Sierra Metals (SMTS) is a base metal producer running three mines located in Peru (Yauricocha) and Mexico (Bolivar and Cusi):

Source: Sierra Metals

As the chart above shows, zinc and copper are the main metals produced by the company, accounting for 73% of total production.

Interestingly, this year the prices of zinc and copper have dropped significantly (26.4% and 18.4%, respectively) but Sierra shares have held steadily (a brownish area on the chart below):

Source: Stockscharts.com

Note that since the beginning of 2017 Sierra shares have been moving in a wide trading range (C$2.9 – C$3.7), most recently outperforming a popular copper sector ETF (COPX).

In my opinion, there’s a good reason why Sierra shares hold steadily. In this article I’m trying to explain this phenomenon.

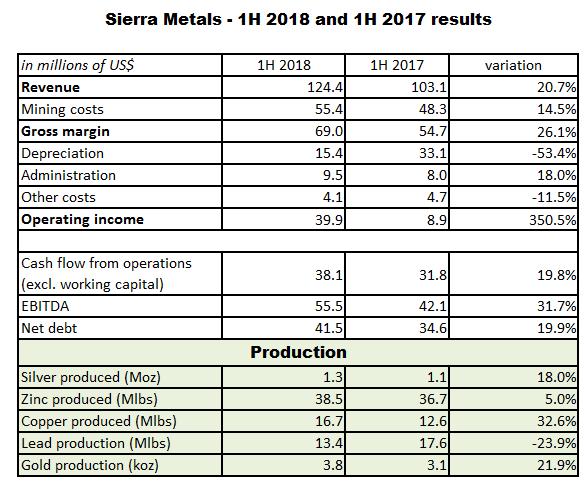

1H 2018 results

Firstly, let me discuss the company’s results. The table below presents a few main measures reported in 1H of 2018 and 2017:

Source: Simple Digressions

As the table shows, in 1H 2018 Sierra improved generally all measures across the board. First of all, due to higher production and stronger metal prices, revenue went up 20.7%, compared to 1H 2017. However, before I go on, it has to be noted that revenue reported in 1H 2017 was a bit distorted.

Look at these figures:

- in 1H 2017 Sierra produced 4.9 million ounces of silver equivalent (payable metal) and sold 6.4 million ounces. It means that the company sold more metals than it produced, significantly reducing its inventory and artificially inflating revenue figures

- in 1H 2018 the company produced and sold 8.0 million ounces of silver equivalent

It means that despite much higher production reported in 1H 2018 (an increase of 63%, compared to 1H 2017), the 1H 2018 revenue was only slightly higher than in 1H 2017 (an increase of 25%). What’s more, in 1H 2018 the company was selling its metals (silver equivalents) at a lower silver price than in 1H 2017 (a drop of 4.0%, compared to 1H 2017). As a result, revenue reported in 1H 2018 is up only 20.7%, compared to 1H 2017.

As a result, due to artificially higher revenue reported in 1H 2017, the results reported in 1H 2018 are hardly comparable to 1H 2017. However, even with this inconvenience, an operating profit and cash flow were much better than in 1H 2017.

Note: In 1H 2018 an operating profit was driven up by a very low depreciation charge of $15.4M ($33.1M in 1H 2017). It’s another misleading occurrence but there is a simple explanation. Namely this year the company significantly increased mineral reserves at its flagship property, Yauricocha (from 243.9 million pounds of zinc at the end of 2016 to 477.2 million at the end of 2017). As a result, a unit depreciation charge (calculated as: book value of a mine divided by the amount of metals to be produced over the life of the mine) went strongly down, driving the total depreciation charge down as well.

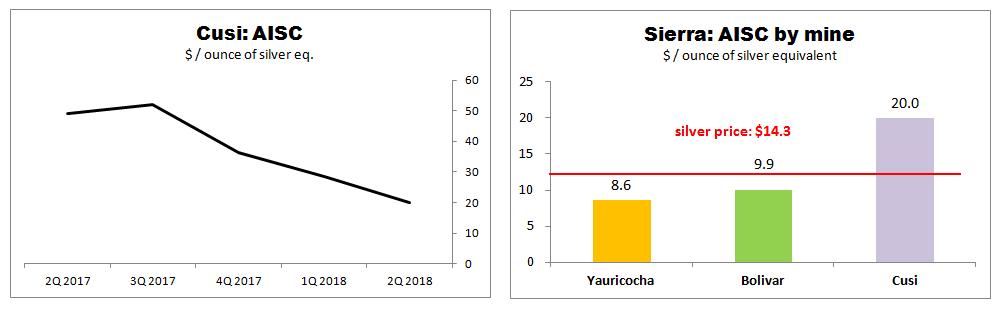

Costs of production

I’m very impressed to see cost cuts reported by Sierra this year. The chart below shows an all-in sustaining cost (AISC) of production (the panel on the right) reported by each mine in 2Q 2018:

Source: Simple Digressions

Note the two largest operations, Yauricocha and Bolivar, are cash flow positive mines today, producing their metals at AISC of $8.6 and $9.9 per ounce of silver equivalent, respectively. The third mine, Cusi, is still a high-cost producer (AISC of $20.0 per ounce of silver equivalent) but, as the panel on the left shows, the mine performs much better than in the past. I’m confident that sooner or later we will see additional cuts in costs of production at this small silver producer.

Bolivar and Cusi are much better now

Generally, Sierra Metals is about the Yauricocha mine. The flagship property is responsible for nearly everything here (margins, cash flows, production etc.) but the other two mines, although still of secondary importance, are making good progress. As discussed above, the Cusi mine is showing lower costs of production and Bolivar already is a low-cost producer. What’s more, in 1H 2018 both laggards increased production:

- Bolivar produced 7.6 million pounds of copper (an increase of 19.3%, compared to 1H 2017)

- Cusi delivered 298 thousand ounces of silver (an increase of 49.7%, compared to 1H 2017

As a result, a gross margin delivered by these two mines accounted for 22.6% of the total gross margin generated by the company while in 1H 2017 Bolivar and Cusi participation was 18.3%, only.

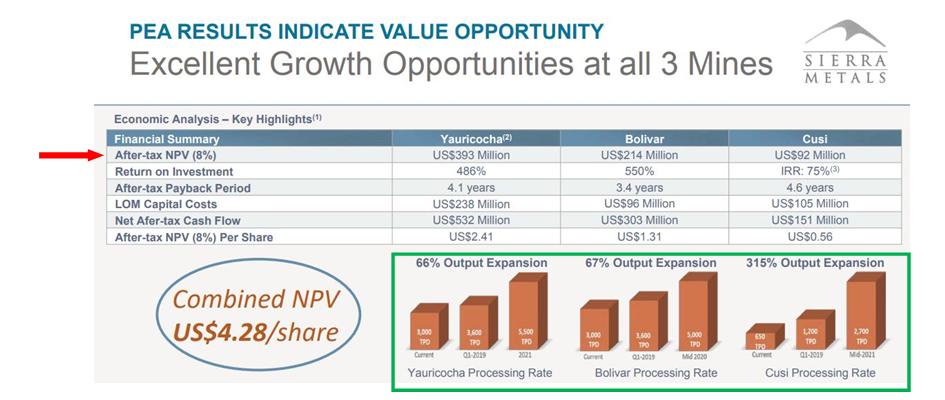

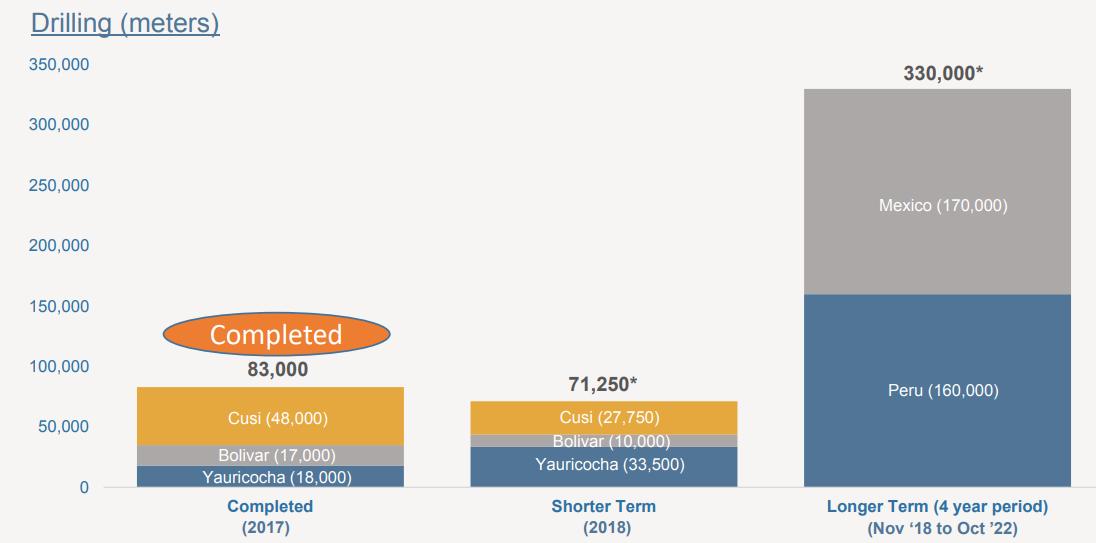

What’s more, as the graph below shows (the green rectangle), the company wants to convert the Cusi mine into a large-scale operation, increasing the mill’s throughput from the current 650 tons of ore per day to 2,700 tons in 2021:

Source: Sierra Metals

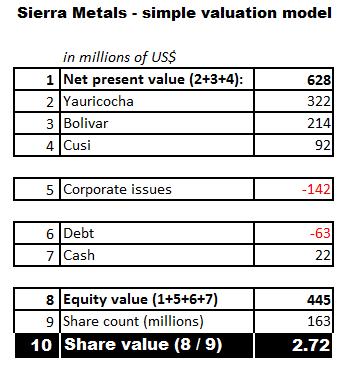

Valuation

This year Sierra released the updated technical reports for all three mines. As a result, it’s possible to build a simple valuation model based on the data delivered by the company. The graph above depicts net present values disclosed in technical reports for Yauricocha, Bolivar and Cusi (the red arrow). I have plotted these values into the table below and, after making a few small adjustments, I arrived at the equity value of the company of $445M or $2.72 a share:

Source: Simple Digressions

Notes:

- The company holds an 82% interest in Yauricocha so the net present value of $393M should be cut by 18%

- The figure depicted in the line “Corporate issues” was calculated assuming annual corporate expenses of $27M; this figure was additionally adjusted by a statutory Canadian corporate tax rate of 26.5%

- According to the company, the longest-life operation is the Bolivar mine; hence, I assume that the company will operate for eleven years

- Debt and cash figures are as of June 30, 2018

Today Sierra shares are trading at $2.55 a share so they are slightly undervalued.

Upside potential

I always stress that discounted cash flow valuation models do not take into account the upside potential the mining properties demonstrate. And, in my opinion, in the case of Sierra this potential is substantial. Look at the graph below:

Source: Sierra Metals

As the graph shows, in the coming years the company wants to continue a very aggressive exploration program (started in 2017). Up to now this program was very fruitful and resulted in a significant increase of mineral reserves and resources. For example, Yauricocha’s mineral reserves (zinc) increased by 96% and Cusi’s silver resources went up more than 150%.

Definitely, Sierra’s properties offer significant upside potential.

Risk

Share liquidity

Sierra shares are listed on the American Stock Exchange (AMEX) under the ticker SMTS. This year the average daily trading volume for these shares was 43.3 thousand. It is not a high figure. What’s more, there are trading days when there is very small volume or even no volume at all.

Summary

I’m impressed by Sierra Metals’ results reported in 1H 2018. Generally all measures improved, compared to 1H 2018. The company produced more metals at a lower cost and converted the Bolivar mine into a cash flow generating operation. What’s more, the Cusi mine, the smallest and the worst operation, is heading for the right direction – costs are falling and production is rising.

As a result, in my opinion, the company is well-positioned for a period of lower base metals prices. Yauricocha and Bolivar produce metals at an all-in sustaining cost of production below $10.0 per ounce of silver equivalent, which means that even today these mines are profitable and cash generating operations. Very soon the Cusi mine should join them.

According to the simplified valuation model presented in this article, one share of Sierra is worth $2.72. Today Sierra shares are trading at $2.55 so they are slightly undervalued. However, as discussed above, this figure does not take into account the significant upside potential demonstrated by each property.

Final Note

Did you like this article? If your answer is yes, please visit my Unorthodox Mining Investing Marketplace service where I manage a portfolio of up to 10 mining picks, discuss new investment ideas, and provide subscribers with a medium-term outlook on a few financial markets (particularly the base/precious metals market).

Disclosure: I am/we are long CEF, GDX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment