There is no denying that Hertz (NYSE:HTZ) has been an absolute disappointment over the past few years. Between 2016 and 2017, the stock price declined from $50 to less than $10. At this point, the company is trading at roughly $18 after a very solid second-quarter report. It seems that growth is bottoming, thanks to a strong economy and Hertz’s measures to improve profitability and customer outreach. On top of that, we could be in for higher used car prices, which could massively support the company’s residual values.

Source: Hertz

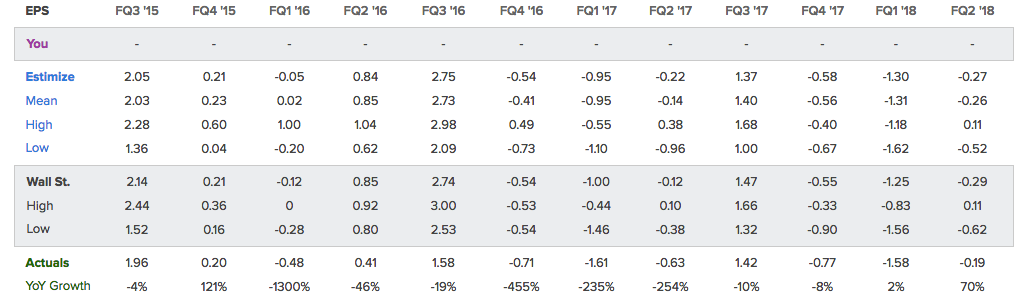

Both Sales and EPS Beat Estimates

Second-quarter sales came in at a loss of $0.19 versus expectations of -$0.29. This is the second consecutive earnings beat and the second consecutive quarter with an EPS improvement.

Source: Estimize

Sales came in at $2.39 billion versus expectations of $2.32 billion. This puts the sales growth at 7%, which is the fourth consecutive quarter of higher sales.

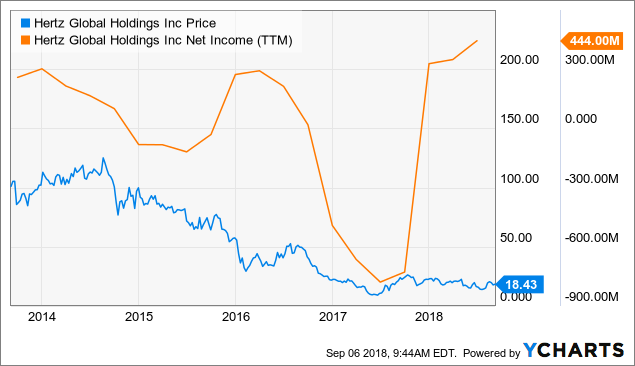

The bigger picture shows that net income on a trailing twelve-month basis is back at its highs of currently $444 million after going below -$600 million in 2017.

HTZ data by YCharts

HTZ data by YCharts

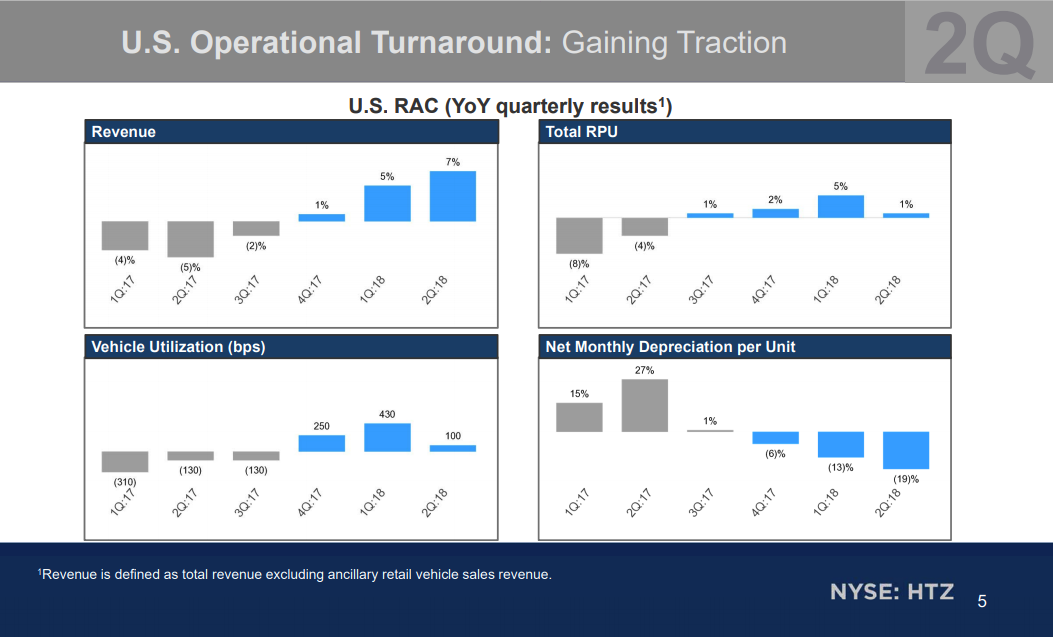

Moreover, we are witnessing an acceleration trend. Revenue growth has accelerated after bottoming in Q2 2017. Growth has increased from -5% to currently 7%. Revenue per user is growing since the third quarter of 2017, even though the growth rate is quite low. Depreciation also declined by 19%, which is the third consecutive quarter of lower depreciation numbers. I will elaborate on this in the second half of this article.

Source: Hertz Q2/2018 Earnings Presentation

Sales were supported by both higher volume as well as higher time and mileage rates. On top of that, the company is once again improving its utilization rate. The current utilization rate is at 81%, which is the result of machine learning and better fleet management. The total vehicle capacity increased 3% in the second quarter excluding fleet dedicated to transportation network companies.

International rental revenues increased 8%, which is the result of a strong European market. The European market accounts for roughly 25% of Hertz’s total sales. Moreover, SG&A as a percentage of total sales increased to 70% from 67% in Q2 2017. This is the result of overall higher rental activities and the company’s current turnaround.

The company itself mentioned that profits are still lagging investment costs. This is simply the result of a long-term turnaround which takes some time to unfold. And even though the second quarter showed that Hertz is making strong progress, there is more to come.

What’s Next?

Before I move over to what I consider to be a massive tailwind for Hertz, it is important to focus on the company’s own measures to enhance productivity and overall top line growth regardless of its business environment. I just mentioned that SG&A costs increased 3 points, which is the result of higher spending. This is expected to stay high, according to the second-quarter earnings call:

A significant portion of our incremental spending is related to additional personnel as well as consulting resources primarily in field operations and technology support. In those areas, spending will remain elevated through 2019 as we continue the operations improvement program and update our 30-year old technology platform.

Especially marketing suffered from long-term underinvestment, according to Hertz. The result are the company’s measures to improve fleet productivity/utilization, marketing, as well as a better connection to the customer. This will be achieved by brand marketing campaigns, machine learning programs, as well as better training for current and new employees.

Source: Hertz Q2/2018 Earnings Presentation

On top of that, the company will provide a better platform to sell used cars. And speaking of used cars, one of the reasons why Hertz struggled over the past few years is the fact that second-hand car prices were in a strong downtrend. This is a massive problem for a company which is highly dependent on the value of its biggest assets (rental cars).

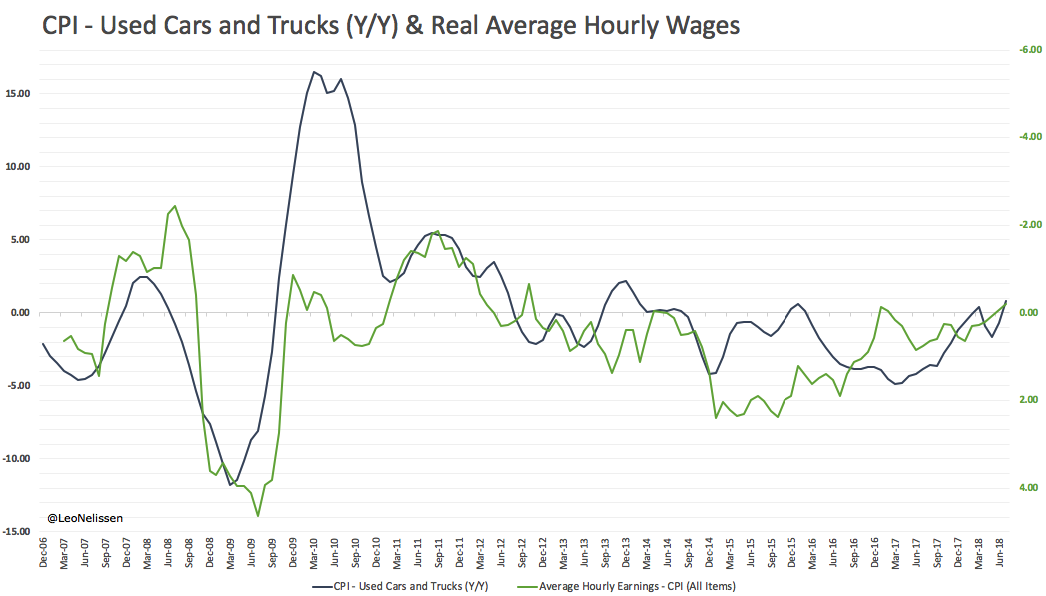

In July, the price of an average used car or truck was 0.8% higher compared to its prior-year quarter. This is the second positive growth rate since January 2016 and another high of the uptrend that started in March 2017. I compared this graph to real wages (inverted). Real wages in this case are average hourly earnings minus CPI growth (all items). What we see is that real wages are actually down, which is the result of outperforming input prices in the current inflation trend. The price of oil is a major factor, considering that oil is back at $70 after dropping below $30 in 2016. That said, I expect that used car prices continue to improve. I am not sure if we are going to see growth rates similar to the ones of 2011, but I do expect more than 2% growth over the next few months.

Source: Author’s spreadsheets (Raw data: FRED)

This means that rental companies, which were amongst the biggest losers during the depreciation trend, will be among the biggest winners again.

Hertz itself is also noticing a trend reversal:

Monthly vehicle depreciation expense of $285 per unit decreased 19% versus the prior year quarter. The decrease in unit vehicle depreciation expense is a result of continued favorable market residual values we spoke about in the first quarter call as reflected in the Manheim rental index, which posted increases of 79% per month in the quarter.

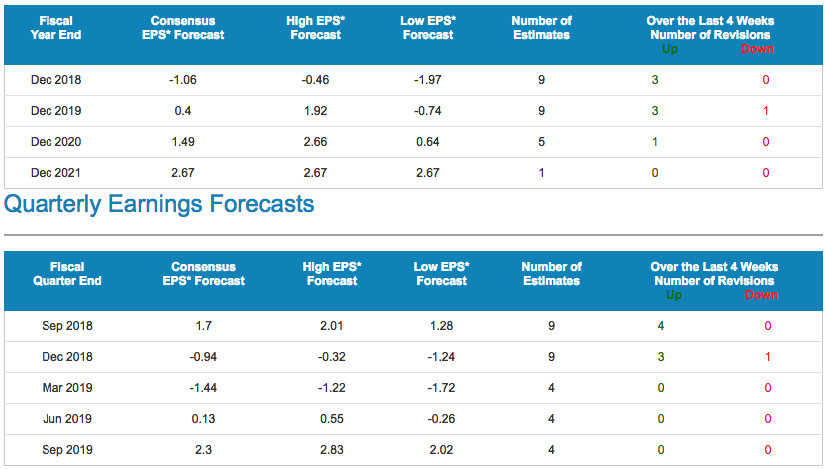

Analysts seem to agree. EPS expectations for 2018, 2019, and 2020 have been raised, while especially the third and fourth quarters of this year are expected to do better. We also see that real improvements are expected to happen in 2020, when EPS is expected to come close to $1.50. 2021 is expected to be almost double that at $2.67.

Source: Nasdaq

Which brings us to the valuation. At this point, the stock is valued at 1.4 times earnings (not a typo) with a forward P/E of 66. This is the simple result of a company in danger that is working on a recovery. Hertz is trading at just 12 times 2020 earnings. This means that current buyers have to look much further than 2019. That said, I also expect more EPS revisions, as the macro environment continues to be favorable. This means that lending volume and residual values will continue to improve.

A problem is the company’s debt position. Hertz has a current ratio of 0.85, which indicates possible liquidity problems on the mid-term. On top of that, the company’s debt-to-equity ratio is at 20.5.

However, the first debt maturity will take place in October 2020, while the company invested a lot of cash, which was the reason why the current ratio went below 1.0. Also, Hertz expects free cash flow to grow significantly in the full year 2018. It is not expected to get a positive cash flow result, but the trend could indicate positive cash flow in 2019.

All things considered, I like the company’s turnaround and its longer-term outlook. It seems that Hertz will continue to benefit from rising residual values and a stronger economy, which supports car lending volume and average customer spending. I expect the stock to finish a higher low, which could lead to a stock price of $25 over the next few months.

The downside is a risky balance sheet which could cause serious harm to the stock price in case of an economic decline or management failure to effectively implement the new technology and employment measures.

Be aware of these risks and keep your position small. The stock is volatile, and the company is not out of the woods yet.

Stay tuned!

Thank you for reading my article. Please let me know what you think of my thesis. Your input is highly appreciated!

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in HTZ over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This article serves the sole purpose of adding value to the research process. Always take care of your own risk management and asset allocation.

Be the first to comment