Seadrill (SDRL) has recently filed a 6-K report, which updates the financial information in the registration statement of Form F-1 and provides financials for the first half of this year. While the first half of the year is long past us since it’s the end of September, the information provided in this report is interesting and allows us to look both at the situation in Seadrill during bankruptcy and what the future may bring for the company. Without further ado, let’s look at the key points.

Source: Seadrill 6-K filing

In the first half of this year, the company was obviously suffering from a significant deterioration on the revenue side. Busy with bankruptcy proceedings, Seadrill had no practical chance of keeping backlog intact amidst very tough market conditions. This picture looks grim, but unfortunately for Seadrill, there is more pain ahead.

Here’s what the company writes on its backlog in the filing:

“Our contract backlog, as of September 27, 2018, totaled approximately $2.2 billion. Of the total contract backlog, $0.7 billion is attributable to our semi-submersible rigs and drillships and $1.5 billion attributable to our jack-up units. We expect approximately $0.2 billion of our contract backlog to be realized in the remainder of 2018“.

So, unless Seadrill adds more business for this year, the company will have $200 million of revenue in the fourth quarter. If we travel in time and look at the fourth-quarter revenue in 2016, before bankruptcy, we’ll find it at $667 million. In the fourth quarter of 2015, revenues stood at $959 million. This is a vivid picture of how the business might shrink in just a few years due to low demand, poor dayrates, and the difficult restructuring process.

In my opinion, it is now obvious that fourth-quarter results will look ugly. I don’t think third-quarter results will look pretty either, especially given the fact that investors will look at fresh-start accounting numbers, which, as history of restructurings in the offshore drilling and offshore supply vessel space shows us, will be sobering.

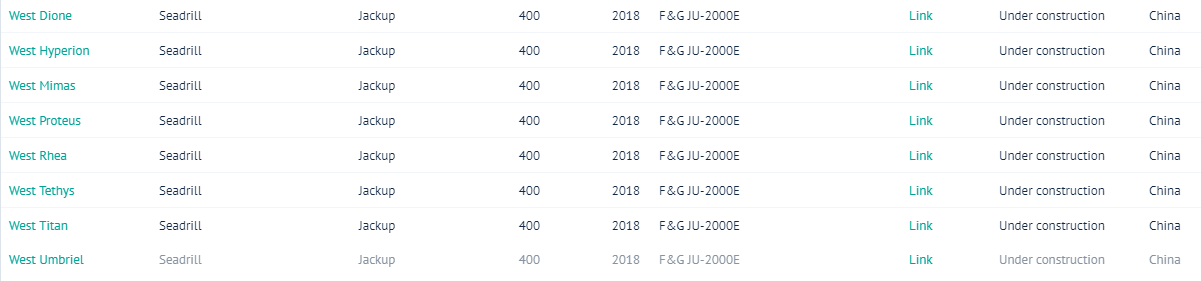

Another interesting point is the newbuild jack-ups, which fell into no man’s land during the restructuring:

Source: Bassoe Offshore

Here’s the company’s comment on this issue:

“As at June 30, 2018, we had contractual commitments under eight newbuilding contracts totaling $1.7 billion. The newbuilding commitments are for eight jack-up contracts that we have with the Dalian shipyard. These contracts are all with limited liability subsidiaries of Seadrill Limited that do not have the benefit of a Seadrill Limited guarantee. We continue discussions with Dalian regarding taking delivery of those units“.

Put simply, the new Seadrill is not obliged to take them (which has been long known since the companies that hold these jack-ups were non-debtors in the restructuring process), but is still in some “discussions” with the yard. Perhaps, we’ll hear more on this topic when the company reports its third-quarter earnings and holds the conference call with analysts. While listed as Seadrill’s in Bassoe database, I don’t see how the company can take the delivery of those rigs, especially under current conditions, with revenue tanking. I’d also note that given the company’s revenue performance and the debt load, the words of the CEO that Seadrill is poised to make acquisitions seem rather strange to me.

Seadrill’s shares are recovering together with shares of other offshore drillers on the back of stronger oil prices. Shares may have more speculative upside due to the general inflow of money into the offshore drilling sector. However, I’d note that Seadrill won’t have that much fuel for upside as other drillers as it has recently gone through restructuring and traders who decided to bet on the industry’s failure have not established significant short positions compared to other major drillers.

If you like my work, don’t forget to click on the big orange “Follow” button at the top of the screen and hit the “Like” button at the bottom of this article.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I may trade any of the above-mentioned stocks.

Be the first to comment