Investment Thesis

Roots (OTC:RROTF) delivered weak Q2 2018 earnings due to a tough comparable from last year’s “Canada 150” celebration. As a result, its shares slid over 20% and have resulted in a forward P/E ratio of 8.5x. The selloff is likely overdone as the company still has solid initiatives to grow its top and bottom lines. Its UBR strategy continues to help it deliver gross margin expansion. The company’s expansion into Asia and the United States should provide a long runway of growth. However, negative traffic trends will likely result in weak comparable sales growth in Q3 and perhaps even Q4.

Why Roots’ shares dived more than 20% after its earnings release

Roots reported disappointing Q2 2018 earnings. As a result of its weak earnings, its shares have dived about 24% in two days. Let us review why its shares have plunged by this much before we discuss why we continue to remain bullish.

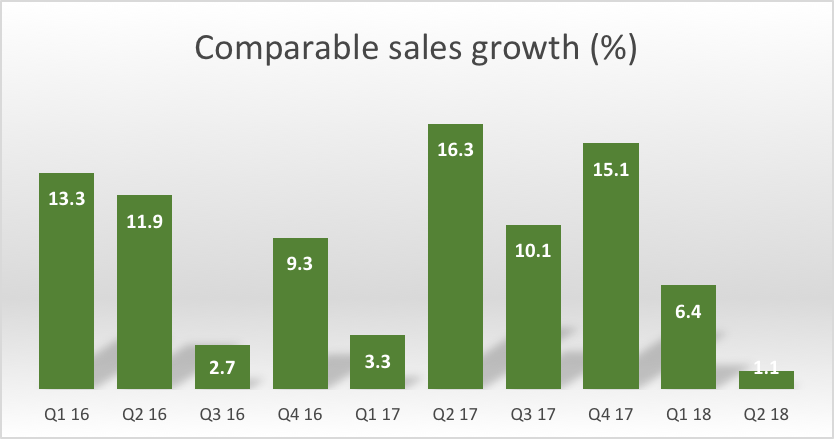

As the chart below shows, Roots’ comparable sales growth rate of 1.1% in Q2 2018 was the lowest in more than 2 years. As many investors know, 2017 was the 150th anniversary of Canada’s confederation. Roots took advantage of this and recorded comparable sales growth of 16.3% in Q2 2017. Originally we thought that mid-single digit comparable sales were achievable as the company achieved similar growth in Q1 2018. However, we were disappointed by its comparable sales growth rate of only 1.1% year over year.

Source: Created by author; Company Reports

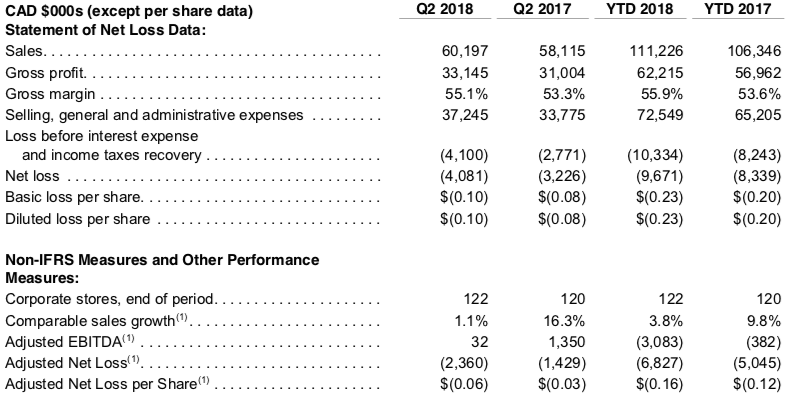

As a result of its lower comparable sales growth rate, Roots’ revenue only grew by 3.6% year over year. Its adjusted EBITDA of only C$32 thousand in the quarter was also significantly lower than last year’s C$1.4 million. Upon examination, this was primarily due to rising selling, general and administrative expenses. Its SG&A expenses increased from C$33.8 million in Q2 2017 to C$37.2 million in Q2 2018. The company’s SG&A expenses as a percentage of total revenue increased from 58.1% in Q2 2017 to 61.9% in Q2 2018. The result was likely due to the fact that it opened several new stores in Boston and Washington. In addition, the company also ramped up marketing expenses to increase its brand awareness in these new markets.

Source: Q2 2018 MD&A

In the conference call, management also indicated that they have experienced negative traffic trends in Q2 and this has carried onto Q3 as well. Management revealed that last year’s Canada 150 celebration has resulted in positive sales of around C$8 to C$9 million in 2017. The company estimated that revenue in Q2 2017 benefited was positively impacted by around C$4 million of additional sales. Hence, it was a tough comparison. However, this also means that we may continue to see slower than expected comparable sales in the third quarter given the fact that management mentioned that they continue to experience negative traffic trend in its fiscal Q3.

Reasons why we still like the company and believe it can continue to grow its top and bottom lines

Despite a weaker than expected quarter, we remain bullish in the medium to longer term. Here are reasons why we are still bullish on Roots:

Second quarter revenue only represent a small portion of its total sales

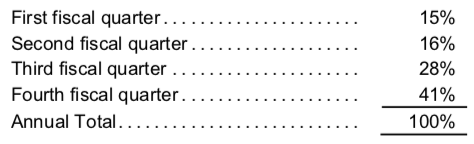

Although Roots had a weak quarter, we need to also consider seasonality. As the table below shows, sales in its second quarter typically represents about 16% of its total annual sales. As can be seen, Q3 and Q4 sales together comprised nearly 70% of its total sales. We believe Q3 earnings release will give us a better indication of whether Roots can overcome its current negative trend.

Source: Q2 2018 MD&A

United Brand Range merchandising strategy is working well

Roots’ United Brand Range initiative has been performing well. The UBR initiative is a consumer-focused merchandising strategy focused on building a more simplified and scalable product assortment as well as a more consistent presentation that is coordinated across collections and categories. This analysis-driven approach helps management to edit out unproductive SKUs and amplify better performing products. The company has reduced its SKU count by 25% since Q2 2016. Its UBR initiative was a big contributing factor to its gross margin expansion. As a result, its gross margin has improved significantly from 53.3% in Q2 2017 to 55.1% in Q2 2018. This helped it to grow its gross profit from C$31.0 million to C$33.1 million in Q2 2018. This growth rate of 6.9% was much higher than its revenue growth rate of 3.6% year over year.

E-commerce growth

E-commerce continues to be the fastest growing part of Roots’ business. Although no specific numbers were provided in its conference call, the company estimates that e-commerce will reach about 20% to 22% of its direct-to-consumer sales in its fiscal 2019.

Store renovations and relocations

Another key driver to Roots’ business is through store renovations and relocations. The company has renovated or relocated 3 stores in Q2 2018. Management provided in the conference call that store relocations and renovations have resulted in about 20% increase in sales year over year. Looking forward, we believe management will continue to evaluate its existing stores and optimize its sales through store renovations and relocations.

Source: Q2 2018 MD&A

Several other growth opportunities

We like Roots’ growth opportunities and believe these opportunities should provide a long runway of growth:

Expansion to the United States

The company has recently opened two new stores in Boston in June 2018. The company is targeting 10 to 14 new retail locations in the United States by the end of 2019 and hopes to have about 100 locations in the long-term. We like the fact that the company’s selective approach and is not targeting too many markets in the same time.

International Market

The second growth opportunity for Roots is markets in Asia. In the past quarter, the company opened 2 partner-operated stores in Taiwan and 1 partner-operated store in China. The company now has 112 and 27 partner-operated stores in Taiwan and China respectively.

Footwear/Leather

The third growth opportunity is Roots’ re-launch of new footwear and leather products in 2018. This should help grow its revenue further. Management noted that 2018 would be the year to lay the groundwork. They are optimistic that footwear will soon represent a significant share of its total revenue (double-digit range). However, selling footwear is not the same as selling its other products. It will take competency in selling footwear to keep customer satisfactions at a high level. Hence, we believe labor cost may increase as its sales increase.

We still have some concerns

We remain cautious about Roots Q3 comparable sales growth, as management did not provide much detail of how they will overcome the negative traffic trend. On top of that, management indicated in the conference that they would not cut its profit margin to stimulate sales. We will like to see more detail of management’s plan to increase store traffic in its third quarter conference call. We think it might be better for investors to apply a wait-and-see approach.

Valuation

Management has chosen to keep its fiscal 2019 targets:

- Sales of C$410 million to C$450 million.

- Adjusted EBITDA of C$61 million to C$68 million.

- Adjusted net income of C$35 million to C$40 million.

At this point, we think it might be wise to be conservative. Hence, we would choose the lower end of its guidance to estimate our target price. Its net income of C$35 million in fiscal 2019 is equivalent to about C$0.83 per share. As a result, its P/E ratio based on fiscal 2019 estimate would be about 8.5x. This is very low. As a comparison, Canadian retailer Aritzia is currently trading at a forward P/E ratio of 21.6x. We believe Roots deserve a P/E ratio of at least 13x. Using this P/E multiple, we have a target price of C$10.79 per share. This is equivalent to a return of 53% (based on the share price of C$7.06 at the end of closing on September 13, 2018).

Investor Takeaway

Despite a weak Q2 2018, we believe Roots will be able to return to strong growth given its solid growth prospects. However, we think it might still be challenging to increase its comparable sales in Q3 given a tough comparable from last year. Nevertheless, we believe the recent selloff is overdone as its forward P/E ratio has declined down to only 8.5x. This actually presents a good opportunity for investors willing to ride out short-term volatility.

Note: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

Thank you for reading. If you like my article, please scroll to the top of the article and click on “follow” to receive future updates.

Disclosure: I am/we are long RROTF.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment