Introduction

Welcome to my Oil Weekly report. In this report, I wish to discuss the effects of crude oil inventories and net speculative positioning changes, based respectively on the Weekly Energy Information Administration (EIA) report and the Commodity Futures Trading Commission (CFTC) estimates, on oil markets. Then, I identify key global and oil market developments and their impacts on iPath S&P Crude Oil Total Return Index ETN (OIL).

Crude and petroleum stocks

According to the latest EIA report, U.S. oil stockpile dipped for the fourth consecutive week, down 1.32% (w/w) to 396.2m barrels on the August 31 – September 7 period, whereas Cushing inventories plunged 5% (w/w) to 23.58m barrels. With these decreases, crude storage deficit worsens again, establishing now 5.6% or 23.5k barrels below the 5-year average and 15.4% or 72k barrels under last year’s inventory.

Source: EIA

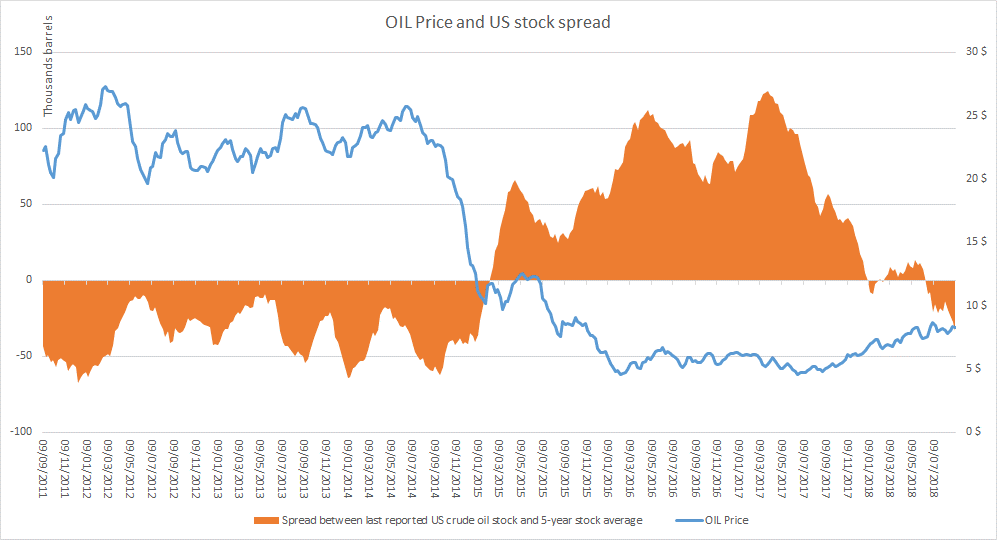

Meanwhile, the five-year U.S. oil storage spread continues its plunge, down 33.1k barrels on the respective period and continues to sustain crude futures and OIL share price.

Source: EIA

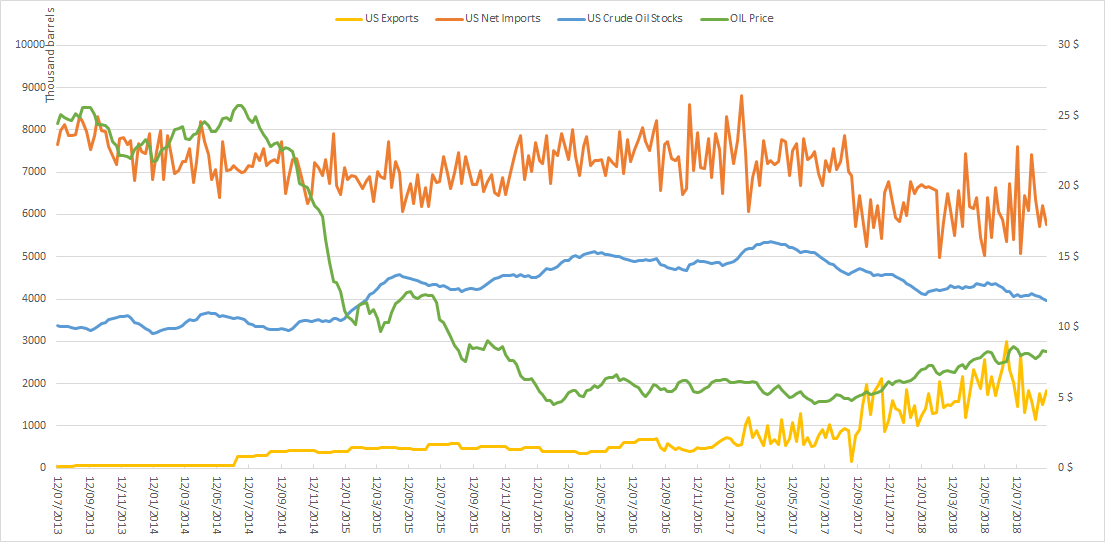

On the other side, refined product continued to build up, following accelerating utilization rates, which approach full capacity (97.6%). Gasoline stocks posted a weaker (w/w) advance, up 0.53% to 235.9m barrels compared to the previous period, mainly due to the robust gasoline demand, whereas distillate stockpiles surged 4.63% to 139.3m barrels.

Concomitantly, U.S. crude oil balance improved over the week, amid boosting exports, up 21.22% (w/w) to 1.83m barrels and dipping net imports, down 7.14% (w/w) to 5.76m barrels.

Source: EIA

U.S. crude production slightly declined on the August 31 – September 7 period, down 0.91% (w/w) to 10.9m barrels. However, the latest Baker Hughes report accounted for 7 new oil rigs on the following week, which might propel oil output to new highs and therefore, weigh on OIL shares.

Source: Baker Hughes

In the meantime, OIL lost 1.27% to $8.26 per share, growing demand worries and trade tariff intensification.

Source: Bloomberg

Speculative positioning

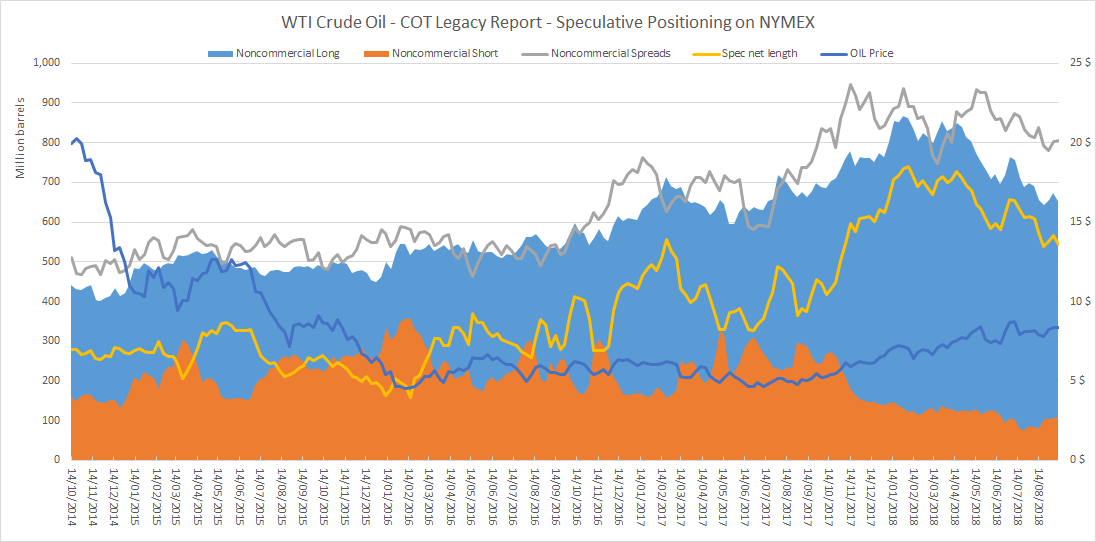

According to the latest Legacy Commitment of Traders Report (COTR) released by the CFTC on September 4-11 period, crude net speculative length on NYMEX futures declined moderately, down 3.87% (w/w) to 543 845 contracts, while OIL shares advanced 0.25% to $8.36 per share.

Source: CFTC

Oil net speculative positioning dip is attributable to both moderate long liquidations and slightly building short accumulations. Over the period, long speculative positioning dove 3.04% (w/w) to 652,935 contracts and was amplified by short builds of 1.29% (w/w) to 109,090 contracts.

Since the beginning of the year, net speculative positioning plunged further and is now down 12.88% or 80,368 contracts, whereas OIL (YTD) ramp up persists, up 27.05% to $8.36 per share.

Fresh U.S. $200b tariffs on Chinese goods bullies already weakening oil demand

Since my last article, OIL lost 2.83% to $8.24 per share, following demand dip linked to the passage of Hurricane Florence and growing concerns that OPEC countries will not be able to counterbalance losses from not only Iran but also Venezuela and Libya.

U.S. administration should announce later today the already famous $200b trade tariffs on China, triggering similar measures from its counterpart, which will inevitably hurt already weakening oil demand. The U.S. is entering the refining maintenance season, which should boost crude storage figures and further weigh on OIL shares.

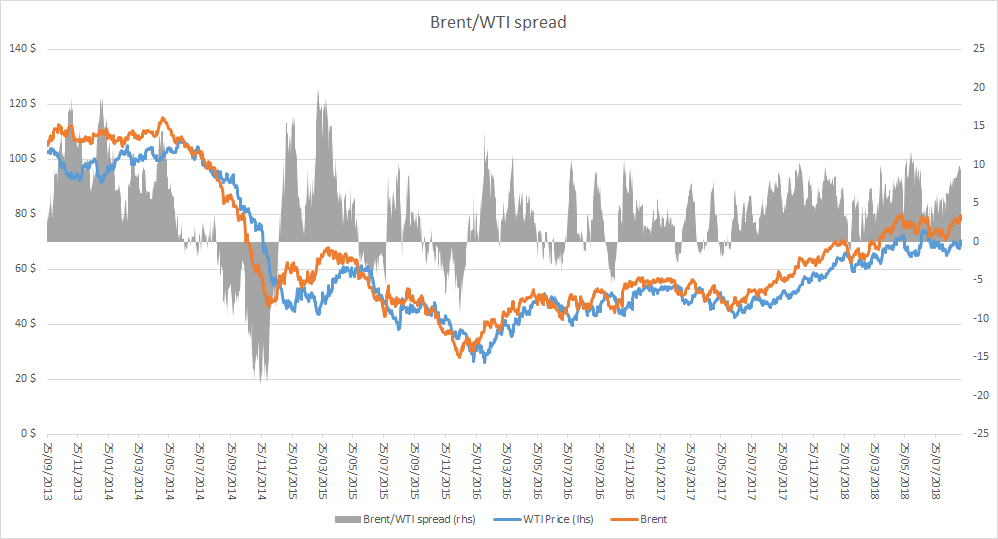

The Brent-WTI spread widened again, from $8.3 to $9.81 per barrel on the September 4-11 period, following storage deficit acceleration and supply concerns linked to approaching Iran oil sanction date.

In the meantime, the dollar index (DXY) measuring the bucks strength against a basket of major currencies retested its strong support level of $94.50. Recent announcement of 10% tariff on about $200b in Chinese goods next week are not favoring the greenback anymore, but the emerging markets currency rout will weigh on foreign investors’ oil purchase power.

Source: TradingView

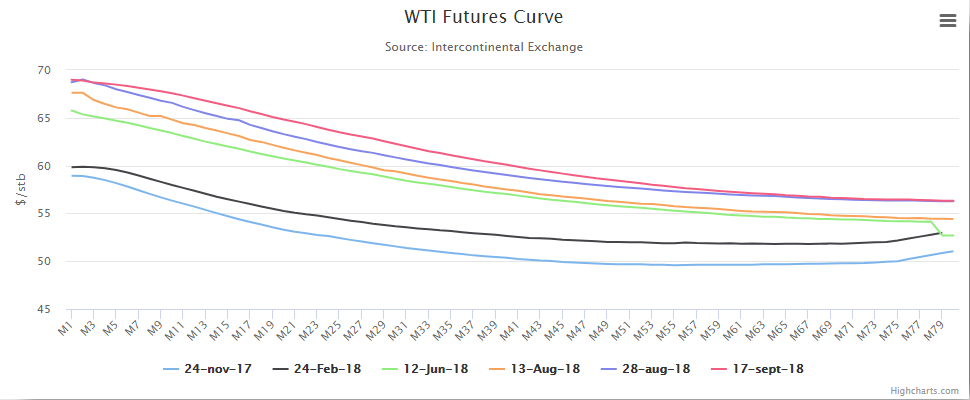

WTI futures backwardation slope flattens on nearby maturities, signaling that oil demand expectation in the short term is declining, whereas international investors’ supply concerns ease.

Given the elements above, I maintain my bearish short- and long-term view on OIL given U.S. aggressive trade policy.

I look forward to reading your comments. If you enjoyed the article, thanks for showing your support by following my account or sharing the article.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a short position in OIL over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment