Preface

Viking Therapeutics (NASDAQ:VKTX) threw quite the pass this week for a first down. It was NAFLD data that was, at the least, comparable to its direct future competitor: Madrigal Pharmaceuticals (MDGL).

In light of the new, all-important proof of concept, I will have to adjust my thesis and price target on Viking. The following article will assess my original thesis, compare Viking’s data with Madrigal’s data, and review my renewed thesis in Viking going forward.

Original Conviction Thesis

Grade “A” investment call (my previous way of saying “conviction buy”): see article

Original thesis with price target:

In the event (1) phase 2 for VK2809 is successful, propelling Viking Therapeutics to a NASH player, (2) the company secures a positively perceived partnership for VK5211, and (3) the general market cooperates, I envision the market cap appreciating towards $800 million to $1 billion (~ $15-20/share). If not before phase 2 data, Viking will likely have to raise cash to support phase 3 trials for VK5211 and VK2809, as well as ongoing proof-of-concept trials for younger pipeline prospects. All things considered, I will place a price target at $15 before the year’s end. This includes room for necessary dilutive financing.

Source: CBR article, May 18

| Buy Price | Timeline | Price Target | Relevant Events |

| $5.15 | < 7 months | $15 |

|

After announcing positive VK2809 Phase 2 data today, Viking surpassed my original price target of $15. Because the relevant events and the price target were met, I will now reevaluate the investment thesis in Viking.

NAFLD Trial

I will compare Madrigal’s data to Vikings only because it gives us a reference (not because I’m arguing Viking should be valued similarly to Madrigal). I will focus on what is relevant: NAFLD data (I understand Viking’s primary endpoint was hypercholesterolemia).

Note: Madrigal has both NAFLD and NASH data. Madrigal has trialed ~3x more patients. Madrigal has efficacy and safety data at 36 weeks. Viking does not yet have the extensive amount of data Madrigal has.

To do this, I need to first look at trial design, how the NAFLD endpoint was assessed, inclusion criteria, and exclusion criteria:

Trial Design

- Viking: Double-Blind, Randomized, Placebo-Controlled; 35 patients

- Madrigal: Double-Blind, Randomized, Placebo-Controlled; 116 patients

How NAFLD Endpoint Was Assessed

- Viking: “determined by magnetic resonance imaging-estimated proton density fat fraction (MRI-PDFF) at 12-weeks”

- Madrigal: “determined by magnetic resonance imaging-estimated proton density fat fraction (MRI-PDFF) at 12-weeks”

Inclusion Criteria (relevant to NAFLD)

- Viking: “Must have confirmation of ≥10% liver fat content on PDFF-MRI, BMI of 18.50 – 40.00 kg/m2 inclusive at screening, waist circumference >40 inches in men or >35 inches in women”

- Madrigal: “Must have confirmation of ≥10% liver fat content on PDFF-MRI, male and female adults ≥18 years of age with a BMI <45 kg/m^2, biopsy-proven NASH”

Exclusion Criteria (relevant to NAFLD)

No relevant differences between Viking and Madrigal.

NAFLD Data

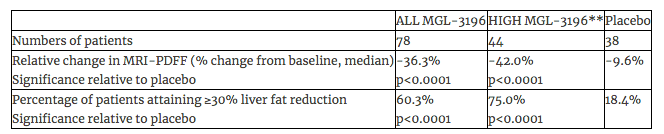

Madrigal:

Source: Madrigal Press Release

- Statistically significant reductions in ALT and AST were observed in the treatment arm.

- Statistically significant improvements in secondary endpoints including LDL-C, triglycerides, apolipoprotein B, and Lp A.

- Drug was well-tolerated with only a few moderate adverse events, balanced between placebo and treatment arm.

- There were no adverse effects on laboratory or vital sign (e.g. blood pressure) parameters.

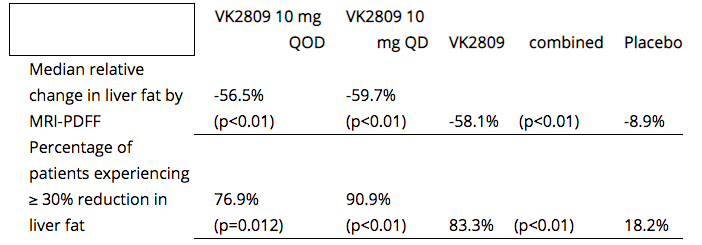

Viking:

Source: Viking Press Release

- Reductions in ALT were observed in treatment arm. There were no meaningful differences in bilirubin, alkaline phosphatase, or INR. There was no meaningful change to the thyroid hormone axis.

- Statistically significant improvements in LDL-C, apolipoprotein B, and Lp A were seen in treatment arm.

- Drug was well-tolerated and without any serious adverse events. According to Viking, the “total number of AEs was highest in placebo arm”.

Summary:

| NAFLD measures | MDGL | High MDGL | Placebo | VKTX | High VKTX | Placebo |

| Relative Δ in MRI | -36.3% | -42% | -9.6% | -56.5% | -59.7% | -8.9% |

| % of patients >30% fat reduction | 60.3% | 75% | 18.4% | 76.9% | 90.9% | 18.2% |

- The trials were similar in design. So, it’s, generally, fair to compare data between Viking and Madrigal. We do so, however, with an understanding that there may have been coincidental factors that influenced the data (e.g. if Viking’s enrolled patients had “more fatty” livers at baseline that would give them an “unfair” advantage over Madrigal).

- When assessing liver fat reduction, it is most fair to assess the “high doses” between the two. Viking is the clear leader (Note: is Viking’s dose higher than Madrigal’s? Meaning, is Viking using more “drug” than Madrigal? This would be a good question to look into).

- Both drugs appear safe and well-tolerated. Viking purposely highlighted liver enzyme safety data, as this was a major concern with the drug. Also important, no changes in the thyroid hormone axis imply that the drug’s systemic effects are dulled.

- As long as VK2809 remains SAFE after 36 weeks, I believe it is likely to reap superior NASH data than Madrigal’s (based on NAFLD data, it’s almost certain to have a significant impact in NASH).

Valuation

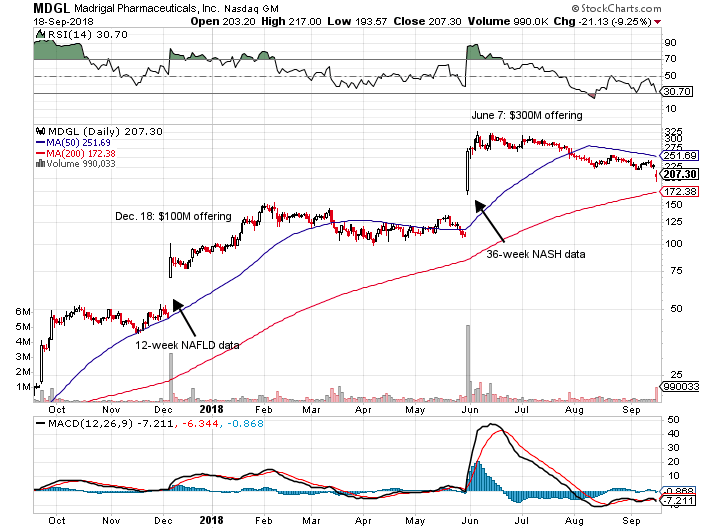

Madrigal‘s valuation following 12-week data (where Viking is now) was ~ $1.1B. They had ~ $62M in cash and no debt. “Under the Roche (OTCQX:RHHBY) Agreement, Roche exclusively licensed certain patent rights and know-how relating to MGL-3196 in exchange for consideration consisting of an upfront payment, milestone payments, the remainder of which total $10 million and are tied to future commencement of Phase 3 clinical trials and regulatory approval in the United States and Europe of MGL-3196 or any derivative product, and single-digit royalty payments based on net sales of MGL-3196 and any derivative products, subject to certain reductions.” Patients for MGL-3196 expire between “2026 and 2033”.

Chart courtesy of StockCharts.com

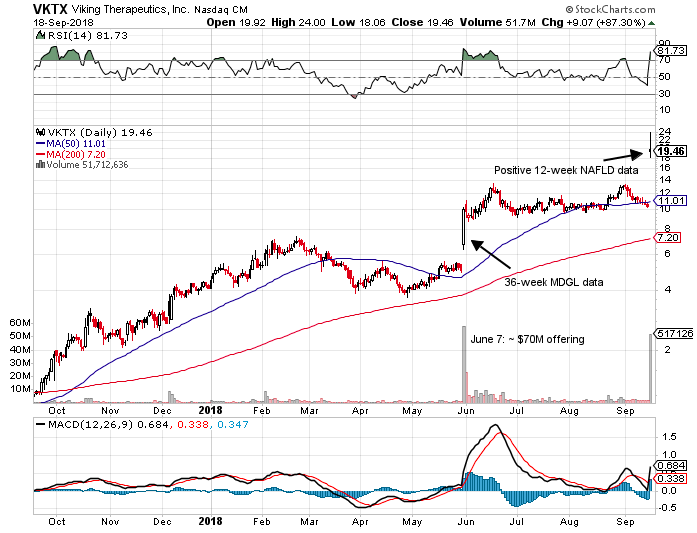

Viking’s valuation following 12-week data was ~ $1.2B. They have ~ $140M in cash and no debt. They will owe Ligand (NASDAQ:LGND) “75.0 million per indication (for up to a total of three indications) upon the achievement of certain development and regulatory milestones and up to $150.0 million upon the achievement of certain sales milestones” + “low-to-middle single-digit royalties upon sales of VK2809”. Patents for VK2809 expire between “2025 and 2038”.

I can assume the intellectual properties for both companies are relatively equal. So, I can forgo involving this when comparing valuation.

Chart courtesy of StockCharts.com

Summary

Viking’s Phase 2 data far exceeded expectations. The sample size is smaller but because the effect was so great, I can reasonably and safely assume this will likely translate in larger populations. 2809 can now be theorized to have best-in-class potential in NASH because of this data. Coincidentally, Viking is trading eerily similar to Madrigal following 12-week data. Similar to what happened to Madrigal, I expect Viking to appreciate more in the coming months. It is of note, however, that Viking is, at least, 18-24 months away from having 36-week data in NASH. I believe Viking is now reasonably valued between $22-26/share. I would suggest aggressively accumulating shares in the event prices fall < $18. Relevant catalysts should justify a greater valuation than $22-26/share in the coming months.

Viking remains a conviction buy. I will assign a new price target of $30/share to be reached within 12 months, implying a 50% upside at writing. The PT assumes an offering ~$100M and also depends on other relevant catalysts (listed below).

| Timeline | Price Target | Relevant Events |

| < 12 months | $30 |

|

Authors note: For more conviction ideas like Viking, be sure to subscribe to my exclusive marketplace, The Formula.

Disclaimer: The intention of this article is to provide insight not investment advice. While the information provided in this article is intended to be factual, there is no guarantee and prospect investors are encouraged to do their own fact-checking and research before investing in a company. One must also consider one’s own financial standings, risk tolerance, portfolio diversification, etc. before making a decision to buy shares in a company. Many of my articles detail biotechnology companies with little or no revenue. These stocks are, therefore, speculative and volatile. Even when prospects seem promising, there is no predicting the future. Losses incurred may be significant.

Disclosure: I am/we are long VKTX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Be the first to comment