation isn’t necessarily guaranteed.

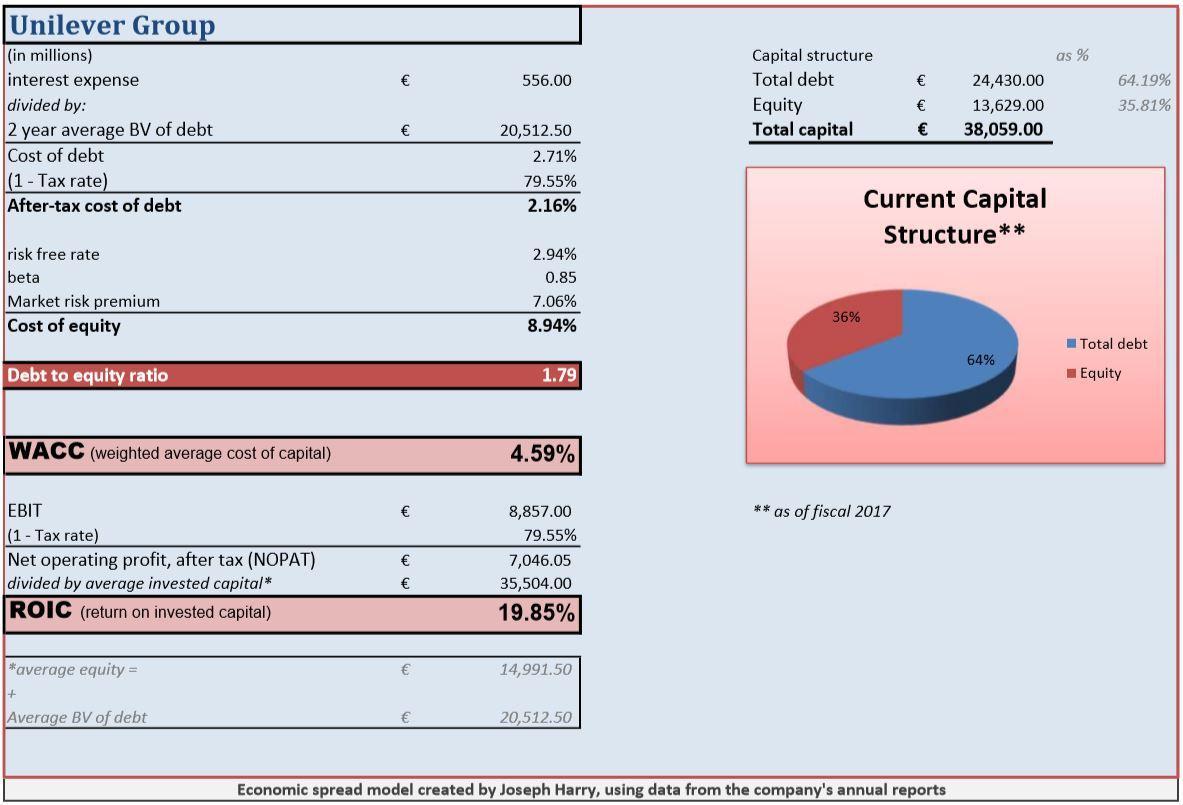

Return on invested capital analysis

Unilever is an above-average company, one that I’d call “best in class”. It earns ROIC of close to 20%, far in excess of its likely cost of capital:

The company’s strong brand portfolio, size and scale, and emerging markets exposure give it ample growth opportunities as well, and due to its ability to out-earn its cost of capital, this growth is also highly profitable.

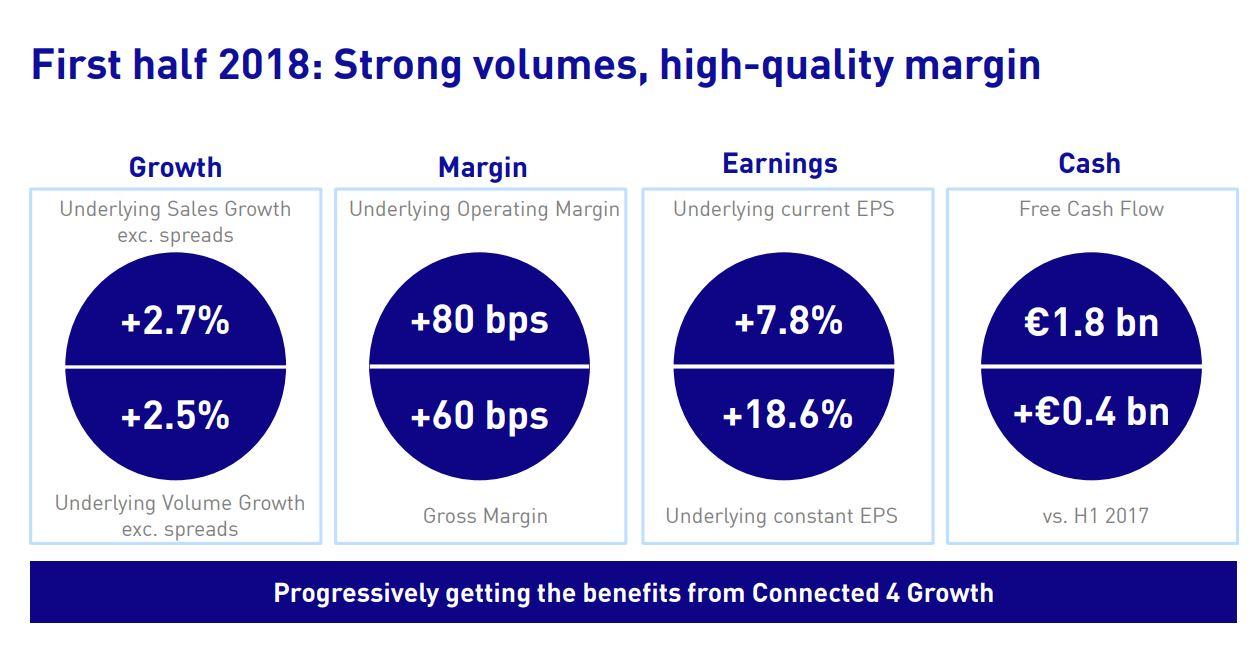

Source: Unilever FH2018 presentation

The company also continues to expand margins, which is highly encouraging, since its margins are actually on the lower end of the spectrum (compared to peers).

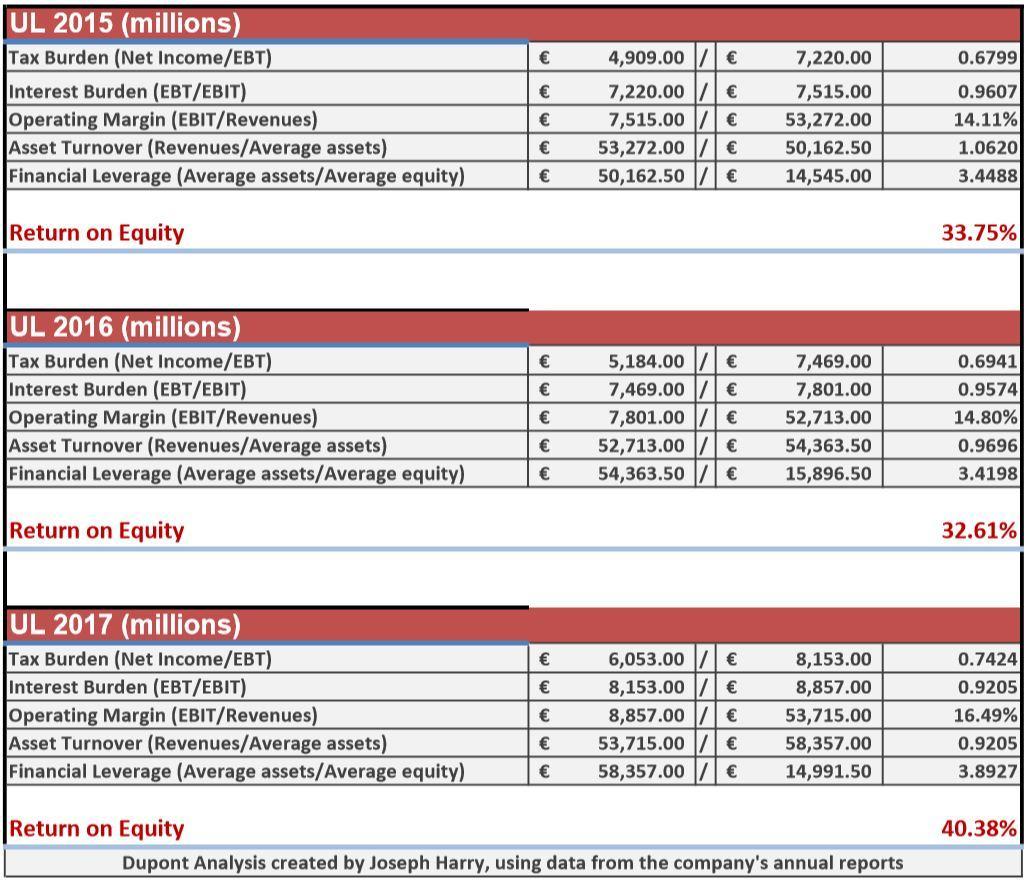

Return on equity analysis

Breaking apart Unilever’s ROE into five analyzable pieces gives us some more insight.

The company has been driving ROE higher largely through margin expansion, a lighter tax burden, and modestly increasing financial leverage. Asset efficiency (the amount of sales generated from its existing asset base, as measured by the asset turnover ratio) is declining, however.

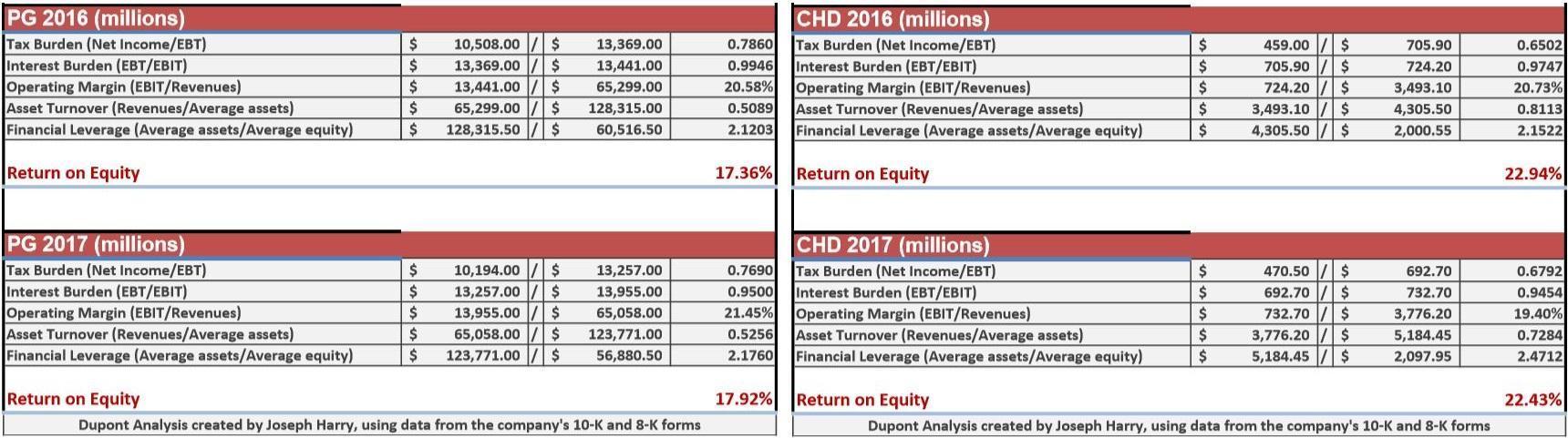

Despite lower margins, Unilever is still able to achieve leading ROE when stacked up against peers Procter & Gamble (NYSE:PG) and Church & Dwight (NYSE:CHD):

Even though the company’s asset turnover is declining, it’s still far superior to that of both of its peers. If anything, I think that Unilever has the opportunity to continue to expand margins, and even if it doesn’t get them to the 20% or higher range at the operating level, I still think it’s the superior operator in the space.

If we wanted to run a thought experiment and set the leverage ratio at 1x for all three firms (while holding everything else constant), Unilever would still come out on top, with underlying ROE of roughly 10.37%, versus just 9.07% for CHD and 8.24% for PG.

Conclusion

Since I last looked at Unilever back in June, it’s largely been “running stuck in place”, underperforming peers by a wide margin:

UL data by YCharts

UL data by YCharts

At the time, I said that:

I already own established positions in both UL and CHD (which I think are the superior companies long term), but if I was putting new money into this sector, I would take a long hard look at PG shares here. I think they provide the most potential upside as a value investment, and will also provide the highest yield along the way. Unilever remains the best firm in the industry overall, however.

Obviously, CHD was the way to go in hindsight, but PG’s rally also beat UL’s share price performance by a wide margin. Back in June, PG shares were closer to yielding 4% and trading at a decent discount to peers. Today, the gap has closed some between UL and PG valuations-wise, so I think Unilever is the way to go here due to its superior business quality. If the company does move to the Netherlands and the Dutch dividend tax remains, however, I think that shares could experience selling pressures in the short term.

Long term, I think it’s a very high-quality company trading around fair value here, while also paying a nice, safe dividend with a yield comfortably above 3%. I think that it’s especially important for dividend investors relying on UL for income to pay close attention to the headquarters situation, however, since a move could mean a vague “substitution payment mechanism” or a new 15% withholding tax on dividends. Therefore, if you want to continue to hold UL shares going forward, I would recommend holding them in a taxable account just to be safe. There’s also the (perhaps slight?) chance the company stays British, too.

If you enjoyed this article and would like to receive further updates and articles in the future, please feel free to hit the “Follow” button at the top of the page next to my name.

For even more exclusive content, please consider a free two-week trial to my marketplace service, Harry’s Retail Report.

Disclosure: I am/we are long UL, CHD.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Articles I write for Seeking Alpha represent my own personal opinion and should not be taken as professional investment advice. I am not a registered financial adviser. Due diligence and/or consultation with your investment adviser should be undertaken before making any financial decisions, as these decisions are an individual’s personal responsibility.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment