My regular readers know that I love a good “underloved” story. For that reason, people might be forgiven to think that I’d be a fan of Horizon Global Corp. (HZN), the shares of which are down about 54% over the past 12 months. They’d be forgiven for thinking that, but people would be wrong. I am not a fan of Horizon Global and I’ll go through my reasoning below. In a nutshell, the reward simply isn’t worth the risk at these levels.

The Company

Horizon Global is a leading designer, manufacturer, and distributor of a variety of custom engineered towing, trailering, and cargo management products. The company sells globally into three reportable segments: Horizon Americas, Horizon Europe-Africa, and Horizon Asia Pacific. The company serves the aftermarket, retail and OE markets.

In 2017, the company began experiencing performance issues related to some of the plants in Horizon Americas (Reynosa, Mexico, and Kansas City), and in their Romanian manufacturing facility in Europe-Africa. Although the company seems upbeat about the efficiency initiatives they’ve undertaken, they admit that global trade uncertainties overhang their business.

Financial Snapshot

A quick review of the financial history here suggests that sales are relatively robust. In fact, over the past five years, revenue has grown at a CAGR of about 8.7%, and operating profit has grown at a CAGR of ~43%. Unfortunately, that’s where the good news ends. As the company has grown sales, so too have they grown losses. Net income is significantly lower now than it was in 2013. Additionally, dilution seems to be a recurring theme, given that the share count has increased at a CAGR of about 6.7% over the past five years. In fairness, though, the share count has dropped somewhat from last year to this. Finally, the level of debt has ballooned massively over the past five years, up from ~$670,000 in 2013 to $310 million today. Also, $125 million of this debt is a convertible note due in 2022. In addition, fully 41% of the long term debt on the balance sheet is due in 2021, which increases the risk here obviously. In sum, the level of debt isn’t the only problem on the balance sheet as I’ll suggest below, but the capital structure represents significant risk in my view.

My level of pessimism doesn’t decrease when I look over a shorter time span because the first six months of 2018 have not been great relative to the same time last year. The most significant highlight (lowlight?) of this change relates to the $54.6 million charge the company took against its Europe-Africa asset. It seems that the Europe-Africa segment did not perform in line with forecasted results, largely because of a combination of increased commodity costs, and the fact that more of the market seems to be switching to lower margin products.

Source: Company filings

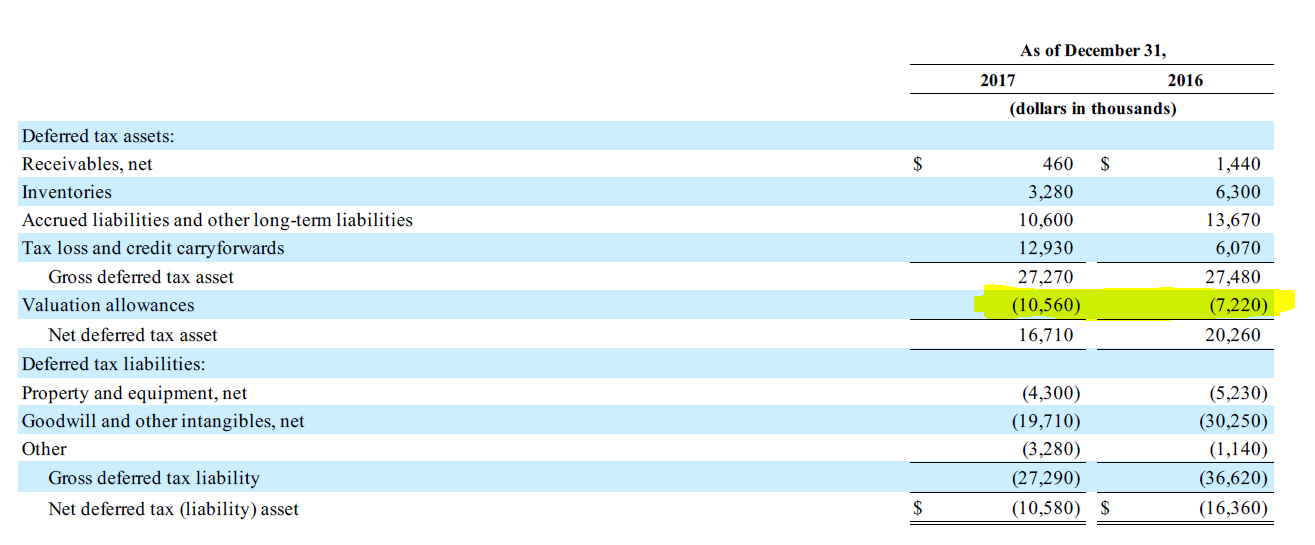

Increase in Valuation Allowance

I think it’s also worth noting that there’s some evidence that management themselves are not particularly sanguine about the short term future of the business. The reason for this is the elevated level of the valuation allowance against deferred tax assets from 2016 to 2017. Please note that this change isn’t posted on the balance sheet itself, but is buried in the notes.

Source: 10-K, pp 74

Source: 10-K, pp.39

Hard as it is to believe, the 10-K does not clearly describe what a valuation allowance is in plain language. For those who aren’t as familiar with them, there are a host of well written sources online that offer examples of this very telling balance sheet item. The gist of the matter is that these indicate that management themselves are skeptical that they will earn enough money in future to fully realize the economic value of their deferred tax assets. Rather than writing the deferred tax asset down, management applies a contra account against these assets. Thus, a valuation allowance is a signal that management itself is forecasting future trouble.

The Stock

The financial history here, and the likely financial future is troubling in my view. This doesn’t automatically disqualify this company from consideration, though. A troubled business can still be a wonderful investment if the price is right. The problem in this case is that the price is far from “right.”

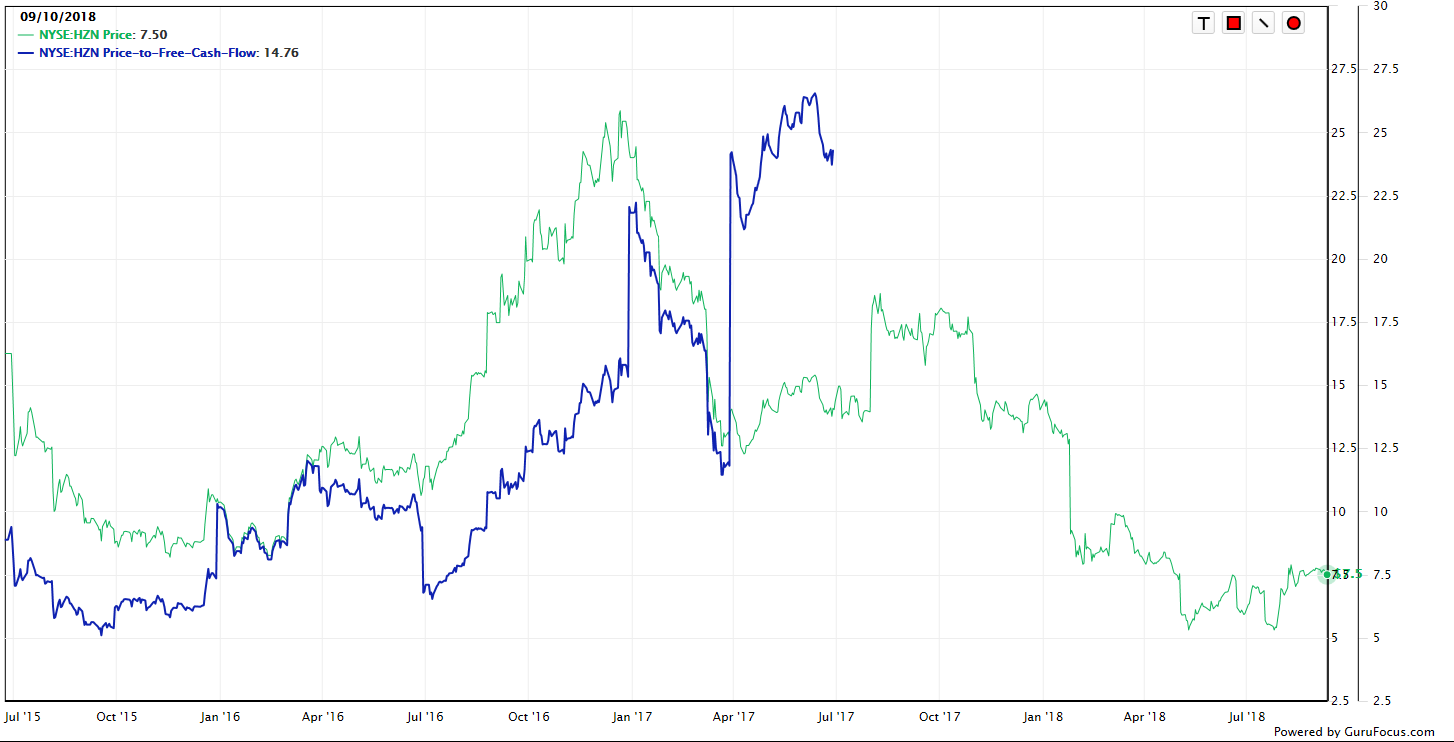

I judge whether a stock is a worthy investment based on a host of factors, two of which I typically write about on this forum. The first of these is the standard price to free cash flow metric, the second is a review of the market’s current assumptions about the business.

Price to free cash flow is quite easy to understand, and the perils of paying too much for a dollar of free cash flow is exemplified by Horizon. The following is a graph that charts both price to free cash flow and price over the past several years. Please note that the blue line “stops” in mid-2017, just as free cash dries up. Someone who bought when the shares were this expensive has subsequently been punished, driving home the idea that the more an investor pays for a future dollar of free cash, the lower will be their subsequent returns. There’s just too much that can go wrong when you pay a large premium over free cash flow, and nothing demonstrates that more effectively than this stock.

Source: Gurufocus

In addition to looking at price to free cash flow, I like to get a sense of what the market assumes about future growth of the business. The idea is that if the market is overly optimistic about the growth of the business, it will likely be disappointed over time, which will drive the shares lower. In order to work out the market’s current assumptions about the business, I turn to the excellent work done by Professor Stephen Penman in his book “Accounting for Value.” In this book, Penman relates how an investor can isolate the “g” variable in a fairly straightforward finance formula to work out what the market must be thinking about future growth in the business. At the moment, the market is assuming that earnings of Horizon Global will grow at a perpetual rate of about 6.5%. I consider this forecast to be excessively optimistic, especially given the history here.

Conclusion

I think one of the best reasons to be concerned about the future of thsi business is the fact that management themselves seem to be signalling a view that things are slowing. In spite of that, the shares remain relatively expensive in my view. I think this is a very dangerous combination for investors and I would suggest that they should sell shares before incurring further losses.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment